Finding the right financial guidance can transform your financial future, but with thousands of advisors competing for your attention, identifying truly top rated financial advisors requires understanding what separates exceptional professionals from the rest. The financial advisory landscape has evolved significantly, with virtual-first models and fiduciary standards reshaping how advisors serve clients. Whether you're planning for retirement, managing investments, or developing estate strategies, selecting an advisor who aligns with your goals and operates with transparency can make a substantial difference in achieving long-term financial success.

Understanding What Makes Financial Advisors Top Rated

The designation of top rated financial advisors extends beyond marketing claims. Several objective factors contribute to an advisor's standing in the industry, including professional credentials, client satisfaction metrics, regulatory compliance history, and the breadth of services offered.

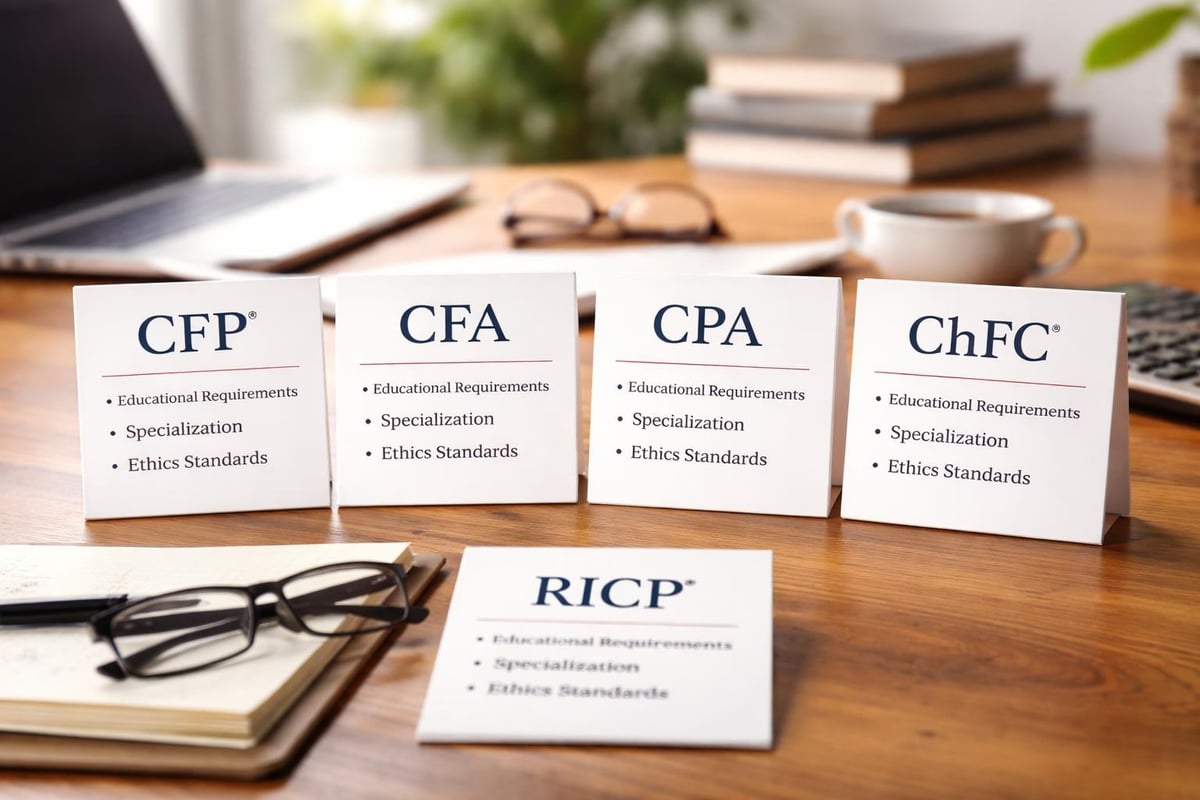

Professional certifications serve as foundational indicators of expertise. Certified Financial Planners (CFP) complete rigorous coursework covering investments, taxes, retirement, estate planning, and insurance. Chartered Financial Analysts (CFA) demonstrate deep investment management knowledge, while Certified Public Accountants (CPA) bring tax expertise to the table. Many top rated wealth management firms employ professionals with multiple credentials to provide comprehensive guidance.

Key Credentials to Look For

When evaluating potential advisors, certain qualifications indicate advanced training and ongoing education:

- CFP (Certified Financial Planner): Requires extensive education, examination, experience, and ethics commitments

- CFA (Chartered Financial Analyst): Focuses on investment management and portfolio strategy

- CPA (Certified Public Accountant): Brings tax planning and accounting expertise

- ChFC (Chartered Financial Consultant): Covers comprehensive financial planning topics

- RICP (Retirement Income Certified Professional): Specializes in retirement income strategies

According to CNBC’s Financial Advisor 100 for 2025, the highest-ranked firms consistently employ advisors with multiple advanced certifications, reflecting their commitment to professional development and client service excellence.

The Fiduciary Standard: A Non-Negotiable Requirement

One of the most critical distinctions separating top rated financial advisors from others involves their legal obligation to clients. Fiduciary advisors must act in their clients' best interests at all times, placing client needs above their own financial gain. This contrasts with the suitability standard, which only requires recommendations to be suitable rather than optimal.

Fiduciary commitment manifests in several concrete ways. Fee-only advisors eliminate conflicts of interest by charging transparent fees rather than earning commissions on product sales. They disclose all potential conflicts and provide clear documentation of their compensation structure. Fiduciary planning ensures that every recommendation prioritizes client objectives without hidden incentives influencing the guidance provided.

Why Fee Structure Matters

| Fee Type | How It Works | Potential Conflicts |

|---|---|---|

| Fee-Only | Flat fee, hourly rate, or percentage of assets | Minimal conflicts; advisor compensated directly by client |

| Commission-Based | Earns commissions on products sold | May incentivize product recommendations |

| Fee-Based | Combination of fees and commissions | Mixed incentives requiring careful evaluation |

Transparency in compensation creates trust and alignment between advisors and clients. When researching financial advisors independent of product manufacturers, you'll often find clearer fee disclosures and fewer conflicts of interest.

Services That Define Comprehensive Advisory

Top rated financial advisors offer integrated services that address multiple dimensions of financial wellness. Rather than focusing exclusively on investments or insurance, comprehensive advisors coordinate various planning elements into cohesive strategies.

Retirement planning forms the cornerstone of most advisory relationships. This includes analyzing income sources, projecting expenses, optimizing Social Security claiming strategies, and developing withdrawal plans that balance current needs with long-term sustainability. Effective retirement planning and estate planning work together to ensure wealth transfers according to client wishes while minimizing tax burdens.

Investment management extends beyond simple asset allocation. Top advisors conduct thorough risk assessments, rebalance portfolios systematically, implement tax-loss harvesting strategies, and adjust allocations as client circumstances evolve. They consider both traditional investments and alternative assets when appropriate for client goals.

Comprehensive Service Offerings

A truly integrated approach includes:

- Financial planning: Goal setting, cash flow analysis, and scenario modeling

- Investment management: Portfolio construction, ongoing monitoring, and performance reporting

- Retirement planning: Income strategies, healthcare planning, and longevity risk management

- Estate planning coordination: Working with attorneys on wills, trusts, and beneficiary designations

- Tax strategy: Collaborating with CPAs or providing in-house tax guidance

- Risk management: Insurance analysis and protection planning

NerdWallet’s 2026 list of the 9 Best Financial Advisors highlights firms that excel across multiple service categories rather than specializing narrowly.

Technology and Accessibility in Modern Advisory

The shift toward virtual-first advisory models has expanded access to top rated financial advisors regardless of geographic location. Technology enables more frequent communication, real-time portfolio monitoring, and efficient document sharing while often reducing overhead costs that might otherwise be passed to clients.

Virtual platforms don't sacrifice personalization for convenience. Video conferencing allows face-to-face meetings without travel requirements. Secure client portals provide 24/7 access to account information, financial plans, and relevant documents. Digital signatures expedite paperwork that once required in-person meetings.

However, technology should enhance rather than replace human expertise. The best virtual-first advisors combine sophisticated planning software with personalized guidance tailored to individual circumstances. They use technology to increase efficiency in data gathering and analysis, freeing more time for strategic conversations about client goals and concerns.

Questions to Ask When Evaluating Advisors

Before committing to an advisory relationship, thorough due diligence protects your interests and ensures alignment with your needs. The right questions reveal not only qualifications but also compatibility and approach.

Regulatory background provides objective information about an advisor's history. You can verify credentials through FINRA BrokerCheck or the SEC's Investment Adviser Public Disclosure database. These resources reveal any disciplinary actions, customer complaints, or regulatory issues.

Essential Questions for Prospective Advisors

- Are you a fiduciary 100% of the time?

- How are you compensated, and what are your total fees?

- What credentials and certifications do you hold?

- What is your investment philosophy and planning approach?

- How often will we meet, and how do you communicate between meetings?

- What services are included in your fee?

- Do you provide tax planning or coordinate with my CPA?

- How do you measure success in client relationships?

Bankrate’s Best Financial Advisors of 2026 emphasizes the importance of understanding an advisor's planning philosophy before making commitments.

Client-Centric Approaches and Personalization

Top rated financial advisors recognize that cookie-cutter strategies rarely serve clients effectively. Personalization begins with comprehensive discovery, exploring not just financial data but life goals, risk tolerance, values, and family dynamics.

Customized planning considers unique circumstances that generic advice overlooks. A business owner approaching retirement faces different challenges than a corporate executive. Someone planning to relocate internationally requires different strategies than someone aging in place. Financial advisor for business owners services address succession planning, concentrated stock positions, and business valuation considerations that don't apply to W-2 employees.

Ongoing relationships require periodic reassessment as circumstances change. Marriage, divorce, inheritance, career transitions, health issues, or market volatility all trigger the need for plan adjustments. Advisors who proactively reach out during major life events or market turbulence demonstrate client-centered commitment.

Red Flags and Warning Signs

While identifying top performers matters, recognizing advisors to avoid protects you from costly mistakes. Several warning signs indicate potential problems worth investigating further.

Pressure tactics suggest misaligned priorities. Legitimate advisors allow time for decision-making and never rush clients into investments or strategies. Similarly, guaranteed returns or promises of specific performance violate securities regulations and indicate dishonesty, as markets contain inherent uncertainty that no advisor can eliminate.

Warning Signs to Watch For

| Red Flag | Why It Matters |

|---|---|

| Unlicensed or unregistered | Operating outside regulatory oversight |

| Vague fee disclosures | Hidden costs reduce your returns |

| Performance guarantees | Violates securities laws; unrealistic promises |

| High-pressure sales tactics | Prioritizes advisor's interests over yours |

| Lack of fiduciary commitment | May recommend products benefiting them |

| Poor communication | Indicates service issues ahead |

Reviewing an advisor's Form ADV (for registered investment advisors) provides detailed information about their business practices, conflicts of interest, and disciplinary history. This document is publicly available and should be reviewed carefully before engaging services.

The Value of Independence and Objectivity

Many top rated financial advisors operate independently rather than being tied to specific product manufacturers or large financial institutions. This independence enables objective recommendations based solely on client needs rather than internal sales quotas or preferred product lists.

Independent advisors access a broader universe of investment options and insurance products. They can compare offerings from multiple providers to identify solutions with optimal fee structures, performance characteristics, and features. This contrasts with captive advisors limited to proprietary products that may not serve client interests as effectively.

The financial consulting company model emphasizes personalized strategies over product sales, aligning advisor success with client outcomes rather than commission generation. This structural alignment creates natural incentives for advisors to prioritize long-term client relationships over short-term transactions.

Specialization and Niche Expertise

While comprehensive services matter, some top rated financial advisors develop specialized expertise serving specific client segments. This focused approach allows deeper knowledge of unique challenges facing particular groups.

High-net-worth clients benefit from advisors experienced with complex estate planning, multigenerational wealth transfer, alternative investments, and tax optimization strategies. High networth financial advisors understand trust structures, charitable giving vehicles, and sophisticated planning techniques relevant to substantial wealth.

Other specializations include serving retirees transitioning from accumulation to distribution, healthcare professionals managing student debt alongside wealth building, or expatriates navigating international tax treaties and cross-border financial planning. When your situation includes unique complexity, specialized expertise often delivers superior outcomes compared to generalist approaches.

Technology Integration and Security

As advisory relationships increasingly occur virtually, cybersecurity and data protection become paramount considerations. Top rated financial advisors implement robust security measures protecting sensitive client information from unauthorized access or data breaches.

Secure systems include encrypted communications, multi-factor authentication, regular security audits, and employee training on data protection protocols. Advisors should clearly explain their security measures and provide policies governing data storage, sharing, and retention.

Beyond security, technology should enhance the client experience through user-friendly portals, mobile access, and intuitive reporting. The best platforms present complex financial information in digestible formats, allowing clients to understand their financial picture without requiring advanced financial knowledge.

Measuring Advisor Performance and Value

Evaluating an advisor's performance extends beyond simple investment returns. While portfolio performance matters, comprehensive value includes tax savings, planning guidance, behavioral coaching, and coordination of complex financial matters.

Holistic value assessment considers multiple factors:

- Risk-adjusted returns: How portfolio performance compares to appropriate benchmarks given your risk tolerance

- Tax efficiency: Strategies implemented to minimize tax burden

- Planning quality: Thoroughness of financial plans and recommendations

- Responsiveness: Timeliness and quality of communications

- Fee competitiveness: Whether fees align with services received

- Goal achievement: Progress toward stated financial objectives

According to CNBC’s FA 100 ranking for 2024, the highest-rated firms demonstrate consistent performance across multiple evaluation criteria rather than excelling in only one dimension.

The Role of Ongoing Education and Development

Financial markets, tax laws, and planning strategies evolve continuously. Top rated financial advisors commit to ongoing professional development, ensuring their knowledge remains current and relevant to client needs.

Continuing education requirements vary by credential, but leading advisors exceed minimum standards. They attend industry conferences, pursue additional certifications, participate in study groups, and stay informed about legislative changes affecting financial planning.

This commitment to learning benefits clients directly through more sophisticated strategies, awareness of new planning opportunities, and proactive adjustments when regulations change. Advisors who view education as ongoing rather than complete upon initial certification typically provide higher-quality guidance throughout long-term relationships.

Building Long-Term Advisory Relationships

The greatest value from working with top rated financial advisors emerges over time through consistent guidance, relationship depth, and accumulated knowledge of your unique situation. Short-term thinking rarely serves long-term financial goals effectively.

Relationship continuity enables advisors to understand family dynamics, personal values, risk tolerance nuances, and goal evolution that aren't evident in initial meetings. This depth of understanding allows more personalized recommendations and proactive outreach during relevant life events.

Long-term relationships also facilitate behavioral coaching during market volatility. When advisors know clients well, they can provide perspective and encouragement that prevents emotional decisions undermining long-term strategies. This behavioral value often exceeds the impact of investment selection or tactical allocation adjustments.

Questions About Advisory Firm Structure

The organizational structure of an advisory firm influences service delivery, continuity, and scalability. Understanding whether you're working with a solo practitioner, small team, or larger organization helps set appropriate expectations.

Solo practitioners offer highly personalized service but may face challenges with continuity if illness or vacation interrupts availability. Small teams often provide the ideal balance of personalized attention with backup coverage and diverse expertise. Larger firms deliver systematic processes and deep specialist resources but may feel less personal.

Consider succession planning as well. If your advisor is approaching retirement, does the firm have plans ensuring service continuity? Firms with documented succession strategies protect client relationships during ownership transitions.

Selecting among top rated financial advisors requires evaluating credentials, fiduciary commitment, service breadth, and personal compatibility to ensure alignment with your unique goals and circumstances. The investment in finding the right advisor pays dividends through decades of informed guidance, tax-efficient strategies, and coordinated planning across all aspects of your financial life. Brookwood Investment Group LLC operates as a fiduciary, virtual-first advisory firm providing personalized retirement planning, investment management, estate planning, and tax strategies tailored to your unique lifestyle and objectives, helping you navigate complex financial decisions with clarity and confidence.