Navigating your financial future can feel overwhelming, especially when you're unsure whether you need professional guidance or where to start without breaking the bank. Financial advisor free advice exists in more forms than many people realize, ranging from complimentary initial consultations with fiduciary advisors to government-sponsored programs and employer benefits. Understanding where to find legitimate, quality guidance at no cost helps you make informed decisions about your money while determining whether ongoing professional support aligns with your goals. This guide explores the landscape of free financial resources available to individuals seeking expert perspectives on retirement planning, investment strategies, and wealth management.

Understanding What Constitutes Free Financial Advice

Financial advisor free advice comes in various formats, each serving different purposes and offering distinct levels of value. The term encompasses everything from brief educational consultations to comprehensive initial assessments that help you understand your current financial position.

Complimentary Initial Consultations

Many fiduciary advisory firms, including virtual-first practices, offer no-obligation introductory meetings where potential clients can discuss their financial situations. These sessions typically last 30 to 60 minutes and provide an opportunity to:

- Review your current financial landscape

- Identify immediate concerns or opportunities

- Understand the advisor's approach and philosophy

- Determine whether ongoing services would benefit your situation

These consultations serve a dual purpose. You receive professional insights into your finances, while the advisor assesses whether you're a good fit for their practice. This mutual evaluation ensures both parties can make informed decisions about working together.

Educational Content and Resources

Financial professionals frequently publish educational materials designed to help individuals understand complex topics. These resources include:

- Webinars covering retirement planning strategies

- Blog articles explaining investment concepts

- Email newsletters with tax-saving tips

- Podcasts discussing estate planning considerations

This type of financial advisor free advice serves to educate rather than provide personalized recommendations. While valuable for building knowledge, it differs from tailored guidance specific to your circumstances.

Where to Access Legitimate Free Financial Guidance

Multiple channels exist for obtaining quality financial information and preliminary advice without cost. Several reputable sources provide free financial advice through various platforms and programs.

Employer-Sponsored Programs

Many companies partner with financial wellness providers to offer employees access to financial education and guidance. These programs may include:

| Program Type | Typical Features | Best Used For |

|---|---|---|

| Retirement Plan Support | 401(k) education, contribution guidance | Understanding employer retirement benefits |

| Financial Wellness Platforms | Budgeting tools, debt calculators, planning resources | Building foundational financial knowledge |

| One-on-One Consultations | Sessions with CFP professionals | Specific questions about workplace benefits |

Your human resources department can provide details about available programs. These benefits represent a valuable component of your total compensation package.

Government and Nonprofit Resources

Federal and state agencies offer free financial counseling services to citizens. The Financial Counseling Association of America maintains a network of certified counselors who provide guidance on budgeting, debt management, and credit improvement.

Additionally, government resources and HUD-approved counselors can assist with housing-related financial decisions and homeownership education. These services particularly benefit first-time homebuyers or individuals facing financial hardship.

Bank and Credit Union Services

Financial institutions increasingly provide complimentary financial planning services to customers. These offerings vary by institution but commonly include:

- Retirement planning calculators

- Meetings with in-house financial advisors

- Educational workshops on various topics

- Portfolio review services for investment account holders

The quality and comprehensiveness of these services differ significantly between institutions. Some banks offer robust advisory services, while others provide only basic educational materials.

Online Financial Planning Tools

The digital landscape has expanded access to financial guidance considerably. Digital resources and budgeting applications now offer sophisticated features that were once available only through paid advisory relationships.

These platforms typically provide:

- Automated budget tracking and analysis

- Investment portfolio recommendations

- Retirement savings projections

- Debt payoff calculators and strategies

While these tools offer valuable insights, they lack the personalized judgment that comes from working with a human advisor who understands your complete financial picture and life goals.

Evaluating the Quality of Free Financial Advice

Not all financial advisor free advice carries equal weight or reliability. Developing criteria to assess the guidance you receive helps you make sound decisions based on credible information.

Credentials and Qualifications Matter

When seeking advice, verify the credentials of the person providing it. Look for designations such as:

- Certified Financial Planner (CFP)

- Chartered Financial Analyst (CFA)

- Certified Public Accountant (CPA)

These credentials indicate the advisor has completed rigorous education, passed comprehensive examinations, and adheres to ethical standards. Understanding fiduciary advisory services helps you recognize advisors legally obligated to act in your best interest.

Transparency About Limitations

Quality free advice comes with clear boundaries. Reputable advisors will explain what they can and cannot address during a complimentary session. They'll distinguish between general education and specific recommendations that require a formal advisory relationship.

Be cautious of anyone offering definitive investment recommendations or detailed financial plans without fully understanding your situation or establishing a client relationship. Comprehensive financial planning requires extensive information gathering and analysis.

Alignment with Your Needs

The most valuable free guidance directly addresses your current priorities. Consider whether the advice you're receiving:

- Speaks to your specific life stage and goals

- Acknowledges your unique circumstances

- Provides actionable next steps

- Helps you understand complex concepts relevant to your situation

Generic advice applicable to anyone may have limited value compared to insights tailored to your particular financial landscape.

Common Areas Covered in Free Financial Consultations

Understanding what topics typically receive coverage during complimentary advisory sessions helps you prepare productive questions and maximize the value of these interactions.

Retirement Planning Fundamentals

Most initial consultations touch on retirement readiness, including:

- Current savings rate assessment

- Projected retirement income needs

- Social Security claiming strategies

- Required Minimum Distribution (RMD) planning for those approaching age 73

- Healthcare cost considerations in retirement

These discussions help you understand whether your current trajectory aligns with your retirement goals. Retirement planning and estate planning often intersect, particularly for individuals with significant assets or complex family situations.

Investment Portfolio Review

If you have existing investments, advisors may offer preliminary observations about:

- Overall asset allocation appropriateness

- Fee structures and expense ratios

- Diversification across asset classes

- Tax efficiency of account types

- Alignment between investments and risk tolerance

These reviews typically identify broad opportunities rather than providing specific buy or sell recommendations, which require deeper analysis and a formal advisory relationship.

Tax Strategy Considerations

While advisors cannot provide tax advice unless they're also licensed tax professionals, they can discuss how financial decisions impact your tax situation. Common topics include:

- Tax-advantaged retirement account utilization

- Roth conversion opportunities

- Tax-loss harvesting concepts

- Charitable giving strategies

- Required Minimum Distribution timing

For comprehensive tax planning, working with a financial advisor and CPA provides coordinated guidance across both disciplines.

The Transition from Free Advice to Paid Services

Understanding when free resources have reached their limits and when ongoing professional guidance might benefit your situation represents an important financial decision itself.

Recognizing Complexity Thresholds

Certain financial situations benefit significantly from comprehensive professional management:

- Multiple income streams requiring coordination

- Business ownership with complex retirement plan options

- Significant inherited assets or windfalls

- Estate planning involving trusts or charitable vehicles

- Multi-generational wealth transfer goals

Making financial decisions becomes increasingly complex as your financial life evolves. The value of professional guidance often becomes apparent when free resources cannot adequately address your situation's nuances.

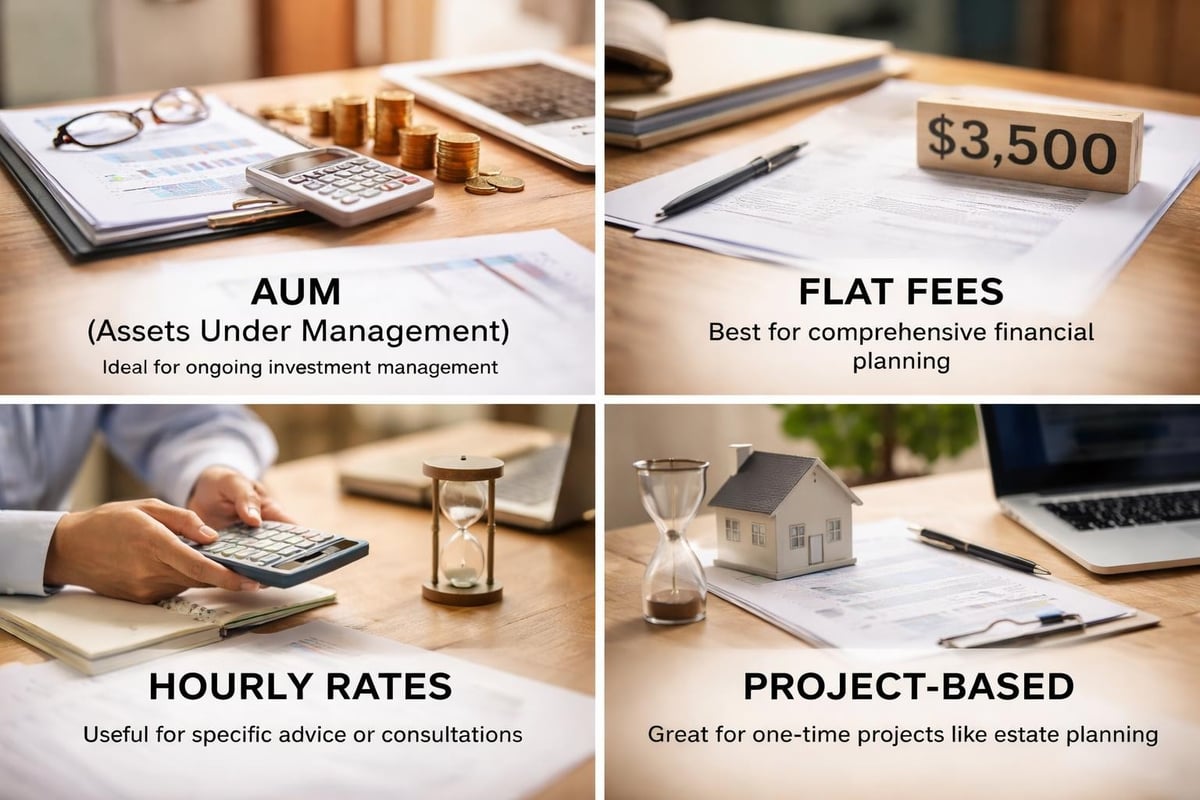

Understanding Fee Structures

When considering the transition to paid advisory services, understanding how advisors charge for their work enables informed comparisons:

| Fee Structure | How It Works | Potential Advantages |

|---|---|---|

| Assets Under Management (AUM) | Percentage of invested assets annually | Aligns advisor incentives with portfolio growth |

| Flat Fee | Annual or monthly retainer | Predictable costs regardless of portfolio size |

| Hourly Rate | Pay for specific consultations | Flexibility for specific questions or projects |

| Project-Based | One-time fee for defined scope | Clear costs for financial plan creation |

Fiduciary advisors transparently disclose their compensation structures and any potential conflicts of interest. This transparency allows you to evaluate the cost-benefit relationship of ongoing services.

Value Beyond Investment Returns

Professional financial guidance extends far beyond portfolio management. The value includes:

- Behavioral coaching during market volatility

- Coordination across multiple financial domains

- Tax-efficient withdrawal strategies in retirement

- Estate planning implementation and updates

- Regular progress monitoring toward goals

These services contribute to financial outcomes in ways that may not be immediately apparent in investment performance alone. Fiduciary financial advice ensures that all recommendations prioritize your interests above the advisor's compensation.

Maximizing Free Resources While Building Financial Knowledge

Strategic use of available free resources builds your financial literacy and helps you ask better questions when you do engage professional advisors.

Creating a Personal Financial Education Plan

Approach financial education systematically by:

- Identifying Knowledge Gaps: Assess which financial topics you understand well and which areas need development

- Prioritizing Learning Areas: Focus first on decisions you face soon, such as retirement account contributions or insurance needs

- Utilizing Multiple Sources: Free financial advice sources offer different perspectives and explanations

- Applying Knowledge Incrementally: Implement what you learn in manageable steps rather than attempting wholesale financial overhauls

This structured approach builds competence and confidence in managing your financial life.

Preparing for Advisory Consultations

Whether meeting with an advisor for a free consultation or engaging paid services, preparation enhances the value you receive. Gather:

- Recent account statements for all investments and retirement accounts

- Current budget or spending estimates

- List of financial goals with approximate timelines

- Questions about specific concerns or opportunities

- Information about employee benefits and existing insurance

This preparation enables more substantive conversations during limited consultation time. Financial consulting companies appreciate clients who arrive prepared, as it allows for more productive discussions.

Building Long-Term Financial Partnerships

Even if you begin with free resources and consultations, consider the relationship-building aspect of these interactions. The advisor you meet for a complimentary session today might become your trusted partner years later when your needs evolve.

Approach these relationships professionally by:

- Following through on action items discussed

- Providing feedback about what was helpful

- Staying in touch even if you're not ready for ongoing services

- Referring others who might benefit from the advisor's expertise

Quality advisors remember individuals who engage thoughtfully, even if they don't immediately become clients.

Avoiding Common Pitfalls with Free Financial Guidance

While financial advisor free advice provides genuine value, certain pitfalls can diminish its effectiveness or lead to poor decisions.

The "Free Lunch" Seminar Caution

Free financial seminars, particularly those targeting retirees, deserve careful scrutiny. While some offer legitimate education, others serve primarily as marketing vehicles for products with high commissions.

Warning signs include:

- High-pressure sales tactics following the presentation

- Focus on specific products rather than broad education

- Promises of guaranteed returns or risk-free investments

- Limited time offers requiring immediate decisions

Legitimate educational events provide value without requiring immediate commitments or purchases. They focus on building knowledge rather than generating sales.

Distinguishing Education from Recommendations

General financial education differs fundamentally from personalized recommendations. An article explaining Roth conversion benefits provides education. A specific recommendation about whether you should convert $50,000 from your Traditional IRA to a Roth IRA requires analysis of your individual tax situation, income projections, and retirement goals.

Attempting to apply general guidance to your specific situation without professional analysis can lead to suboptimal or even detrimental decisions. Recognize when you're receiving education versus when you need personalized advice.

The Limitations of Robo-Advisors

Automated investment platforms offer low-cost portfolio management and are sometimes positioned as sources of free or low-cost advice. These services provide value but have inherent limitations:

- Algorithm-based decisions lack nuanced judgment

- Limited consideration of factors outside the platform

- No coordination with broader financial planning needs

- Difficulty adapting to unique circumstances

Robo-advisors work well for straightforward investment management but cannot replace comprehensive financial planning for complex situations.

The Role of Virtual Advisory Services

The financial advisory landscape has evolved significantly, with virtual-first practices now offering the same comprehensive services traditionally delivered in person.

Accessibility Advantages

Virtual advisory relationships eliminate geographic constraints, allowing you to work with advisors whose expertise and approach align with your needs regardless of location. This model particularly benefits:

- Individuals in rural areas with limited local advisor options

- People with mobility challenges or demanding schedules

- Those who prefer digital communication

- Families with members in different locations

Technology enables secure document sharing, video conferencing, and collaborative financial planning tools that match or exceed in-person experiences.

Maintaining Personal Connection

Quality virtual advisory relationships prioritize personal connection despite physical distance. Advisors achieve this through:

- Regular video conferences rather than phone-only communication

- Proactive outreach during market volatility or life changes

- Personalized communication reflecting your specific goals and concerns

- Responsive service addressing questions and needs promptly

The virtual delivery method should enhance rather than diminish the personal nature of the advisory relationship. Working with independent financial advisors often provides flexibility in communication methods and meeting schedules.

Building Confidence in Financial Decision-Making

The ultimate goal of financial advisor free advice extends beyond answering immediate questions. It should build your confidence and capability in managing your financial life.

Developing Financial Literacy Over Time

Financial knowledge accumulates through:

- Consistent engagement with educational resources

- Practical application of learned concepts

- Learning from both successes and mistakes

- Asking questions when concepts remain unclear

This ongoing development transforms you from a passive recipient of advice to an informed participant in financial planning conversations. Even when working with professional advisors, your understanding enhances decision quality.

Knowing When to Seek Help

Part of financial wisdom involves recognizing when professional guidance provides value. Situations warranting advisor consultation include:

- Major life transitions such as retirement, inheritance, or divorce

- Significant financial windfalls requiring allocation decisions

- Complex tax situations involving multiple income sources

- Estate planning beyond basic wills

- Coordinating employee benefits with personal financial strategies

Seeking help appropriately demonstrates sound judgment rather than financial incompetence.

Creating Your Financial Action Plan

Whether you ultimately engage ongoing advisory services or manage your finances independently, a written financial plan provides direction and accountability. Your plan should address:

- Cash Flow Management: Income, expenses, and savings targets

- Debt Strategy: Prioritization and payoff timelines

- Emergency Reserves: Target amounts and account locations

- Retirement Savings: Contribution rates and account types

- Investment Approach: Asset allocation aligned with goals and risk tolerance

- Protection Needs: Insurance coverage for various risks

- Estate Considerations: Document status and beneficiary designations

Free consultations and resources can help you develop this framework, even if you implement it independently. Financial strategy planning provides structure to your financial life and clarity about progress toward goals.

Financial advisor free advice serves as a valuable entry point for individuals seeking to improve their financial situations without immediate cost commitments. Whether through complimentary consultations, employer programs, government resources, or educational content, these opportunities help you build knowledge and identify areas requiring attention. As your financial life grows more complex or you seek coordinated guidance across multiple domains, Brookwood Investment Group LLC offers fiduciary, virtual-first advisory services tailored to your unique goals and circumstances. Schedule a complimentary consultation to explore how personalized financial guidance can support your long-term objectives while maintaining the flexibility and accessibility that fits your lifestyle.