Understanding how financial professionals structure their compensation is essential for anyone seeking guidance with retirement planning, investment management, or comprehensive wealth strategies. The financial advisory landscape has evolved significantly, offering various payment models designed to align with different client needs and preferences. Navigating these options requires clarity about what you're paying for and how different structures might influence the advice you receive.

Types of Financial Advisor Charges

Financial advisor charges vary widely based on service models, client needs, and the complexity of financial situations. Understanding the primary compensation structures helps you evaluate which approach aligns with your goals and budget.

Assets Under Management (AUM) Fees

The most common structure involves percentage-based charges on assets under management, typically ranging from 0.50% to 2.00% annually. Under this model, clients pay based on the total value of investments the advisor manages.

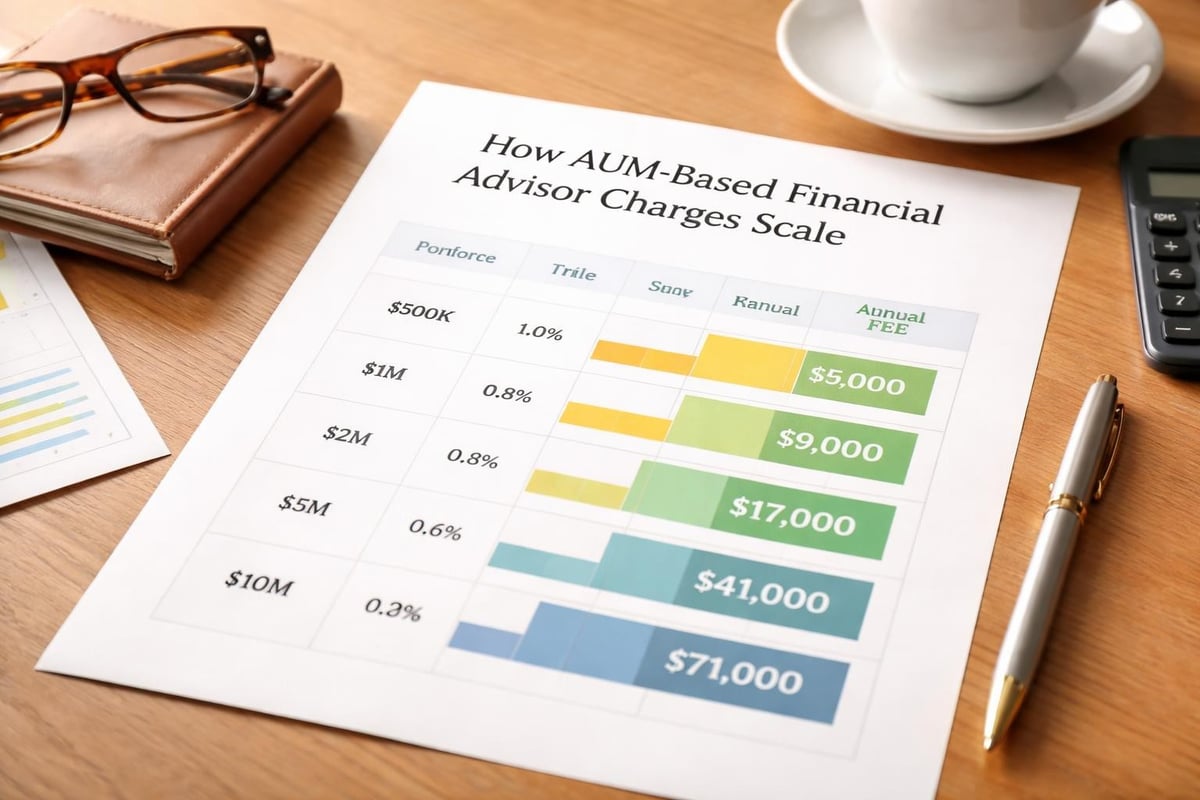

Common AUM fee tiers include:

- $500,000 or less: 1.00% to 1.50%

- $500,001 to $1 million: 0.75% to 1.25%

- $1 million to $5 million: 0.50% to 1.00%

- Above $5 million: 0.25% to 0.75%

This approach creates alignment between advisor and client interests, as both benefit from portfolio growth. However, the actual dollar amount you pay increases as your assets grow, even if the service level remains consistent.

Flat Fee and Retainer Models

Flat fee arrangements have gained popularity for their transparency and predictability. These structures offer clear value propositions independent of portfolio size, making them attractive for clients with complex needs but limited investable assets.

Annual retainer fees typically range from $2,000 to $10,000 or more, depending on service scope. This model works well for comprehensive financial planning that extends beyond investment management to include tax strategies, estate planning, and retirement projections.

Some advisors charge project-based flat fees for specific deliverables:

- Comprehensive financial plan: $1,500 to $5,000

- Retirement analysis: $1,000 to $3,000

- Estate planning coordination: $2,000 to $4,000

Hourly Consultation Rates

Hourly billing provides flexibility for clients seeking targeted advice rather than ongoing relationships. Financial advisor charges on an hourly basis generally range from $150 to $500 per hour, with credentialed professionals commanding premium rates.

This approach suits specific situations such as:

- Second opinions on major financial decisions

- One-time retirement readiness assessments

- Strategic planning for business owners

- Education on self-directed investing

The key advantage lies in paying only for services consumed, though total costs can become unpredictable for complex situations requiring extensive consultation time.

Understanding Fee-Only vs. Commission-Based Compensation

The distinction between fee-only and commission-based compensation significantly impacts the advice you receive and the relationship dynamics with your advisor.

Fee-Only Advisory Models

Fee-only advisors receive compensation exclusively from client fees, eliminating potential conflicts inherent in commission-based relationships. Understanding what fee-only financial advice means helps clients appreciate the transparency this model provides.

These professionals often operate as fiduciaries, legally obligated to act in clients' best interests. Working with fiduciary advisory services creates alignment where recommendations stem from client needs rather than product compensation.

| Fee-Only Advantages | Fee-Only Considerations |

|---|---|

| No product sales conflicts | May have higher upfront costs |

| Fiduciary standard typically applies | Limited access to certain products |

| Transparent compensation | Services may not include implementation |

| Objective recommendations | Client must be proactive in execution |

Commission and Hybrid Approaches

Commission-based advisors earn compensation through product sales, receiving payments from insurance companies, mutual fund providers, or brokerage firms. While this can reduce upfront client costs, it creates potential incentive misalignment.

Hybrid models combine fees and commissions, offering flexibility but requiring careful scrutiny. Different fee structures advisors use reflect varying business models and client service philosophies.

Understanding these distinctions proves particularly valuable when evaluating financial consulting company offerings and determining which compensation approach aligns with your preferences.

Evaluating Value Beyond Price

Financial advisor charges represent only one dimension of the advisor-client relationship. The true value extends to expertise, accessibility, comprehensive planning, and personalized strategy development.

Service Scope and Deliverables

Higher fees don't automatically indicate better service, nor do lower charges guarantee poor advice. Evaluate what's included in the compensation structure:

Comprehensive services might include:

- Quarterly portfolio reviews and rebalancing

- Annual tax-loss harvesting strategies

- Ongoing retirement projections and adjustments

- Estate planning coordination with attorneys

- Tax strategy collaboration with CPAs

- Insurance needs analysis and implementation

- Cash flow management and budgeting assistance

When assessing fiduciary planning offerings, consider whether the advisor provides integrated services or focuses narrowly on investment management. Comprehensive planning often justifies higher financial advisor charges through holistic value delivery.

Technology and Accessibility

Modern advisory relationships increasingly leverage technology for efficiency and client convenience. Virtual-first firms reduce overhead costs while maintaining service quality, potentially offering more competitive pricing structures.

Consider accessibility factors when evaluating fees:

- Communication responsiveness and availability

- Portal access for real-time account monitoring

- Digital document sharing and signing capabilities

- Video conferencing for personal consultations

- Mobile app functionality for on-the-go access

These technological advantages enable advisors to serve clients effectively regardless of geographic location, expanding options beyond traditional pension financial advisor near me searches.

Hidden Costs and Total Expense Ratios

Advertised financial advisor charges don't always represent total costs. Understanding the complete fee picture requires examining underlying investment expenses and potential additional charges.

Investment Product Expenses

Portfolios constructed with actively managed mutual funds carry expense ratios ranging from 0.50% to 2.00% annually. These internal costs exist separate from advisory fees, creating a layered expense structure.

Investment vehicle expense comparison:

| Investment Type | Typical Annual Expense |

|---|---|

| Index Funds | 0.03% to 0.20% |

| Actively Managed Mutual Funds | 0.50% to 2.00% |

| Exchange-Traded Funds (ETFs) | 0.05% to 0.75% |

| Separately Managed Accounts | 0.10% to 0.50% |

An advisor charging 1.00% annually who uses high-cost mutual funds averaging 1.50% in expenses creates a total annual cost of 2.50%. Conversely, an advisor with 1.25% fees using low-cost index funds at 0.10% results in total costs of 1.35%.

Additional Administrative Fees

Some financial advisor charges include supplementary costs for specific services or account features:

- Custodian fees for account maintenance

- Transaction costs for trading activity

- Financial planning software subscriptions passed to clients

- Document preparation and delivery charges

- Wire transfer and check-writing fees

Request a comprehensive fee disclosure covering all potential charges, not just the primary compensation structure. Evaluating fee structures requires examining total cost of engagement.

Negotiating and Comparing Financial Advisor Charges

Financial advisor charges aren't always fixed. Many professionals offer flexibility based on account size, service scope, and client circumstances.

When Fee Negotiation Makes Sense

Advisors with AUM-based structures often negotiate rates for larger portfolios. A client with $2 million might secure a 0.75% rate instead of the standard 1.00%, resulting in $5,000 annual savings.

Negotiation opportunities commonly arise with:

- High-net-worth portfolios exceeding $1 million

- Simplified service needs requiring less advisor time

- Multiple family members engaging the same advisor

- Transition from commission-based to fee-only relationships

However, focusing exclusively on price minimization can backfire. The lowest-cost advisor may lack expertise in critical areas like estate planning or advanced tax strategies, ultimately costing more through missed opportunities.

Comparing Apples to Apples

Creating meaningful comparisons requires standardizing assumptions across different advisor proposals. Understanding typical costs helps establish reasonable expectations.

Create a comparison framework including:

- Total annual costs as a percentage and dollar amount

- Specific services included in base fee

- Additional services requiring extra charges

- Investment philosophy and typical portfolio expenses

- Advisor credentials and experience level

- Communication frequency and accessibility

- Minimum account size or retainer requirements

Request written proposals detailing all components. This documentation facilitates informed decision-making and prevents misunderstandings about service expectations.

Questions to Ask About Fees

Transparent conversations about compensation demonstrate an advisor's commitment to clear communication and client understanding. Never hesitate to request detailed explanations of financial advisor charges.

Essential Fee Disclosure Questions

Direct questions yield clarity about total engagement costs and potential conflicts. Important distinctions exist between various advisory designations and compensation models.

Ask these specific questions:

- How are you compensated for the services you provide?

- Do you receive any third-party payments for product recommendations?

- What is your typical all-in cost for a client with my profile?

- How do you charge for additional services beyond investment management?

- What investment products do you typically recommend and what are their expense ratios?

- Are there any circumstances where your fees might increase?

- How often do you review and potentially adjust your fee structure?

Understanding Value Proposition

Price alone doesn't determine value. An advisor charging higher fees who implements sophisticated tax strategies saving $15,000 annually delivers far more value than a lower-cost provider offering basic services.

Evaluate the comprehensive value proposition:

- Years of experience and professional credentials

- Specialization in your specific financial situation

- Track record with clients in similar circumstances

- Breadth of services beyond portfolio management

- Quality of client communication and education

- Proactive planning and opportunity identification

Working with independent financial advisors often provides flexibility in service customization and fee structures compared to advisors employed by large institutions with standardized offerings.

The Fiduciary Difference in Fee Structures

The fiduciary standard requires advisors to act in clients' best interests, influencing how they structure compensation and make recommendations. This legal obligation affects financial advisor charges and service delivery.

Fiduciary vs. Suitability Standards

Fiduciary advisors must prioritize client interests above their own, while suitability standards only require recommendations to be appropriate, not necessarily optimal. This distinction profoundly impacts advice quality and fee transparency.

Fiduciary obligations typically accompany fee-only structures, though not exclusively. Fiduciary investment approaches emphasize minimizing conflicts while maximizing client outcomes.

Fiduciary advantages include:

- Legal requirement to disclose all conflicts of interest

- Duty to recommend lowest-cost appropriate solutions

- Obligation to avoid self-dealing and hidden compensation

- Responsibility to provide ongoing monitoring and adjustments

Impact on Service Delivery

Fiduciary advisors structure services around comprehensive client needs rather than product sales opportunities. This approach often results in integrated planning addressing retirement planning and estate planning simultaneously.

The compensation model influences service scope. Fee-only fiduciaries typically offer broader planning encompassing tax efficiency, insurance analysis, and legacy considerations beyond basic investment management.

Choosing the Right Fee Structure for Your Situation

No single compensation model suits every client. Your financial situation, planning complexity, and personal preferences should guide the selection process.

Life Stage Considerations

Different life stages present varying advisory needs and appropriate fee structures:

Early career professionals may benefit from hourly consultations for student loan strategies and initial retirement planning without justifying ongoing AUM fees.

Mid-career accumulators with growing portfolios often find AUM-based structures align well with wealth-building goals and increasingly complex planning needs.

Pre-retirees and retirees frequently require comprehensive services addressing retirement readiness, income planning, and wealth transfer, making flat-fee retainers or AUM models appropriate.

Business owners need specialized expertise in exit planning, succession strategies, and tax optimization, often warranting project-based fees or higher retainer arrangements given complexity.

Portfolio Size and Complexity

Account size significantly influences which fee structures offer the best value. Typical financial advisor costs vary based on service model and client circumstances.

| Portfolio Size | Often Most Cost-Effective Structure |

|---|---|

| Under $100,000 | Hourly consultation or flat-fee planning |

| $100,000 to $500,000 | Flat annual retainer or AUM hybrid |

| $500,000 to $2 million | AUM-based with negotiated rate |

| Above $2 million | Tiered AUM or custom retainer arrangement |

These guidelines aren't absolute. A $50,000 portfolio with complex estate planning needs might justify a flat-fee arrangement, while a $3 million portfolio in simple index funds could work with lower-touch, lower-cost advisory services.

Technology's Impact on Financial Advisor Charges

Digital platforms and robo-advisors have disrupted traditional advisory pricing, creating new options at various price points. Understanding how technology influences financial advisor charges helps identify the right service level.

Robo-Advisor Alternatives

Automated investment platforms charge 0.25% to 0.50% annually for algorithm-driven portfolio management. These services suit investors comfortable with digital-only interaction and standardized investment approaches.

However, robo-advisors typically lack:

- Personalized tax planning integration

- Complex estate planning coordination

- Behavioral coaching during market volatility

- Customized strategies for unique situations

- Comprehensive retirement income planning

Hybrid Human-Digital Models

Many advisors now blend technology efficiency with personal expertise, offering competitive pricing through reduced overhead. Virtual-first firms provide comprehensive services while maintaining lower fee structures than traditional brick-and-mortar practices.

This approach delivers:

- Video conferencing for personal consultations

- Digital document management and e-signatures

- Real-time portfolio monitoring through client portals

- Automated reporting and performance tracking

- Efficient communication via secure messaging

These technological advantages enable advisors to serve more clients effectively while potentially offering more competitive financial advisor charges without sacrificing service quality or personalized attention.

Understanding the full spectrum of financial advisor charges empowers you to make informed decisions about professional guidance that aligns with your goals and budget. Transparent fee structures, fiduciary obligations, and comprehensive service delivery create the foundation for successful long-term advisory relationships. Brookwood Investment Group LLC offers fee-only, fiduciary services with transparent pricing tailored to your unique financial situation. Schedule a consultation to explore how personalized, virtual-first financial guidance can support your retirement planning, investment management, and estate planning goals.