If you've found yourself thinking "I need an investment," you're not alone. Many individuals reach a point in their financial journey where they recognize the importance of putting their money to work rather than letting it sit idle. Whether you're planning for retirement, saving for a major life goal, or simply looking to build wealth over time, understanding how to approach investing is a critical step toward financial security. The path forward involves careful planning, education, and often professional guidance to help navigate the complexities of modern financial markets.

Understanding Why You Need an Investment

The realization that "I need an investment" often comes from several common scenarios. Perhaps you've accumulated savings in a traditional bank account and noticed that inflation is eroding your purchasing power faster than interest can accumulate. Or maybe you're approaching a significant life milestone and want to ensure your financial future is secure.

The Impact of Inflation on Savings

Cash savings lose value over time due to inflation. In 2026, with various economic factors at play, the purchasing power of dollars held in low-yield accounts continues to diminish. When you say "I need an investment," you're recognizing that traditional savings alone may not be sufficient to meet your long-term financial objectives.

Key reasons to move beyond savings accounts:

- Inflation consistently outpaces standard savings account interest rates

- Tax-advantaged investment accounts can help reduce your overall tax burden

- Compound growth potential increases substantially over extended time periods

- Diversified investments can provide multiple income streams

Time Horizon and Financial Goals

Your investment timeline significantly influences which strategies and vehicles make sense for your situation. The earlier you start investing, the more time your assets have to benefit from compound returns. This principle applies whether you're in your twenties or approaching retirement.

Consider these common investment timeframes:

- Short-term (1-3 years): Emergency funds, down payment savings, or near-term purchases

- Medium-term (3-10 years): Education funding, business ventures, or major lifestyle changes

- Long-term (10+ years): Retirement planning, wealth building, or legacy creation

Building Your Investment Foundation

When you determine "I need an investment," the next step involves establishing a solid foundation. This means understanding your current financial situation, defining clear objectives, and creating a roadmap that aligns with your risk tolerance and capacity.

Assessing Your Financial Readiness

Before committing capital to investments, evaluate several foundational elements. Do you have adequate emergency savings? Have you addressed high-interest debt? Are you maximizing employer-sponsored retirement contributions? These questions help determine whether you're positioned to invest effectively.

| Financial Checkpoint | Recommended Status | Priority Level |

|---|---|---|

| Emergency Fund | 3-6 months expenses | High |

| High-Interest Debt | Paid down or managed | High |

| Employer Match | Maximized | High |

| Insurance Coverage | Adequate protection | Medium |

| Budget Framework | Established and tracked | Medium |

Many investors benefit from working with professionals who understand fiduciary planning principles, ensuring that recommendations prioritize client interests above all else.

Determining Risk Tolerance

Risk tolerance isn't just about how you feel during market volatility-it's also about your capacity to absorb potential losses without derailing your financial plans. When thinking "I need an investment," matching your emotional comfort with your financial capacity creates a sustainable strategy.

Factors influencing risk tolerance:

- Age and years until retirement

- Income stability and growth potential

- Existing assets and liabilities

- Financial obligations and dependents

- Previous investment experience

Investment Vehicle Options for 2026

The investment landscape in 2026 offers numerous options for those thinking "I need an investment." Understanding the characteristics, benefits, and considerations of each vehicle helps you make informed decisions aligned with your objectives.

Tax-Advantaged Retirement Accounts

Retirement accounts remain one of the most powerful investment tools available. These vehicles offer tax benefits that can significantly enhance long-term wealth accumulation while supporting retirement planning objectives.

Common retirement account types:

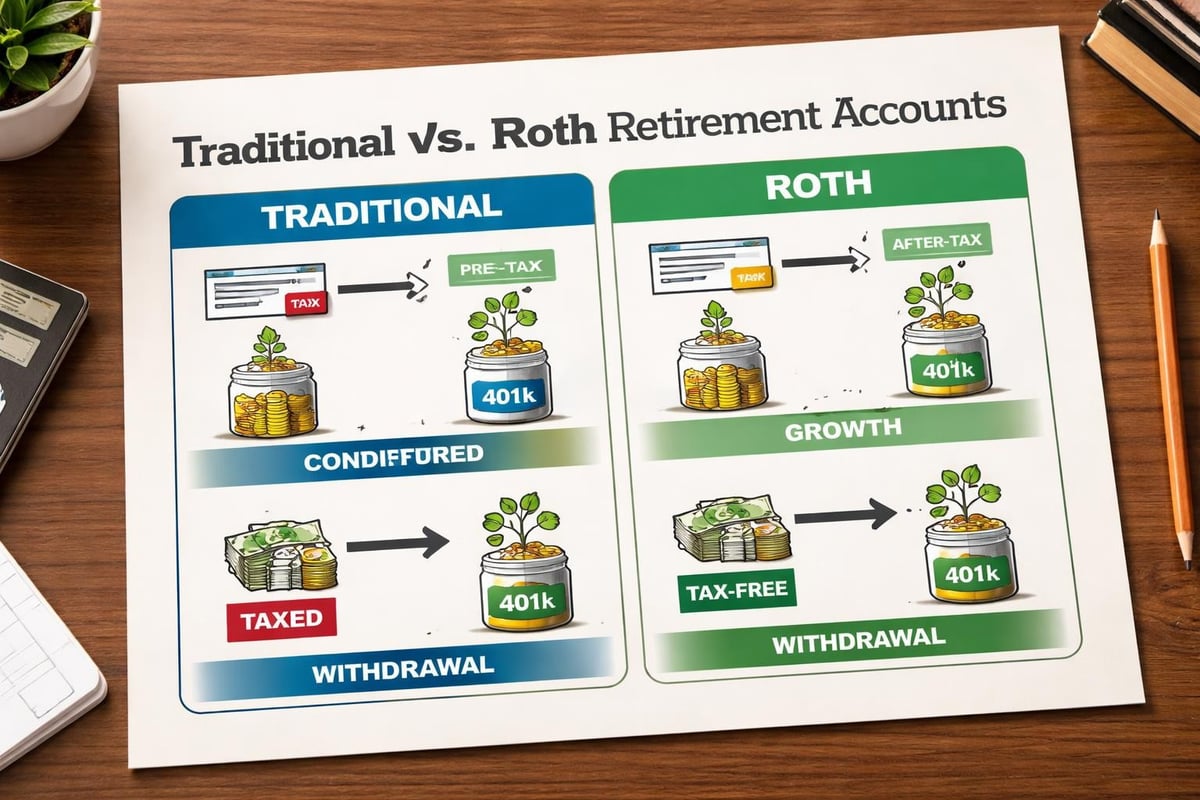

- 401(k) and 403(b): Employer-sponsored plans with potential matching contributions

- Traditional IRA: Tax-deductible contributions with tax-deferred growth

- Roth IRA: After-tax contributions with tax-free qualified withdrawals

- SEP IRA and Solo 401(k): Options for self-employed individuals and business owners

Exchange-Traded Funds and Mutual Funds

For those new to investing, ETFs offer accessible diversification with relatively low costs. These pooled investment vehicles allow you to gain exposure to broad market segments, specific sectors, or particular investment strategies without needing to select individual securities.

| Feature | ETFs | Mutual Funds |

|---|---|---|

| Trading | Throughout market hours | End of day only |

| Minimum Investment | One share price | Often $1,000+ |

| Management Style | Often passive | Active or passive |

| Expense Ratios | Generally lower | Can be higher |

| Tax Efficiency | Typically higher | Varies |

Individual Securities and Bonds

Some investors prefer direct ownership of stocks and bonds, providing greater control over specific holdings. This approach requires more research and monitoring but can be appropriate for those with experience or working with advisors who provide personalized investment management.

When you think "I need an investment" in individual securities, consider how each holding fits within your overall portfolio strategy rather than viewing positions in isolation.

Diversification Strategies That Work

Saying "I need an investment" is just the beginning-building a resilient portfolio requires thoughtful diversification. This principle helps manage risk while pursuing returns across various market conditions and economic cycles.

Asset Class Allocation

Spreading investments across different asset classes provides protection against concentrated risk. Your allocation should reflect your goals, timeline, and risk tolerance while maintaining enough diversification to weather market fluctuations.

Primary asset classes to consider:

- Domestic equities (large-cap, mid-cap, small-cap)

- International equities (developed and emerging markets)

- Fixed income (government bonds, corporate bonds, municipal bonds)

- Real estate investment trusts (REITs)

- Alternative investments (commodities, private equity, hedge funds)

The 5% diversification rule suggests limiting individual positions to prevent overconcentration in any single investment, helping manage portfolio-level risk.

Sector and Geographic Diversification

Beyond asset classes, diversifying across economic sectors and geographic regions provides additional layers of protection. Different sectors perform better during various economic phases, while international exposure can offer growth opportunities outside domestic markets.

When you recognize "I need an investment" strategy that accounts for global dynamics, you're positioning yourself to benefit from opportunities worldwide while reducing country-specific risks.

Working With Professional Advisors

Many individuals who think "I need an investment" eventually realize that professional guidance can provide significant value. While self-directed investing is certainly possible, advisors bring experience, objectivity, and comprehensive planning that individual investors may find challenging to replicate.

The Fiduciary Standard

Working with fiduciary advisors means receiving recommendations that prioritize your best interests. This standard of care provides peace of mind that advice stems from client needs rather than commission structures or proprietary products. Understanding how fiduciary advisors operate helps you evaluate potential advisory relationships.

Comprehensive Financial Planning

Investment management represents just one component of comprehensive financial planning. Advisors who integrate tax strategies, estate planning, insurance analysis, and cash flow management provide holistic guidance that considers your entire financial picture.

Elements of comprehensive planning:

- Cash flow analysis and budgeting

- Investment portfolio construction and monitoring

- Tax optimization strategies

- Risk management and insurance review

- Estate planning coordination

- Retirement income planning

Getting Started: Practical Steps

Once you've decided "I need an investment," taking actionable steps moves you from contemplation to implementation. The process doesn't need to be overwhelming when broken into manageable phases.

Step One: Define Clear Objectives

Specificity matters when setting investment goals. Rather than vague aspirations like "save for retirement," quantify your target: "accumulate $1.5 million by age 65 to support $60,000 annual retirement income." Clear objectives inform appropriate strategies and help measure progress.

Step Two: Educate Yourself

While professional guidance offers tremendous value, understanding basic investment principles empowers better decision-making. Resources like FINRA’s investor education materials provide foundational knowledge for those beginning their investment journey.

Step Three: Choose Your Approach

Decide whether you'll manage investments independently, work with an advisor, or use a hybrid approach. Each path has merits depending on your knowledge, time availability, and complexity of your financial situation. Those seeking professional support might explore comprehensive financial advisory services.

Step Four: Open Appropriate Accounts

Select account types that align with your goals and tax situation. Many people benefit from utilizing multiple account types-such as employer retirement plans, IRAs, and taxable brokerage accounts-to optimize tax efficiency and provide flexibility.

Step Five: Implement Your Strategy

Begin investing according to your plan, whether that means dollar-cost averaging into index funds, building a diversified portfolio of individual securities, or allocating across professionally managed strategies. Various investment strategies can help you align your approach with your objectives.

Monitoring and Adjusting Your Portfolio

After you've addressed "I need an investment" by implementing a strategy, ongoing monitoring ensures your portfolio remains aligned with your goals. Markets change, life circumstances evolve, and periodic review helps maintain appropriate positioning.

Regular Review Schedule

Establish a consistent review cadence rather than constantly reacting to short-term market movements. Quarterly or semi-annual reviews typically provide sufficient frequency for most investors, while major life changes may warrant immediate assessment.

Review checklist items:

- Performance relative to benchmarks and expectations

- Asset allocation drift from target percentages

- Contribution rates and savings progress

- Tax-loss harvesting opportunities

- Rebalancing needs

- Life changes affecting financial plans

Rebalancing Methodology

Over time, different investments grow at varying rates, causing your allocation to shift from your target. Rebalancing involves selling portions of overweight positions and purchasing underweight ones to restore your desired allocation.

| Rebalancing Approach | Description | Best For |

|---|---|---|

| Calendar-based | Rebalance at set intervals | Simple, disciplined approach |

| Threshold-based | Rebalance when allocation drifts X% | Reduces unnecessary trading |

| Hybrid | Combines time and threshold triggers | Balanced monitoring approach |

Staying Disciplined During Volatility

Market downturns test investor resolve. Those who maintain discipline during volatility-continuing contributions and avoiding panic selling-historically achieve better long-term results than those who attempt to time the market.

Tax Considerations for Investors

When thinking "I need an investment," don't overlook tax implications. Different investment vehicles and strategies carry varying tax treatments, and understanding these nuances can significantly impact your after-tax returns.

Tax-Efficient Investment Location

Placing investments in accounts based on their tax characteristics can enhance overall efficiency. Generally, tax-inefficient investments (those generating significant ordinary income or short-term gains) belong in tax-deferred accounts, while tax-efficient holdings can occupy taxable accounts.

Tax-efficient account placement:

- Tax-deferred accounts: Taxable bonds, REITs, actively managed funds

- Tax-free accounts (Roth): High-growth potential investments

- Taxable accounts: Tax-managed funds, municipal bonds, buy-and-hold stocks

Capital Gains Management

Understanding short-term versus long-term capital gains helps optimize tax outcomes. Holding investments for more than one year before selling typically results in preferential long-term capital gains tax rates, which remain lower than ordinary income rates.

Coordination With Overall Tax Planning

Investment decisions shouldn't occur in isolation from broader tax planning. Professional advisors who coordinate investment management with tax strategies help minimize lifetime tax burdens while pursuing financial goals.

Common Mistakes to Avoid

Even well-intentioned investors who recognize "I need an investment" can make missteps that hinder their progress. Awareness of common pitfalls helps you avoid these obstacles on your wealth-building journey.

Waiting for the "Perfect" Time

Market timing rarely works as intended. Those who wait for ideal conditions often miss opportunities as markets advance during periods of waiting. Consistent, disciplined investing typically outperforms attempts to time market entry and exit points.

Overconcentration Risk

Placing too much capital in a single investment, sector, or asset class exposes you to unnecessary risk. Whether it's excessive company stock from your employer or too much exposure to one industry, concentration increases vulnerability to adverse developments.

Ignoring Fees and Expenses

Investment costs directly reduce returns. A seemingly small difference in expense ratios compounds significantly over decades. Understanding all-in costs-including advisory fees, fund expenses, and transaction costs-helps evaluate true investment economics.

Emotional Decision-Making

Fear and greed drive poor investment decisions. Selling during market declines locks in losses, while chasing hot performers often leads to buying high. Maintaining a long-term perspective and following a predetermined strategy helps counter emotional impulses.

The Role of Estate Planning

For those thinking "I need an investment" as part of comprehensive wealth management, estate planning considerations shouldn't be overlooked. How you title accounts, designate beneficiaries, and structure ownership can significantly impact wealth transfer efficiency.

Beneficiary Designations

Retirement accounts and insurance policies pass to designated beneficiaries outside of probate. Regularly reviewing and updating these designations ensures assets transfer according to your wishes. Understanding estate planning advantages helps integrate these considerations into your overall strategy.

Trust Structures

Various trust structures can provide control over asset distribution, offer creditor protection, and potentially reduce estate tax exposure. While not appropriate for everyone, trusts serve valuable purposes for many investors building substantial wealth.

Legacy Planning

Beyond tax efficiency, estate planning allows you to articulate your values and intentions for future generations. This may include charitable giving strategies, educational funding for grandchildren, or specific instructions for asset management and distribution.

Resources for Continued Learning

Investment education doesn't end once you've implemented a strategy. Markets evolve, new products emerge, and your circumstances change. Committing to ongoing learning helps you make informed decisions throughout your investment journey.

Reputable Educational Resources

Seek information from objective, credible sources rather than sensationalized media or conflicted parties. Organizations like FINRA, the SEC, and established financial publications provide valuable educational content for investors at all experience levels.

Professional Development Opportunities

Many investors benefit from periodic educational sessions with their advisors, webinars on specific topics, or workshops addressing timely financial issues. These opportunities complement self-directed learning and help you stay current on relevant developments.

Recognizing that "I need an investment" marks an important step in your financial journey, but transforming that recognition into action requires planning, discipline, and often professional guidance. Whether you're just beginning to invest or looking to optimize an existing portfolio, working with experienced professionals who prioritize your interests can make a meaningful difference in achieving your goals. Brookwood Investment Group LLC offers personalized, fiduciary guidance across investment management, retirement planning, tax strategies, and estate planning-helping you build a comprehensive approach tailored to your unique circumstances and aspirations.