Planning for their retirement represents one of the most significant financial undertakings couples or families will face together. Whether managing finances as spouses, supporting aging parents, or advising adult children, understanding the comprehensive nature of retirement preparation requires careful coordination and strategic planning. The complexity increases when multiple individuals depend on shared resources, making it essential to develop a holistic approach that addresses both individual and collective needs. This guide explores the critical components of retirement planning, offering actionable strategies and insights for those navigating this important financial transition.

Understanding Retirement Savings Benchmarks

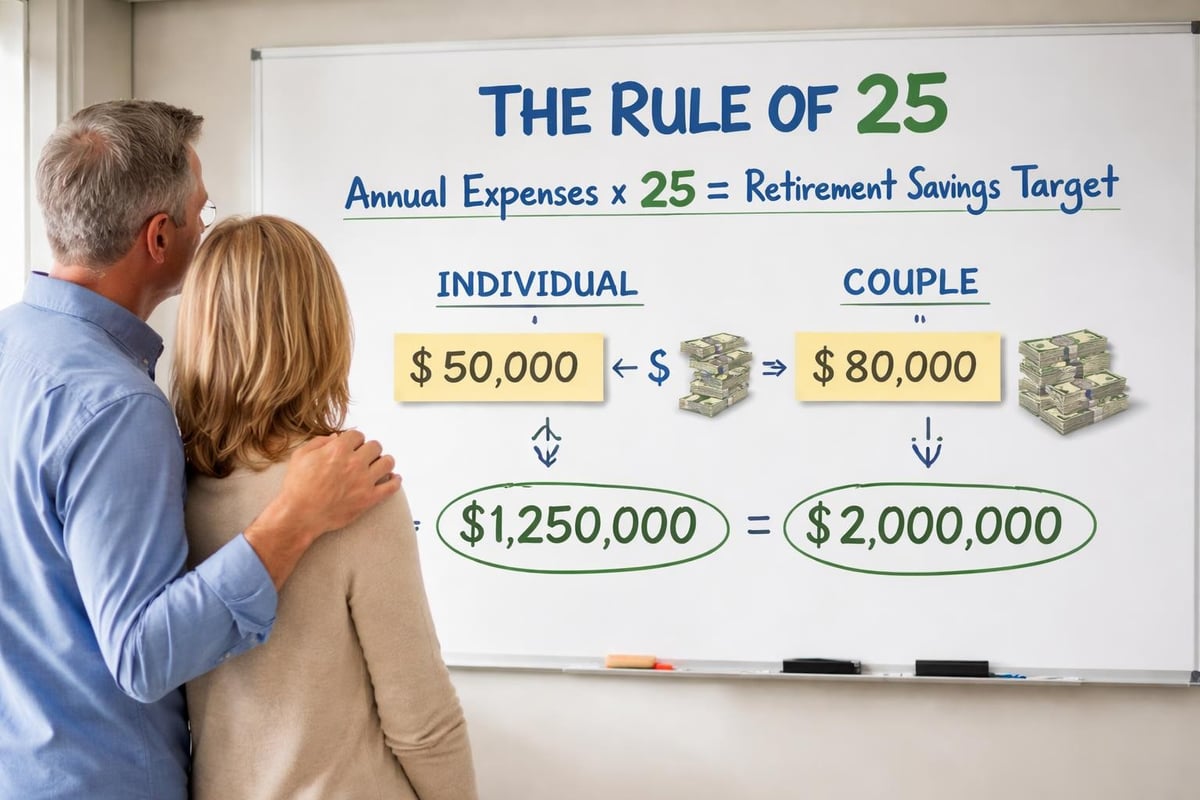

Establishing clear savings targets forms the foundation of successful retirement planning. Many financial professionals reference the Rule of 25 for retirement planning, which suggests individuals should aim to accumulate 25 times their anticipated annual retirement expenses. This benchmark provides a starting point for evaluating whether current savings trajectories align with future income needs.

Calculating Their Retirement Number

Determining the appropriate savings target requires analyzing several variables:

- Current household expenses: Track spending patterns to project future needs

- Anticipated lifestyle changes: Consider downsizing, travel plans, or relocating

- Healthcare projections: Factor in Medicare premiums, supplemental coverage, and out-of-pocket costs

- Inflation assumptions: Account for purchasing power erosion over multi-decade timelines

- Longevity expectations: Plan for potentially 30-plus years in retirement

The calculation becomes more nuanced when planning for multiple people. Couples often benefit from economies of scale in housing and basic living expenses, yet face higher healthcare costs and potentially longer combined life expectancies. A household requiring $80,000 annually would need approximately $2 million using the Rule of 25 framework, though individual circumstances may warrant adjustments.

Age-Specific Accumulation Strategies

The approach to building retirement savings evolves throughout different life stages. For those in their 50s approaching retirement, strategic moves to boost retirement savings become increasingly important. This decade offers unique opportunities through catch-up contributions and portfolio repositioning.

| Age Range | Primary Focus | Key Actions |

|---|---|---|

| 20s-30s | Foundation building | Establish consistent contribution habits, maximize employer matches |

| 40s | Acceleration | Increase contribution percentages, diversify investments |

| 50s-60s | Optimization | Utilize catch-up contributions, evaluate risk allocation |

| 60s+ | Transition | Implement distribution strategies, coordinate tax planning |

Those who have already maxed out their 401(k) contributions in 2026 should explore supplementary savings vehicles. Health Savings Accounts offer triple tax advantages for those with qualifying high-deductible health plans, while taxable brokerage accounts provide flexibility without contribution limits or withdrawal restrictions.

Developing Sustainable Income Strategies

Converting accumulated assets into reliable income streams represents a critical transition point in their retirement journey. The distribution phase requires careful planning to balance current needs with longevity risk, tax efficiency, and legacy objectives.

The Bucket Strategy Approach

One effective framework involves segmenting assets into multiple "buckets" based on time horizons:

Immediate needs bucket (0-2 years)

- Cash and money market funds

- High-quality short-term bonds

- Provides stability and accessibility

Intermediate bucket (3-10 years)

- Balanced portfolio of bonds and dividend-paying stocks

- Moderate growth potential with reduced volatility

- Replenishes the immediate bucket periodically

Long-term growth bucket (10+ years)

- Equity-focused investments

- Real estate or alternative assets

- Supports purchasing power maintenance

This segmentation approach, detailed in retirement income strategies for the long haul, helps manage sequence-of-returns risk while maintaining growth potential. Working with professionals who understand fiduciary planning ensures these strategies align with clients' best interests.

Tax-Efficient Withdrawal Sequencing

The order in which different account types are accessed significantly impacts after-tax income. Strategic withdrawal sequencing considers:

- Required minimum distributions (RMDs): Must begin at age 73 for traditional retirement accounts

- Tax bracket management: Filling lower brackets with taxable income strategically

- Roth conversion opportunities: Moving traditional IRA assets to Roth accounts during lower-income years

- Capital gains harvesting: Utilizing 0% or preferential capital gains rates when available

- Social Security timing: Coordinating benefit claims with overall tax planning

Couples have additional flexibility through coordinated claiming strategies and income splitting between spouses. These decisions interact with healthcare subsidy eligibility, Medicare premium calculations, and state tax considerations.

Managing Longevity and Spending Risks

One of the most common concerns involves the possibility of outliving available resources. Strategies to address the fear of depleting retirement funds focus on establishing sustainable spending baselines and building appropriate safety margins.

Calculating Safe Withdrawal Rates

Traditional guidance suggested 4% annual withdrawals adjusted for inflation, though current research indicates this may require modification based on:

- Prevailing interest rates and bond yields

- Stock market valuations at retirement initiation

- Individual portfolio allocation

- Flexibility to reduce spending during market downturns

- Additional income sources (pensions, annuities, part-time work)

For their retirement planning, couples might adopt a dynamic spending approach that adjusts based on portfolio performance. Strong market years allow for higher discretionary spending, while weaker periods trigger modest reductions in variable expenses like travel or entertainment.

Building Recession Buffers

Market downturns early in retirement pose particular risks through sequence-of-returns challenges. Protective strategies include:

- Maintaining 2-3 years of expenses in stable, liquid assets

- Establishing lines of credit before retirement (when qualification is easier)

- Preserving flexibility to reduce withdrawals temporarily

- Generating supplemental income through part-time consulting or hobbies

- Implementing annuity products for guaranteed income floors

The Department of Labor’s retirement planning tools offer interactive worksheets to help model various scenarios and stress-test financial plans against different economic environments.

Optimizing Spending and Lifestyle Choices

Thoughtful expense management during retirement extends available resources while potentially enhancing quality of life. Creative approaches to spending less and saving more demonstrate how strategic lifestyle decisions compound over decades.

Housing Considerations

Housing typically represents the largest retirement expense category. Options for their retirement planning include:

- Downsizing: Reducing square footage to lower utilities, maintenance, and property taxes

- Geographic arbitrage: Relocating to lower-cost-of-living areas

- Alternative arrangements: Exploring 55+ communities, co-housing, or multi-generational living

- Home equity strategies: Evaluating reverse mortgages or home equity lines of credit

Each option carries trade-offs involving proximity to family, healthcare access, climate preferences, and emotional attachment to long-time residences. These decisions often benefit from professional guidance available through comprehensive financial services.

Healthcare Cost Management

Medical expenses represent both a significant and unpredictable retirement cost. Effective management strategies include:

| Strategy | Description | Potential Savings |

|---|---|---|

| Medicare optimization | Comparing original Medicare plus supplements versus Medicare Advantage | $1,000-$3,000 annually |

| HSA maximization | Contributing maximum amounts in pre-retirement years | $4,000-$8,000 in tax savings |

| Prescription management | Using generic medications, mail-order pharmacies, patient assistance programs | $500-$2,000 annually |

| Preventive care | Maximizing covered preventive services, maintaining healthy lifestyle | Reduces long-term costs |

Long-term care planning deserves particular attention, as extended care needs can rapidly deplete assets. Options range from traditional long-term care insurance to hybrid life insurance policies with care riders, self-insurance through dedicated savings, or strategic asset positioning.

Coordinating Estate and Legacy Planning

Their retirement planning extends beyond personal needs to encompass legacy objectives and efficient wealth transfer. Proper estate planning ensures assets transfer according to wishes while minimizing tax burdens and administrative complications.

Essential Estate Documents

Complete estate planning requires several coordinated components:

- Wills: Specify asset distribution and guardianship arrangements

- Trusts: Provide probate avoidance, privacy, and control over distribution timing

- Beneficiary designations: Ensure retirement accounts and insurance policies align with overall plan

- Powers of attorney: Authorize financial and healthcare decisions if incapacitated

- Healthcare directives: Communicate end-of-life care preferences

These documents require periodic review, particularly following major life events like marriages, divorces, births, deaths, or significant wealth changes. Many couples benefit from working with advisors who coordinate between legal, tax, and financial professionals to ensure comprehensive planning.

Tax-Efficient Wealth Transfer

Strategic gifting and wealth transfer planning can significantly reduce estate tax exposure while providing support to heirs or charitable causes:

- Annual gift exclusions: Each person can gift $18,000 per recipient in 2026 without gift tax consequences

- Lifetime exemption: Current federal estate tax exemption exceeds $13 million per individual

- Qualified charitable distributions: Direct IRA distributions to charity (available at age 70½)

- Appreciated asset transfers: Gifting appreciated securities avoids capital gains recognition

- Education funding: Contributing to 529 plans or directly paying educational institutions

Coordination between these strategies and retirement income planning helps optimize lifetime and legacy outcomes. Understanding how trust advisors operate within this framework provides additional planning opportunities.

Investment Management Throughout Retirement

Portfolio management approaches evolve as individuals transition from accumulation to distribution phases. Their retirement investment strategy must balance growth needs with income requirements and risk tolerance changes.

Asset Allocation Adjustments

Traditional age-based allocation rules suggested holding bond percentages equal to one's age, though modern approaches consider multiple factors:

- Guaranteed income sources (Social Security, pensions) affecting risk capacity

- Spending flexibility and willingness to adjust lifestyle

- Legacy intentions and time horizons beyond personal lifespans

- Healthcare needs and potential long-term care costs

- Emotional comfort with market volatility

A comprehensive allocation might include:

- Domestic stocks: 30-50% for growth and inflation protection

- International stocks: 10-20% for diversification

- Bonds and fixed income: 25-40% for stability and income

- Real assets: 5-15% in real estate, commodities, or inflation-protected securities

- Cash reserves: 5-10% for near-term spending needs

Those working with independent financial advisors benefit from ongoing portfolio rebalancing and tax-loss harvesting strategies that enhance after-tax returns.

Dividend and Income Investing

Income-focused strategies can provide psychological comfort and reduce the need to sell appreciated assets during market downturns. Quality dividend-paying stocks and investment-grade bonds form the core of many retirement portfolios.

However, income investors should avoid common pitfalls:

- Overconcentration in specific sectors (utilities, telecoms, real estate)

- Chasing unsustainably high yields that signal financial distress

- Neglecting total return in favor of current income

- Ignoring tax efficiency between qualified dividends and ordinary income

Diversified approaches balance current income generation with capital appreciation potential and tax efficiency. This strategy aligns with effective retirement strategies that emphasize comprehensive planning over single-dimensional approaches.

Social Security Optimization

Claiming decisions regarding Social Security benefits significantly impact their retirement income security. Coordinated spousal claiming strategies can enhance lifetime benefits by hundreds of thousands of dollars.

Individual Claiming Considerations

Key factors influencing optimal claiming age include:

- Break-even analysis: Comparing cumulative benefits across different claiming ages

- Longevity expectations: Family health history and personal health status

- Spousal benefit coordination: Maximizing survivor benefits for the longer-lived spouse

- Earnings considerations: Impact of continued work on benefit calculations and taxation

- Other income sources: Ability to delay claiming while living on other assets

For each year benefits are delayed beyond full retirement age (67 for those born in 1960 or later), monthly payments increase by approximately 8% until age 70. This represents a guaranteed, inflation-adjusted return unavailable elsewhere.

Spousal Coordination Strategies

Married couples have additional optimization opportunities:

| Strategy | Description | Best For |

|---|---|---|

| Higher earner delays | Lower earner claims earlier, higher earner waits until 70 | Couples with significant earnings disparity |

| Both delay | Both spouses wait until 70 | Couples with other income sources and longevity expectations |

| Survivor benefit maximization | Higher earner delays to maximize survivor benefit | Age gaps or health disparities |

These decisions interact with Medicare enrollment requirements, tax planning, and overall retirement income strategies. Resources from Fidelity’s retirement guidance can help model different scenarios, though personalized advice considering individual circumstances often proves valuable.

Healthcare Planning and Medicare Decisions

Healthcare represents both a significant expense category and a complex decision landscape during their retirement years. Understanding Medicare options and supplemental coverage ensures adequate protection while managing costs.

Medicare Enrollment and Coverage Choices

Initial Medicare decisions occur around age 65, regardless of retirement timing:

- Part A (Hospital Insurance): Typically premium-free for those with sufficient work history

- Part B (Medical Insurance): Requires monthly premiums based on income

- Part D (Prescription Drug Coverage): Optional but recommended to avoid penalties

- Medigap Supplements: Fill coverage gaps in original Medicare

- Medicare Advantage: Alternative comprehensive plans offered by private insurers

Each option involves trade-offs between premiums, deductibles, provider networks, and out-of-pocket maximums. Those who worked with financial advisors for business owners during their careers may need to adjust to Medicare after years of employer-sponsored coverage.

Income-Related Premium Adjustments

Higher-income retirees pay additional Medicare Part B and Part D premiums based on modified adjusted gross income from two years prior. Strategic income management can potentially reduce these surcharges:

- Timing Roth conversions to avoid IRMAA brackets

- Harvesting capital losses to offset gains

- Coordinating qualified charitable distributions

- Managing retirement account withdrawals strategically

These adjustments apply at specific income thresholds, making awareness of bracket boundaries valuable for tax planning. Coordination with overall distribution strategies discussed through comprehensive retirement planning ensures optimal outcomes.

Addressing Emotional and Psychological Dimensions

Financial planning represents only one component of successful retirement transitions. Their retirement journey involves identity shifts, relationship adjustments, and purpose redefinition that require thoughtful navigation.

Transitioning from Accumulation to Distribution

Many individuals find spending accumulated assets psychologically challenging after decades of saving discipline. Common concerns include:

- Guilt about using money saved through sacrifice and delayed gratification

- Anxiety about market volatility affecting lifestyle sustainability

- Uncertainty about appropriate spending levels

- Fear of becoming a burden on family members

These emotional dimensions benefit from structured planning frameworks that provide spending permissions within defined guardrails. Dynamic spending rules, periodic plan reviews, and scenario modeling can build confidence in financial sustainability.

Relationship and Communication Considerations

Retirement often brings couples into closer daily contact after years of separate work routines. Successful transitions involve:

- Discussing retirement visions and expectations openly

- Establishing individual space and activities alongside shared pursuits

- Addressing different risk tolerances or spending philosophies

- Creating systems for financial decision-making and accountability

- Maintaining social connections beyond the marriage relationship

These conversations often prove easier with neutral third-party facilitation. Working with advisors who understand both technical and interpersonal dimensions of their retirement planning can smooth these transitions.

Risk Management and Insurance Strategies

Comprehensive retirement planning addresses various risk exposures that could derail financial security. Their retirement protection strategy should encompass multiple insurance types and risk mitigation approaches.

Insurance Coverage Evaluation

Key insurance considerations during retirement include:

- Health insurance: Medicare plus supplements or Medicare Advantage

- Long-term care: Traditional policies, hybrid products, or self-insurance strategies

- Life insurance: Evaluating continued need as assets accumulate and dependents age

- Liability protection: Umbrella policies protecting accumulated wealth

- Property and casualty: Homeowners, auto, and specialty coverage for valuables

Coverage needs evolve throughout retirement as circumstances change. Periodic reviews ensure protection remains appropriate while avoiding unnecessary premium expenditures on outdated policies.

Longevity Insurance and Annuities

Deferred income annuities and qualified longevity annuity contracts (QLACs) address tail-end longevity risk by providing guaranteed income beginning at advanced ages like 80 or 85. These products offer:

- Protection against outliving assets

- Reduced required minimum distributions (forQLACs)

- Cost efficiency compared to immediate annuities

- Peace of mind regarding basic expense coverage

However, annuity products involve trade-offs including reduced liquidity, inflation exposure, and opportunity costs. Evaluation should consider these products as one component within diversified retirement income strategies rather than singular solutions.

Planning for their retirement requires comprehensive coordination across savings, investments, income strategies, tax planning, healthcare, and estate considerations. The complexity increases when addressing multiple individuals' needs, making professional guidance particularly valuable for navigating these interconnected decisions. Brookwood Investment Group offers personalized, fiduciary financial guidance tailored to your unique retirement goals, helping you transition confidently from accumulation to distribution while addressing the full spectrum of retirement planning considerations.