Choosing the right financial advisor represents one of the most consequential decisions you'll make regarding your financial future. Among the various types of advisors available, understanding fiduciary financial advice and its significance can fundamentally impact the quality of guidance you receive. Unlike advisors who follow a suitability standard, fiduciary advisors are legally and ethically bound to act in your best interest at all times. This distinction matters tremendously when you're planning for retirement, managing investments, or making complex financial decisions that will affect your lifestyle for decades to come.

What Defines Fiduciary Financial Advice

Fiduciary financial advice operates under a strict legal standard requiring advisors to place client interests ahead of their own. This obligation is not merely a suggestion or best practice but a binding duty enforced through regulatory frameworks and professional standards.

The fiduciary standard mandates several core responsibilities:

- Duty of loyalty: Advisors must prioritize client interests without conflicts of interest

- Duty of care: Recommendations must be based on thorough research and professional expertise

- Full disclosure: All fees, compensation structures, and potential conflicts must be transparently communicated

- Prudent management: Investment decisions must follow sound principles aligned with client goals

These requirements create a fundamentally different relationship compared to the suitability standard, where recommendations need only be suitable rather than optimal. Understanding fiduciary practices helps investors recognize the protection this standard provides.

The Legal Framework Behind Fiduciary Obligations

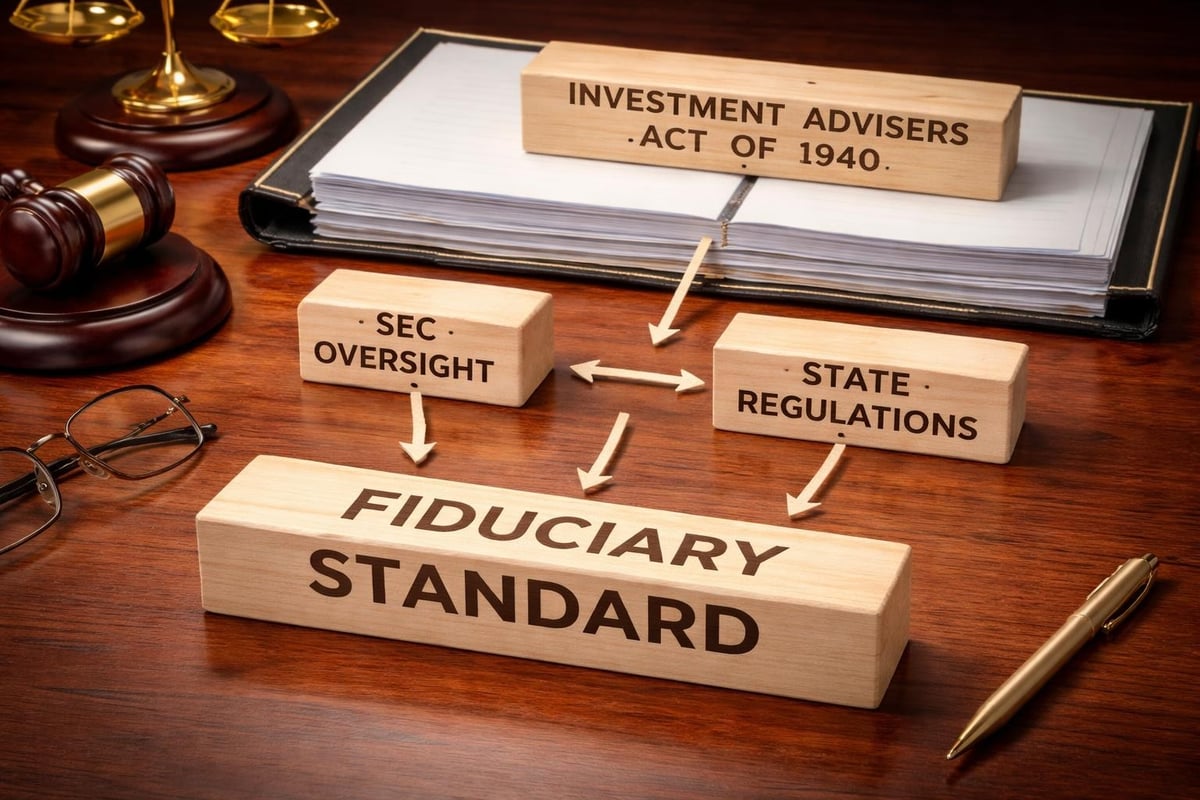

The legal foundation for fiduciary financial advice stems from multiple regulatory sources. Registered Investment Advisors (RIAs) operate under the Investment Advisers Act of 1940, which establishes comprehensive fiduciary duties. The Uniform Prudent Investor Act provides additional guidance for investment management, emphasizing modern portfolio theory and risk-adjusted returns.

State securities regulators and the Securities and Exchange Commission (SEC) oversee compliance with these standards. Advisors who violate their fiduciary duties face serious consequences including regulatory sanctions, legal liability, and professional censure. This enforcement mechanism provides meaningful protection for clients.

How Fiduciary Advice Differs From Other Financial Guidance

Understanding the distinction between fiduciary and non-fiduciary advisors requires examining compensation structures, regulatory requirements, and professional obligations. These differences directly impact the advice you receive and whose interests that advice serves.

| Feature | Fiduciary Advisor | Non-Fiduciary Advisor |

|---|---|---|

| Legal Standard | Best interest | Suitability |

| Compensation Disclosure | Comprehensive and transparent | May be limited |

| Conflicts of Interest | Minimal or disclosed/managed | May be undisclosed |

| Product Recommendations | Based solely on client needs | May include proprietary products |

| Ongoing Obligation | Continuous duty | Transaction-specific |

Commission-based brokers typically operate under the suitability standard, meaning they can recommend products that generate higher commissions as long as those products are suitable for the client. Fee-only fiduciary advisors, conversely, earn compensation directly from clients rather than product sales, eliminating this inherent conflict.

Compensation Models and Their Impact

The way your advisor gets paid significantly influences the guidance you receive. Fee-only advisors charge directly for their services through hourly rates, flat fees, or assets under management percentages. This structure aligns advisor success with client success.

Fee-based advisors may charge fees but also receive commissions from certain products. While some fee-based advisors maintain fiduciary standards, the commission component introduces potential conflicts. Commission-based advisors earn money from product sales, creating incentives that may not always align with client interests.

When evaluating financial consulting services, understanding these compensation structures helps you identify potential biases in recommendations. Transparency in fees should be non-negotiable in any advisory relationship.

Key Benefits of Working With a Fiduciary Advisor

Engaging a fiduciary advisor provides tangible advantages that extend beyond simple investment selection. These benefits compound over time, potentially adding significant value to your financial outcomes.

Objective recommendations form the foundation of fiduciary advice. Without commission incentives, advisors focus exclusively on strategies that advance your goals. This objectivity proves especially valuable during major life transitions such as retirement, inheritance management, or business sales.

Comprehensive financial planning addresses the interconnected nature of your financial life. Rather than isolated product sales, fiduciary advisors examine how investment management, tax planning, estate strategies, and retirement preparation work together. This holistic approach identifies opportunities and risks that single-product focus might miss.

Enhanced Trust and Transparency

The fiduciary relationship fosters deeper trust through mandatory disclosure requirements. You'll understand exactly how your advisor earns compensation, what conflicts exist, and how those conflicts are managed. This transparency eliminates hidden agendas and creates accountability.

Research suggests that knowing who to trust with money advice provides peace of mind that extends beyond financial returns. When you're confident your advisor is legally bound to prioritize your interests, you can focus on your goals rather than questioning motivations.

Regular communication and documentation create clear records of recommendations, rationale, and implementation. This documentation proves valuable for tracking progress, tax purposes, and ensuring continuity if circumstances change.

Questions to Ask When Selecting a Fiduciary Advisor

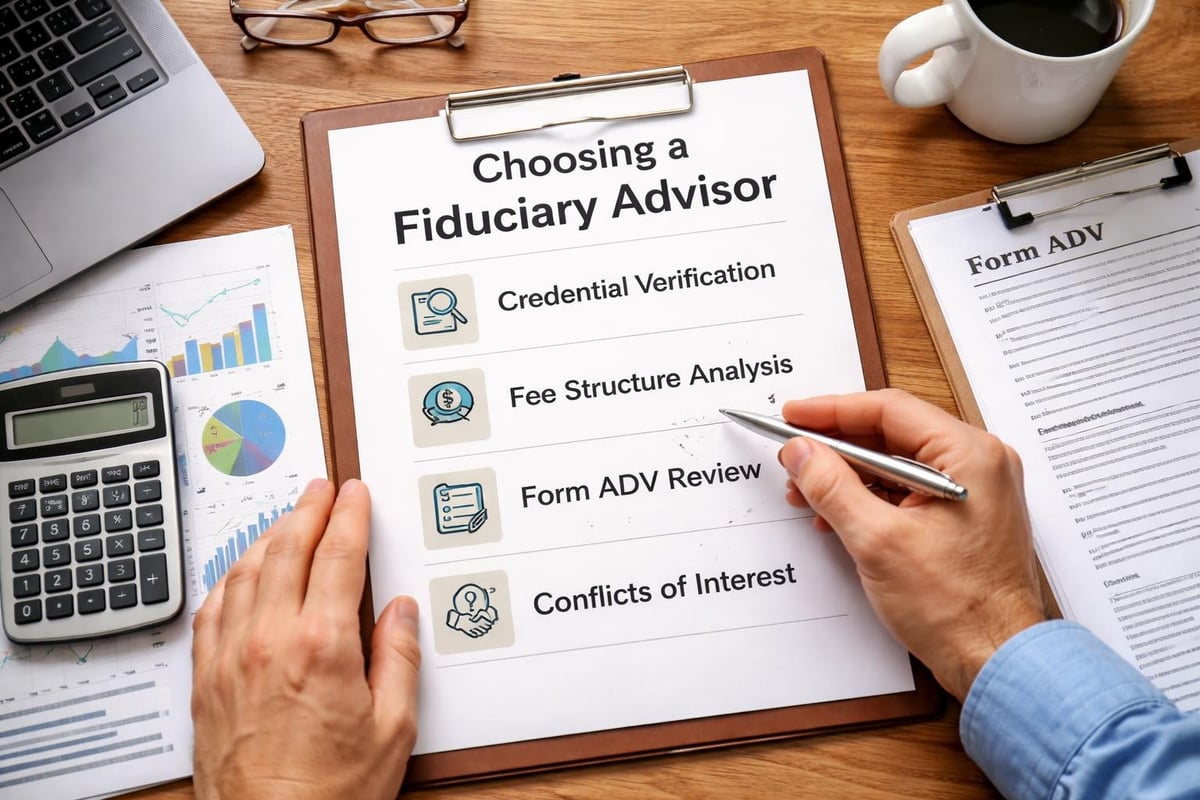

Identifying a genuine fiduciary advisor requires asking specific questions and verifying credentials. Not every advisor who claims fiduciary status operates under that standard for all services.

Essential Verification Steps

- Ask directly: "Are you a fiduciary for 100% of our relationship?"

- Request Form ADV: This SEC-required document discloses business practices, fees, and conflicts

- Review compensation structure: Understand all revenue sources including commissions, fees, and third-party payments

- Check credentials: Verify certifications such as CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst)

- Examine affiliations: Determine if the advisor is affiliated with broker-dealers that may limit fiduciary obligations

Verifying your financial advisor’s fiduciary status requires diligence, but the effort protects you from misrepresentation. Some advisors wear "two hats," acting as fiduciaries for planning services while operating under suitability standards for product sales.

The National Association of Personal Financial Advisors represents fee-only fiduciary advisors who commit to comprehensive fiduciary standards. Membership in professional organizations like NAPFA indicates adherence to rigorous ethical standards.

Common Misconceptions About Fiduciary Financial Advice

Several myths persist about fiduciary advisors that can confuse investors seeking quality guidance. Clarifying these misconceptions helps you make informed decisions.

Myth: All financial advisors are fiduciaries. Reality indicates that many advisors operate under suitability standards, particularly broker-dealer representatives. The title "financial advisor" isn't regulated, meaning anyone can use it regardless of their actual obligations.

Myth: Fiduciary advice costs more. While fee-only advisors charge transparent fees, commission-based advice often costs more when considering embedded product costs. Hidden fees in commission-based products can significantly exceed transparent advisory fees over time.

Myth: Fiduciary advisors only serve wealthy clients. Modern fiduciary practices, including virtual-first models, make professional advice accessible to various wealth levels. Many fiduciary firms offer tiered services or project-based planning for clients at different life stages.

The Reality of Fiduciary Relationships

Fiduciary financial advice emphasizes ongoing relationships rather than transactional interactions. Your advisor should regularly review your situation, adjust strategies as circumstances change, and proactively identify planning opportunities.

This continuity proves especially valuable for complex needs such as retirement and estate planning, where coordination across multiple strategies delivers superior outcomes. Tax efficiency, for instance, requires understanding how investment decisions, retirement distributions, and estate transfers interact.

Technology has transformed how fiduciary advisors deliver services. Virtual-first advisory models maintain the fiduciary standard while offering convenience and accessibility. Video conferences, secure document sharing, and digital planning tools enable comprehensive advice regardless of geographic location.

The Role of Technology in Modern Fiduciary Advice

Advances in financial technology enhance how fiduciary advisors serve clients while maintaining the personal relationship that effective planning requires. These tools augment rather than replace professional judgment.

Digital platforms enable:

- Real-time portfolio monitoring and performance reporting

- Sophisticated tax-loss harvesting strategies

- Scenario modeling for retirement and major purchases

- Secure communication and document management

- Integrated financial planning across all life areas

Artificial intelligence in financial planning raises important questions about maintaining fiduciary principles in technology-driven advice. While AI can process vast data and identify patterns, human judgment remains essential for understanding client values, goals, and unique circumstances.

Ethical implementation of technology requires transparency about algorithmic recommendations, human oversight of automated processes, and clear communication about how technology influences advice. The fiduciary duty extends to ensuring technology serves client interests rather than operational efficiency alone.

Fiduciary Standards in Different Advisory Contexts

The application of fiduciary standards varies across different financial services and regulatory environments. Understanding these distinctions helps you identify where you're protected and where additional scrutiny is warranted.

Investment Management vs. Financial Planning

Investment advisors managing portfolios operate under clear fiduciary obligations defined by securities regulations. Their duty covers investment selection, portfolio construction, risk management, and performance monitoring.

Financial planning encompasses broader territory including budgeting, insurance analysis, tax planning, and estate strategies. When working with a fiduciary for comprehensive planning, ensure their fiduciary duty extends to all planning areas, not just investment management.

Some advisors limit their fiduciary role to specific services while acting in other capacities for different needs. This segmentation can create confusion and potential conflicts. Clear written agreements should specify exactly where fiduciary obligations apply.

Retirement Plan Fiduciaries

Retirement plans such as 401(k)s involve specific fiduciary requirements under ERISA (Employee Retirement Income Security Act). Plan sponsors, investment committees, and advisors to these plans must act prudently and solely in participants' interests.

For individuals, understanding whether your pension financial advisor operates as a fiduciary affects the quality of rollover recommendations and retirement income strategies. Conflicts of interest can be particularly problematic when advisors recommend rolling over low-cost employer plans into higher-fee IRAs.

Building a Long-Term Relationship With Your Fiduciary Advisor

The value of fiduciary financial advice compounds through sustained relationships. Unlike transactional interactions focused on individual products, ongoing advisory relationships evolve with your changing needs and circumstances.

Effective long-term advisory relationships include:

- Regular review meetings to assess progress toward goals and adjust strategies

- Proactive communication about market changes, tax law updates, and planning opportunities

- Life event responsiveness when major changes require strategy modifications

- Multigenerational planning that addresses legacy goals and family dynamics

- Education and guidance that enhances your financial understanding

Your advisor should function as a strategic partner in making financial decisions across all major life areas. This partnership model contrasts sharply with sales relationships where contact occurs primarily when new products become available.

Measuring Advisory Value Beyond Returns

While investment performance matters, fiduciary advisors create value through multiple dimensions. Tax efficiency can add significant value by reducing unnecessary tax burdens. Strategic planning around Social Security claiming, retirement account distributions, and charitable giving optimizes lifetime wealth.

Behavioral coaching prevents costly emotional decisions during market volatility. Studies indicate that preventing one major panic-driven mistake can justify years of advisory fees. Your advisor's ability to keep you focused on long-term strategies during short-term turbulence delivers measurable value.

Estate planning coordination, insurance optimization, and risk management provide protection and peace of mind that transcend simple return calculations. The estate planning advantages of working with a comprehensive fiduciary advisor include integrated strategies that minimize taxes and ensure smooth wealth transfer.

Professional Designations and Fiduciary Commitment

Various professional certifications indicate commitment to fiduciary principles, though not all credentials mandate fiduciary status. Understanding these designations helps you evaluate advisor qualifications.

| Designation | Fiduciary Requirement | Focus Area |

|---|---|---|

| CFP (Certified Financial Planner) | Yes, when providing planning | Comprehensive planning |

| CFA (Chartered Financial Analyst) | Yes, when managing investments | Investment analysis |

| CPA/PFS (Personal Financial Specialist) | Yes | Tax-integrated planning |

| ChFC (Chartered Financial Consultant) | Ethics code, not always fiduciary | Financial planning |

| AIF (Accredited Investment Fiduciary) | Yes, for designated services | Investment fiduciary practices |

The Committee for the Fiduciary Standard advocates for authentic fiduciary practices across the financial services industry. Their work highlights the importance of verifying that credentials translate to actual fiduciary obligations in practice.

Continuing education requirements for these designations ensure advisors maintain current knowledge of regulations, strategies, and best practices. When selecting an advisor, ask about their education, experience, and ongoing professional development.

The Future of Fiduciary Financial Advice

The financial advisory landscape continues evolving toward greater transparency and client-centric standards. Regulatory discussions about expanding fiduciary requirements signal growing recognition of this standard's importance.

Technological advancement will continue reshaping service delivery while the fundamental fiduciary obligation remains constant. Virtual advisory models make professional fiduciary advice accessible to broader populations, democratizing access to quality guidance.

Younger generations increasingly demand transparency and alignment of interests, driving industry evolution toward fiduciary models. This demographic shift, combined with regulatory momentum, suggests fiduciary financial advice will become the expected standard rather than a distinguishing feature.

Integration of comprehensive services including tax strategies and investment management reflects client demand for coordinated approaches. Fiduciary advisors who offer holistic planning address the reality that financial decisions interconnect in complex ways.

Selecting a fiduciary advisor represents a commitment to receiving guidance aligned with your best interests throughout your financial journey. The legal obligations, transparency requirements, and ethical standards inherent in fiduciary financial advice provide a foundation for confident decision-making across all aspects of your financial life. Brookwood Investment Group LLC serves as a fiduciary partner committed to personalized financial guidance tailored to your unique goals, offering comprehensive services including retirement planning, investment management, estate planning, and tax strategies through a convenient virtual-first model. Whether you're planning for retirement, managing a complex estate, or seeking coordinated financial strategies, working with a fiduciary advisor ensures your interests remain the priority.