Finding the right financial guidance can transform your financial future, but identifying the best financial advisors requires understanding what separates exceptional professionals from the rest. The financial advisory landscape has evolved significantly, with virtual-first firms, fee-only models, and specialized services becoming increasingly prevalent. Whether you're planning for retirement, managing investments, or navigating complex tax strategies, selecting an advisor who aligns with your goals and values is one of the most important financial decisions you'll make. This guide explores the essential characteristics, credentials, and questions that will help you identify top-tier financial professionals.

Understanding What Makes the Best Financial Advisors

The best financial advisors share common attributes that distinguish them from average practitioners. These professionals demonstrate deep expertise across multiple financial disciplines while maintaining unwavering commitment to their clients' interests.

Fiduciary responsibility stands as the cornerstone of exceptional financial advice. Advisors who operate under the fiduciary standard are legally obligated to act in your best interests at all times, eliminating conflicts of interest that can compromise the quality of guidance. This commitment means recommendations are based solely on what benefits you, not what generates higher commissions or fees for the advisor.

Transparency in fee structure represents another hallmark of top advisors. The best financial advisors clearly communicate how they're compensated, whether through assets under management (AUM) fees, flat fees, hourly rates, or retainer arrangements. Fee-only advisors typically avoid commission-based products, reducing potential conflicts and ensuring alignment with client objectives.

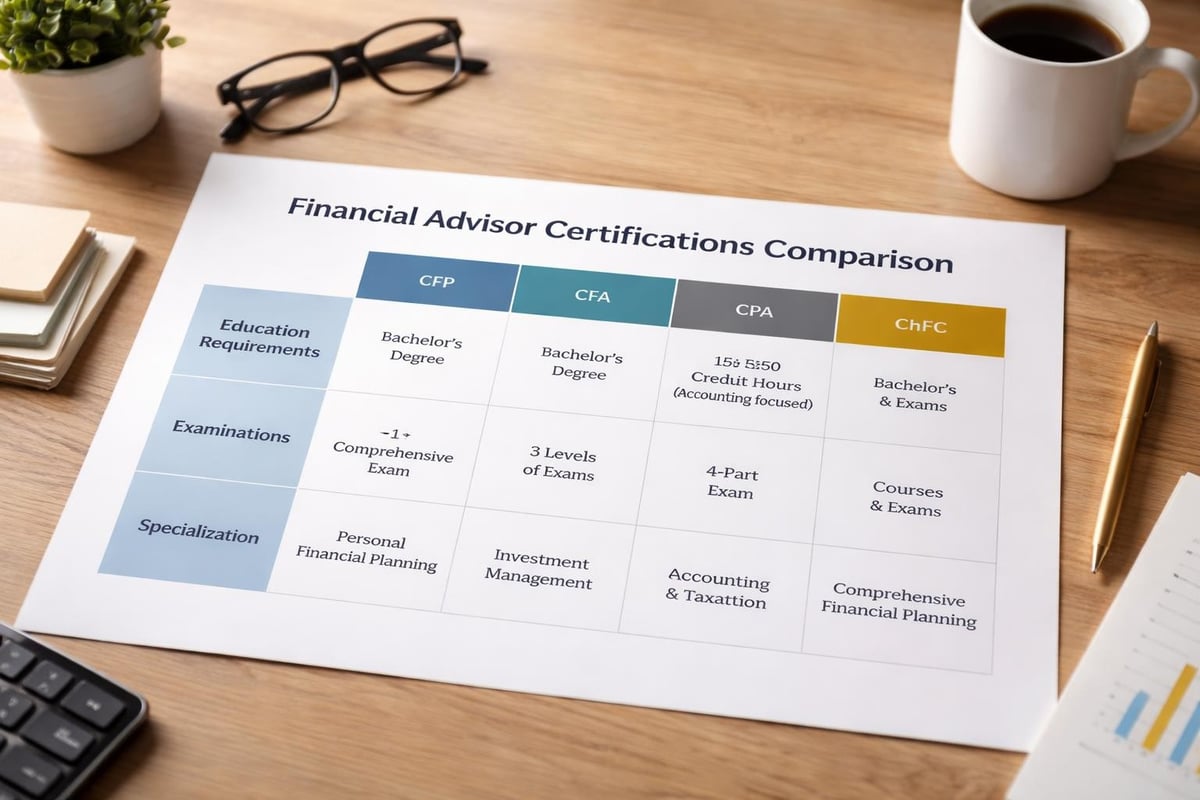

Key Credentials and Qualifications

Professional designations signal an advisor's commitment to education and ethical standards. The CERTIFIED FINANCIAL PLANNER™ (CFP®) designation requires extensive coursework, examination, experience, and adherence to strict ethical guidelines. Chartered Financial Analyst (CFA) credentials demonstrate expertise in investment analysis and portfolio management.

Additional certifications include:

- Certified Public Accountant (CPA) for tax planning expertise

- Chartered Financial Consultant (ChFC) for comprehensive financial planning

- Certified Estate Planner (CEP) for wealth transfer strategies

- Retirement Income Certified Professional (RICP) for retirement planning

These credentials indicate that advisors have invested significant time and resources into their professional development, which often translates into more sophisticated strategies and deeper insights for clients.

Evaluating Service Offerings and Specializations

The best financial advisors provide comprehensive services that address multiple aspects of your financial life. Rather than focusing narrowly on investment management, top professionals take a holistic approach that integrates various planning disciplines.

Comprehensive financial planning encompasses retirement planning, investment management, tax optimization, estate planning, insurance analysis, and cash flow management. This integrated approach ensures all financial decisions work together toward your long-term objectives rather than existing in isolation.

When evaluating service offerings, consider whether an advisor can address your specific needs:

| Service Area | What to Look For | Why It Matters |

|---|---|---|

| Retirement Planning | Withdrawal strategies, Social Security optimization, pension analysis | Ensures sustainable income throughout retirement |

| Investment Management | Asset allocation, portfolio rebalancing, risk management | Aligns investments with goals and risk tolerance |

| Tax Planning | Tax-loss harvesting, Roth conversions, charitable giving | Minimizes tax burden and maximizes after-tax returns |

| Estate Planning | Wealth transfer, beneficiary planning, trust strategies | Protects assets and ensures smooth wealth transition |

Virtual-First Advisory Models

The shift toward virtual financial advisory services has expanded access to quality guidance while reducing overhead costs. Virtual-first firms leverage technology to provide personalized service regardless of geographic location, offering scheduling flexibility and efficient communication tools.

This model particularly benefits clients who value convenience and appreciate digital tools for tracking progress and accessing financial information. However, the best financial advisors in this space maintain the personal touch through regular video conferences, responsive communication, and customized planning regardless of delivery method.

Fee Structures and Cost Considerations

Understanding advisor compensation structures is essential for making informed decisions. Different fee models create varying incentive structures that can impact the guidance you receive.

Assets Under Management (AUM) fees typically range from 0.5% to 2% annually, with larger portfolios often qualifying for reduced rates. This model aligns advisor compensation with portfolio growth but can become expensive as assets increase. For comprehensive guidance on evaluating different compensation models, Kiplinger’s analysis of thinking like Warren Buffett about financial advice costs provides valuable perspective.

Fee-only advisors may charge flat annual fees, hourly rates, or project-based fees. These structures can be more predictable and eliminate commission-based conflicts, though they require direct payment rather than being deducted from investment accounts.

Commission-based advisors earn compensation through product sales. While this can reduce out-of-pocket costs, it may create incentives to recommend products that generate higher commissions rather than those best suited to your needs. Understanding whether an advisor operates under a fiduciary standard becomes particularly important in these arrangements, as discussed in Kiplinger’s guide to confirming fiduciary commitment.

Minimum Investment Requirements

Many top advisory firms establish minimum portfolio sizes, often ranging from $100,000 to $1 million or more. These minimums help firms maintain profitability while delivering comprehensive services. However, several excellent advisors serve clients with smaller portfolios, recognizing that early-career professionals and younger investors benefit significantly from professional guidance.

Virtual-first advisory models often feature lower minimums since reduced overhead allows profitability at smaller account sizes. Some firms offer tiered service levels, with basic planning available at lower minimums and comprehensive wealth management reserved for larger portfolios.

The Selection Process: Research and Due Diligence

Identifying the best financial advisors requires thorough research and careful vetting. This process protects your financial interests and increases the likelihood of a productive long-term relationship.

Start by verifying credentials and regulatory history through public databases. The Securities and Exchange Commission's Investment Adviser Public Disclosure (IAPD) website provides information about registered investment advisors, including disciplinary history, credentials, and business practices. The Financial Industry Regulatory Authority (FINRA) maintains BrokerCheck for broker-dealer representatives.

For detailed guidance on vetting potential advisors, Kiplinger’s eight essential rules for choosing a financial advisor offers comprehensive steps to ensure you select a qualified professional.

Essential Questions to Ask

Interview multiple advisors before making a decision. The best financial advisors welcome questions and provide clear, detailed responses about their approach, qualifications, and services.

Critical questions include:

- Are you a fiduciary 100% of the time when providing financial advice?

- How are you compensated, and are there any potential conflicts of interest?

- What credentials and licenses do you hold?

- What is your investment philosophy and approach to financial planning?

- How often will we meet, and what ongoing communication can I expect?

- What is your typical client profile, and do you have experience with situations similar to mine?

- How do you measure success, and what benchmarks do you use?

- Who else will work on my account, and what are their qualifications?

Pay attention not only to the answers but also to how comfortably and transparently advisors address these topics. Evasiveness or reluctance to discuss fees and conflicts should raise concerns.

Industry Rankings and Recognition

Various publications compile annual rankings of top advisory firms based on factors including assets under management, growth, client satisfaction, and regulatory compliance. While these lists shouldn't be your sole selection criteria, they provide useful starting points for research.

CNBC’s Financial Advisor 100 list for 2025 highlights leading firms based on quantitative metrics and qualitative assessments. Similarly, NerdWallet’s analysis of the best financial advisors provides detailed comparisons of services, fees, and client suitability.

These rankings offer valuable information about firms' scale, specializations, and reputations, but individual fit matters more than industry recognition. A highly ranked firm may not align with your specific needs, while a smaller boutique practice might provide exactly the personalized attention and specialized expertise you require.

Understanding Assets Under Management

Assets under management (AUM) indicates a firm's scale but doesn't necessarily correlate with service quality. Large firms with billions in AUM benefit from resources, research capabilities, and stability. However, they may provide less personalized attention and maintain higher minimums.

Smaller firms often deliver more customized service, greater flexibility, and closer advisor relationships. The best financial advisors compared by Bankrate include both large and boutique firms, demonstrating that excellence exists across different firm sizes.

| Firm Size | Typical Advantages | Potential Considerations |

|---|---|---|

| Large (Multi-billion AUM) | Extensive resources, research teams, institutional pricing | Higher minimums, less personalization, multiple team members |

| Mid-size (Hundreds of millions) | Balanced resources and personal attention, specialized services | May have minimum requirements, growth can affect service |

| Boutique (Under $100 million) | Highly personalized service, direct principal access, flexibility | Limited resources, potential succession questions |

Specialized Expertise and Niche Services

The best financial advisors often develop specialized expertise in particular client segments or financial situations. This specialization allows deeper understanding of unique challenges and more sophisticated solutions.

Common specialization areas include:

- Business owners and entrepreneurs requiring succession planning and exit strategies

- Medical professionals navigating student debt, practice ownership, and malpractice considerations

- Executives managing stock options, deferred compensation, and concentrated stock positions

- Retirees optimizing withdrawal strategies and managing longevity risk

- Multi-generational wealth families coordinating estate planning and family governance

Working with an advisor experienced in your specific situation can provide significant value. For instance, business owners benefit from advisors familiar with financial planning for entrepreneurs and business exit strategies, while those with complex estates need expertise in comprehensive estate planning approaches.

Tax-Planning Integration

Tax efficiency significantly impacts long-term wealth accumulation. The best financial advisors either possess tax expertise themselves or maintain close relationships with qualified tax professionals to ensure coordinated strategies.

Effective tax planning encompasses retirement account optimization, tax-loss harvesting, Roth conversion analysis, charitable giving strategies, and estate tax mitigation. Advisors who collaborate with CPAs can provide integrated guidance that considers both financial planning and tax implications simultaneously.

Technology and Client Experience

Modern financial advisory incorporates sophisticated technology for portfolio management, financial planning, and client communication. The best financial advisors leverage these tools to enhance service quality while maintaining the personal relationships that define successful advisory partnerships.

Client portal technology provides 24/7 access to account information, performance reporting, and financial planning documents. These platforms offer transparency and convenience, allowing you to monitor progress between meetings and access important information when needed.

Financial planning software enables comprehensive scenario analysis, retirement projections, and tax planning. Advanced tools model various strategies, helping you visualize potential outcomes and make informed decisions about complex financial questions.

Communication platforms facilitate video conferences, secure document sharing, and regular updates. Virtual-first firms excel at using these technologies to deliver personalized service regardless of geographic distance, as demonstrated by firms like Brookwood Investment Group that combine technology with customized guidance.

Building Long-Term Advisory Relationships

The relationship with your financial advisor should evolve with your changing circumstances, goals, and life stages. The best financial advisors recognize that effective guidance requires understanding not just your financial situation but also your values, priorities, and aspirations.

Ongoing communication forms the foundation of successful relationships. Regular reviews ensure your financial plan remains aligned with current circumstances and goals. Life events like career changes, inheritance, divorce, or health issues necessitate plan adjustments that responsive advisors address proactively.

Transparency during challenging market periods demonstrates advisor quality. The best financial advisors maintain consistent communication during volatility, providing context, perspective, and reassurance based on your long-term plan rather than emotional reactions to short-term market movements.

Measuring Advisor Performance

Evaluating your advisor's performance extends beyond investment returns. While portfolio performance matters, comprehensive assessment considers planning value, responsiveness, proactive communication, and progress toward your specific goals.

Consider these performance indicators:

- Achievement of financial milestones and goals

- Tax efficiency of investment strategies

- Quality and timeliness of communication

- Proactive planning recommendations

- Risk-adjusted portfolio returns relative to appropriate benchmarks

- Service experience and overall relationship satisfaction

The best financial advisors establish clear expectations, define success metrics aligned with your objectives, and regularly review progress against these benchmarks. This accountability ensures both parties remain focused on what matters most to your financial future.

Red Flags and Warning Signs

Recognizing problematic advisor characteristics protects you from poor guidance and potential misconduct. Certain behaviors should prompt immediate reconsideration of an advisory relationship.

Guaranteed returns or unrealistic promises violate fundamental investment principles and may indicate fraudulent activity. No advisor can guarantee specific returns, and those making such promises should be avoided entirely. All investments involve risk, and the best financial advisors communicate clearly about potential outcomes, including downside scenarios.

Pressure tactics or rushed decisions conflict with thoughtful financial planning. Quality advisors encourage careful consideration, welcome questions, and never pressure clients into hasty choices. High-pressure sales approaches prioritize advisor interests over client wellbeing.

Lack of transparency about fees, conflicts, or investment strategies suggests problematic practices. The best financial advisors readily disclose all relevant information and welcome scrutiny of their recommendations, compensation, and business practices.

Overly complex strategies that you don't understand may indicate inappropriate recommendations. While sophisticated planning has its place, advisors should explain strategies clearly and ensure you comprehend both the approach and its rationale before implementation.

Independent Advisors Versus Captive Firms

The distinction between independent advisors and those affiliated with large financial institutions impacts the guidance you receive. Understanding these differences helps you select an advisor whose business model aligns with your preferences.

Independent advisors operate their own practices or join independent broker-dealers and Registered Investment Advisors (RIAs). This independence typically allows broader product access, greater flexibility in recommendations, and fewer corporate mandates affecting client service. Many independent financial advisors emphasize fiduciary responsibility and fee-only compensation.

Captive or employed advisors work for banks, insurance companies, or wirehouse brokerage firms. While these advisors can be highly qualified, they may face pressure to recommend proprietary products or meet sales targets that create conflicts of interest.

Neither model guarantees superior service, but understanding the structure helps you ask appropriate questions about potential conflicts and recommendation constraints. The best financial advisors, regardless of affiliation, prioritize client interests and maintain transparency about any limitations their business model creates.

Selecting from among the best financial advisors requires careful evaluation of credentials, fee structures, service offerings, and personal fit. The right advisor acts as a fiduciary, communicates transparently, and aligns their expertise with your specific financial needs and goals. As a fiduciary, virtual-first advisory firm, Brookwood Investment Group offers personalized financial guidance including retirement planning, investment management, estate planning, and tax strategies tailored to your unique situation. Connect with our team to explore how comprehensive, client-centered financial planning can help you achieve your financial objectives.