Financial planning and wealth management represent two of the most critical aspects of building a secure future. As we navigate the complexities of 2026's economic landscape, individuals and families face unprecedented challenges in managing retirement accounts, investment portfolios, tax obligations, and estate considerations. The intersection of financial planning and personalized advisory services has evolved dramatically, with fiduciary firms now offering virtual-first approaches that provide accessibility without sacrificing the depth of guidance clients need. Understanding how comprehensive financial strategies work together can mean the difference between financial uncertainty and confident decision-making.

The Foundation of Financial Planning and Strategic Wealth Management

Financial planning and wealth management serve as the cornerstone of achieving long-term financial security. These interconnected disciplines address everything from day-to-day budgeting to complex estate considerations, requiring a holistic approach that considers all aspects of your financial life.

A comprehensive financial strategy examines multiple dimensions simultaneously. Investment management, retirement planning, tax optimization, and estate preservation work together rather than in isolation. According to research from the National Association of Plan Advisors, financial advisors remain the most trusted source for financial guidance, highlighting the value of professional expertise in navigating these complex decisions.

Core Components of Comprehensive Planning

Financial planning and advisory services typically encompass several fundamental areas:

- Retirement strategy development that projects income needs decades into the future

- Investment portfolio management aligned with risk tolerance and time horizons

- Tax efficiency planning to minimize liabilities across different income sources

- Estate preservation to protect assets and ensure smooth wealth transfer

- Insurance analysis to identify gaps in protection coverage

- Cash flow optimization for both short-term needs and long-term goals

The relationship between these components creates synergies that strengthen overall financial health. For instance, retirement account contributions may reduce current tax burdens while simultaneously building future income streams.

Building Your Personalized Financial Strategy

Financial planning and customized approaches differ significantly from one-size-fits-all solutions. Every individual faces unique circumstances, goals, and constraints that demand tailored strategies rather than generic recommendations.

The personalization process begins with comprehensive discovery. Understanding current financial positions, future objectives, family dynamics, and personal values provides the foundation for meaningful recommendations. Brookwood Investment Group’s services exemplify this approach by tailoring guidance to fit unique goals and lifestyles.

Assessment and Goal Setting

| Planning Phase | Key Activities | Expected Outcomes |

|---|---|---|

| Discovery | Financial inventory, goal identification, risk assessment | Clear understanding of current position |

| Analysis | Gap analysis, scenario modeling, strategy development | Actionable recommendations |

| Implementation | Account establishment, portfolio construction, documentation | Active financial plan |

| Monitoring | Performance review, rebalancing, strategy adjustments | Ongoing optimization |

Financial planning and goal alignment require both quantitative analysis and qualitative understanding. While numbers provide objective measures, personal aspirations and concerns shape the most effective strategies. Some clients prioritize leaving legacies for future generations, while others focus on maximizing retirement lifestyle flexibility.

The virtual-first advisory model has transformed accessibility. Clients no longer need to coordinate in-person meetings during business hours, instead connecting with advisors through secure digital platforms that facilitate real-time collaboration regardless of location.

Investment Management Within the Broader Planning Context

Financial planning and investment management represent distinct but deeply connected disciplines. While investment management focuses specifically on portfolio construction and asset allocation, comprehensive planning positions these investments within the broader context of lifetime financial goals.

Modern investment strategies in 2026 incorporate sophisticated approaches to risk management, diversification, and tax efficiency. Portfolios might include traditional stocks and bonds alongside alternative investments, international exposure, and sector-specific allocations based on economic outlooks and individual circumstances.

Strategic Asset Allocation Principles

Investment decisions should always connect back to specific planning objectives. A 35-year-old professional building wealth for retirement decades away requires a fundamentally different allocation than a 65-year-old preparing to transition from accumulation to distribution phases.

Risk tolerance assessment extends beyond simple questionnaires. True understanding requires examining:

- Emotional responses to market volatility

- Capacity to absorb potential losses without lifestyle impacts

- Time horizons for different goal categories

- Income stability and emergency reserves

- Overall financial complexity

Financial planning and portfolio construction benefit from ongoing rebalancing and tax-loss harvesting strategies. These techniques maintain intended risk profiles while potentially reducing tax burdens, demonstrating how investment management and tax planning intersect.

Research into professional financial resources highlights the importance of staying current with evolving investment strategies and market conditions. Professional advisors monitor these developments continuously, adjusting recommendations as circumstances change.

Retirement Planning as the Central Focus

Financial planning and retirement preparation often represent the primary concern for individuals working with advisory firms. The shift from earning active income to relying on accumulated assets requires careful orchestration of multiple income sources and strategic distribution planning.

Retirement planning in 2026 involves navigating complex decisions around Social Security claiming strategies, required minimum distributions, Medicare enrollment, pension elections (when available), and withdrawal sequencing from various account types.

Retirement Income Strategies

Creating reliable retirement income streams requires coordinating several potential sources:

- Social Security benefits optimized through strategic claiming timing

- Employer-sponsored retirement plans including 401(k) and 403(b) accounts

- Individual retirement accounts (Traditional and Roth IRAs) with different tax treatments

- Taxable investment accounts offering flexibility without withdrawal restrictions

- Annuity products potentially providing guaranteed income streams

- Part-time work or consulting supplementing investment income

The sequence of withdrawals from these sources significantly impacts both tax efficiency and portfolio longevity. Financial planning and tax strategy intersect critically in retirement, as strategic approaches can save thousands of dollars annually through thoughtful distribution planning.

Healthcare costs represent one of the largest and most unpredictable retirement expenses. Planning should incorporate projections for premiums, out-of-pocket costs, and potential long-term care needs that Medicare doesn't fully cover.

Estate Planning and Wealth Transfer Strategies

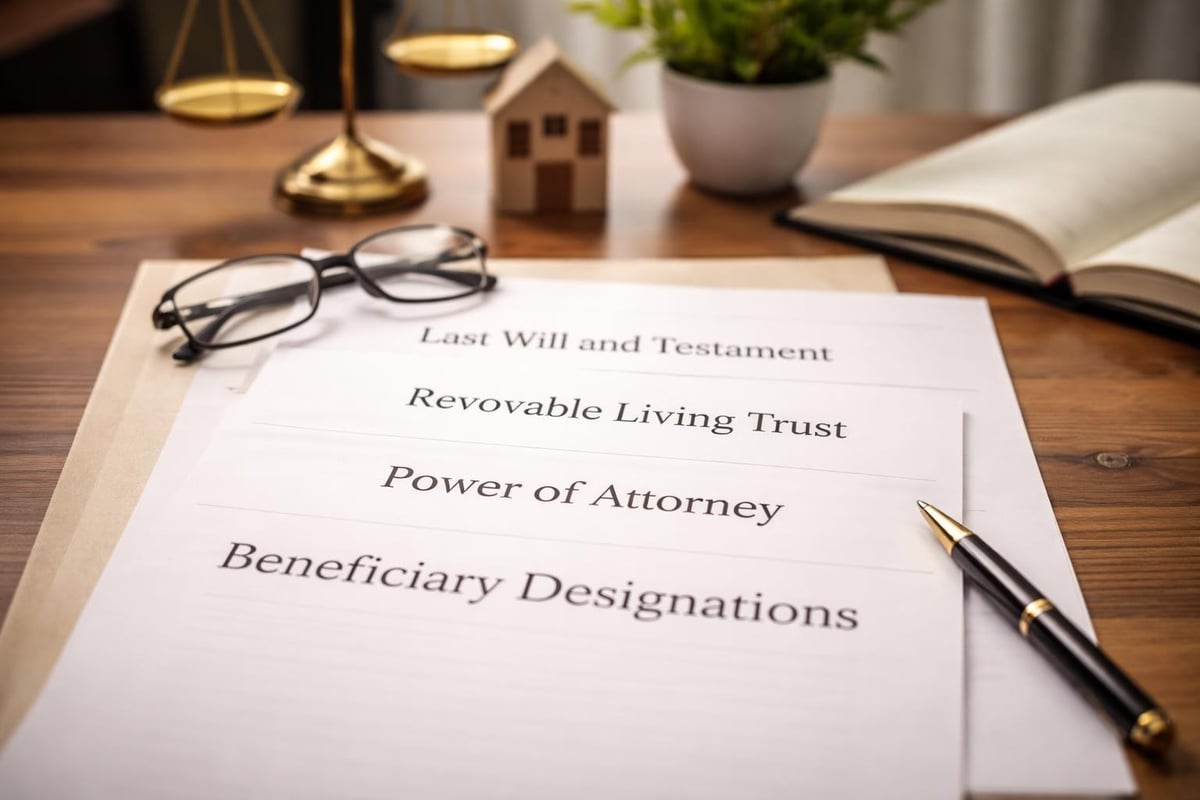

Financial planning and estate considerations ensure that accumulated wealth transfers according to your wishes while minimizing unnecessary tax burdens and administrative complications. Comprehensive estate planning extends beyond simple will creation to encompass trusts, beneficiary designations, power of attorney documents, and healthcare directives.

Many individuals underestimate estate planning importance, assuming it only matters for the ultra-wealthy. In reality, anyone with assets, dependents, or specific wishes about healthcare decisions benefits from proper documentation.

| Estate Planning Tool | Primary Purpose | Typical Use Cases |

|---|---|---|

| Last Will and Testament | Direct asset distribution, name guardians | Foundational document for everyone |

| Revocable Living Trust | Avoid probate, maintain privacy | Larger estates, multiple properties |

| Beneficiary Designations | Direct transfer of specific accounts | Retirement accounts, life insurance |

| Power of Attorney | Financial decision authority | Incapacity planning |

| Healthcare Directive | Medical treatment preferences | End-of-life planning |

Financial planning and estate strategies should coordinate with broader family dynamics and values. Estate planning advantages include reduced family conflict, preserved privacy, and potential tax savings for heirs.

The integration of estate planning with overall financial strategies ensures consistency across all planning documents. Retirement account beneficiaries should align with trust provisions, and asset titling should reflect intended distribution plans. According to the Certified Financial Planner Board, trust remains paramount when selecting financial advisors for these sensitive planning areas.

Tax-Efficient Planning Strategies

Financial planning and tax optimization represent one area where professional guidance delivers measurable value year after year. Strategic tax planning extends far beyond annual return preparation, encompassing retirement contribution strategies, investment account location decisions, and charitable giving approaches.

Year-Round Tax Considerations

Effective tax planning operates throughout the year rather than during a last-minute scramble before filing deadlines. Opportunities for optimization include:

- Roth conversion strategies during lower-income years

- Tax-loss harvesting to offset capital gains

- Charitable contribution bundling using donor-advised funds

- Qualified charitable distributions from IRAs for those over 70½

- Timing of capital gains and income recognition

- Business entity structuring for entrepreneurs and business owners

Working with both financial advisors and CPAs provides comprehensive tax planning that considers both current-year impacts and long-term strategic positioning. These professionals collaborate to identify opportunities that might otherwise go unnoticed.

The relationship between financial planning and tax efficiency becomes particularly important during major life transitions. Job changes, business sales, inheritances, real estate transactions, and retirement timing all create critical tax planning moments that benefit from advance preparation.

Working With Fiduciary Advisors

Financial planning and fiduciary responsibility represent critical considerations when selecting advisory relationships. Fiduciary advisors maintain legal obligations to act in clients' best interests, eliminating many conflicts of interest that can compromise guidance quality.

The distinction between fiduciary and suitability standards matters significantly. Fiduciary advisors must recommend the best available options for client circumstances, not merely products that meet minimum suitability thresholds. This higher standard provides confidence that recommendations prioritize client outcomes over advisor compensation.

Virtual-first advisory models have expanded access to high-quality fiduciary guidance. Geographic limitations no longer restrict your ability to work with advisors whose expertise matches your specific needs. Understanding fiduciary planning helps evaluate potential advisory relationships and ensures alignment between your expectations and advisor obligations.

Evaluating Advisory Services

When considering financial planning and advisory relationships, examine several key factors:

- Fiduciary status and regulatory compliance

- Compensation transparency and fee structures

- Breadth of services and planning depth

- Advisor credentials and continuing education

- Communication frequency and accessibility

- Technology platforms and client experience

- Firm longevity and business stability

Professional designations like Certified Financial Planner (CFP) indicate significant training and ongoing education requirements. Resources from the Financial Planning Association support advisors in maintaining current knowledge across evolving planning disciplines.

The Role of Technology in Modern Planning

Financial planning and technological innovation have converged to enhance both planning accuracy and client experiences. Advanced software platforms enable scenario modeling, Monte Carlo simulations, and real-time portfolio monitoring that were previously unavailable or prohibitively expensive.

Digital tools facilitate collaboration between clients and advisors through secure portals where documents can be shared, accounts aggregated, and progress tracked toward stated goals. This transparency strengthens advisory relationships and enables more informed decision-making.

Artificial intelligence and machine learning now support various planning functions, from portfolio rebalancing algorithms to predictive modeling for retirement outcomes. Academic research into AI integration explores how these technologies can enhance financial advisory services while maintaining the essential human elements of planning relationships.

However, technology serves as an enabler rather than a replacement for professional judgment. Complex financial decisions still benefit from experienced advisors who understand nuanced situations and can provide context that algorithms cannot replicate.

Ongoing Plan Maintenance and Adjustments

Financial planning and continuous monitoring ensure strategies remain aligned with evolving circumstances and objectives. Life rarely proceeds according to initial assumptions, requiring periodic adjustments to maintain plan effectiveness.

Significant life events trigger immediate planning reviews:

- Marriage or divorce

- Birth or adoption of children

- Career changes or business ownership

- Inheritance or windfall

- Major health diagnoses

- Real estate purchases or sales

- Approaching retirement transitions

Even absent major events, annual reviews provide opportunities to assess progress, rebalance portfolios, update assumptions, and refine strategies. Market performance, tax law changes, and evolving personal priorities all influence optimal approaches.

| Review Type | Frequency | Primary Focus Areas |

|---|---|---|

| Comprehensive | Annual | Full plan review, goal progress, strategy adjustments |

| Portfolio | Quarterly | Investment performance, rebalancing needs, allocation |

| Tax Planning | Semi-annual | Year-end projections, optimization opportunities |

| Life Event | As needed | Immediate strategy modifications |

Financial planning and adaptive strategies recognize that flexibility matters as much as initial design. Rigid plans that cannot accommodate life's uncertainties ultimately fail to serve their intended purposes. Accessing ongoing resources supports continuous education and informed decision-making between formal review meetings.

Coordinating Multiple Financial Professionals

Financial planning and professional coordination become increasingly important as financial situations grow more complex. While comprehensive advisory firms provide integrated services, some situations benefit from coordinating multiple specialists including CPAs, estate attorneys, insurance professionals, and business consultants.

Effective coordination prevents conflicting recommendations and ensures all professionals work toward common objectives. Your primary advisor often serves as the quarterback, maintaining communication with other professionals and ensuring strategies complement rather than contradict each other.

This collaborative approach proves particularly valuable for business owners, high-net-worth individuals, and those with complex family situations. The coordination between financial advisors and business planning requires understanding both personal and business financial considerations.

Clear communication protocols and authorized information sharing enable professionals to provide more informed recommendations. When your estate attorney understands your retirement income strategy, they can structure trusts more effectively. When your CPA knows your investment plans, they can provide better tax projections.

Educational Resources and Financial Literacy

Financial planning and ongoing education empower individuals to participate more effectively in planning processes and make informed decisions between advisor meetings. While professional guidance provides valuable expertise, personal financial literacy enhances your ability to evaluate recommendations and understand strategy rationales.

Reputable educational resources help distinguish evidence-based planning principles from speculation or sales pitches. The American Library Association’s financial literacy resources provide trusted content that supports informed decision-making.

Professional organizations and academic institutions offer numerous free educational materials covering investment principles, retirement planning concepts, and estate planning fundamentals. Taking advantage of these resources strengthens your financial knowledge base and enables more productive advisor conversations.

However, education should complement rather than replace professional guidance. Complex financial situations involve numerous variables and interactions that require experienced analysis. Professional editorial guidelines emphasize using authoritative sources and maintaining high standards in financial content creation.

Financial planning and strategic guidance work together to address retirement preparation, investment management, estate preservation, and tax optimization in coordinated ways that maximize long-term outcomes. Understanding how these planning elements interconnect enables more confident decision-making and clearer progress toward your most important financial goals. Brookwood Investment Group offers fiduciary, virtual-first advisory services that provide personalized financial guidance tailored to your unique circumstances, helping you navigate complex decisions with professional expertise dedicated to your best interests.