Understanding the rules surrounding a rollover IRA withdrawal can significantly impact your retirement planning strategy and overall financial health. When you consolidate funds from a previous employer's 401(k) or other qualified retirement plan into a rollover IRA, you gain flexibility and control over your investments. However, accessing those funds before retirement age involves navigating complex tax regulations and potential penalties. Making informed decisions about when and how to withdraw from your rollover IRA requires careful consideration of your current financial situation, future goals, and the specific regulations that govern these accounts.

Understanding Rollover IRA Basics

A rollover IRA serves as a holding account for retirement funds transferred from employer-sponsored plans. This vehicle allows individuals who change jobs or retire to maintain the tax-advantaged status of their retirement savings while consolidating multiple accounts into a single, manageable portfolio.

The primary advantage of a rollover IRA lies in its expanded investment options compared to typical employer plans. You can choose from a broader range of mutual funds, stocks, bonds, and other securities to align with your specific financial objectives and risk tolerance.

Direct vs. Indirect Rollovers

Two methods exist for moving funds into a rollover IRA, each with distinct implications:

- Direct rollover: The plan administrator transfers funds directly to your IRA custodian

- Indirect rollover: You receive a check and have 60 days to deposit it into your IRA

- Tax withholding: Indirect rollovers typically involve 20% mandatory withholding

Direct rollovers eliminate the risk of missing deadlines and facing unnecessary tax consequences. The rollover process requires careful attention to IRS guidelines to avoid triggering taxable events or penalties.

When considering retirement account management strategies, working with professionals who understand the nuances of retirement planning and estate planning can help you navigate these complex decisions.

Age-Based Withdrawal Rules

The age at which you access rollover IRA funds determines whether you face penalties and how much tax you'll owe. Understanding these age thresholds helps you plan withdrawals strategically.

Before Age 59½

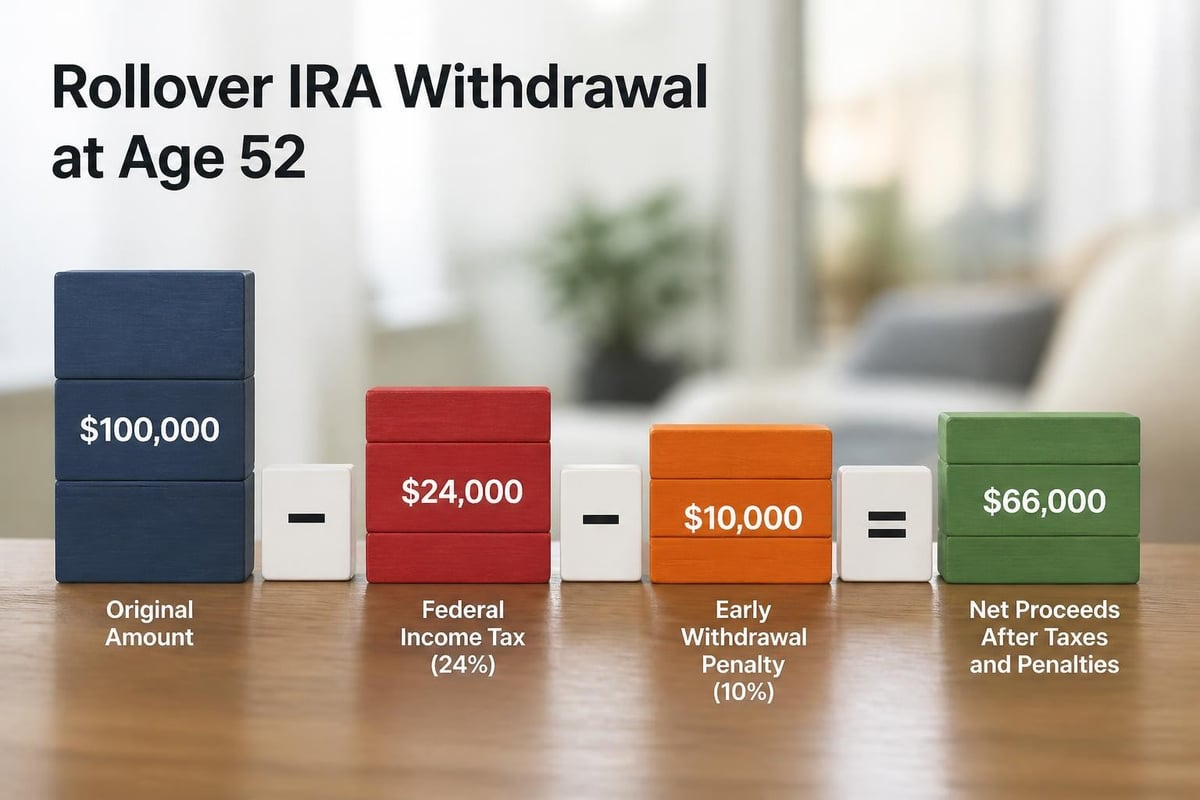

Making a rollover IRA withdrawal before reaching age 59½ typically triggers a 10% early withdrawal penalty on top of ordinary income taxes. This dual tax burden can significantly erode your retirement savings.

Consider this example: A $20,000 withdrawal at age 52 with a 24% tax bracket results in:

| Component | Amount |

|---|---|

| Withdrawal Amount | $20,000 |

| Income Tax (24%) | $4,800 |

| Early Withdrawal Penalty (10%) | $2,000 |

| Total Tax Burden | $6,800 |

| Net Proceeds | $13,200 |

Ages 59½ to 72

Once you reach 59½, you can make penalty-free withdrawals from your rollover IRA. However, you still owe ordinary income taxes on distributions from traditional IRAs. This flexibility allows you to access funds as needed without the additional 10% penalty.

Strategic withdrawal planning during this period can help manage your tax liability effectively. Understanding key milestone ages in retirement enables better planning for your financial future.

After Age 72

Required Minimum Distributions (RMDs) become mandatory at age 72 for traditional rollover IRAs. The IRS calculates your RMD based on your account balance and life expectancy, forcing you to withdraw and pay taxes on a minimum amount annually.

Failing to take your RMD results in a steep 50% penalty on the amount you should have withdrawn. This substantial consequence makes compliance essential for anyone with traditional retirement accounts.

Penalty-Free Withdrawal Exceptions

The IRS recognizes specific circumstances where early rollover IRA withdrawal penalties don't apply, even if you're under 59½. These exceptions provide financial flexibility during life's challenging moments.

Qualified Education Expenses

You can withdraw funds penalty-free to pay for qualified higher education expenses for yourself, your spouse, children, or grandchildren. Eligible expenses include:

- Tuition and fees

- Books and required supplies

- Room and board (for students enrolled at least half-time)

- Equipment required for enrollment

First-Time Home Purchase

The IRS allows penalty-free withdrawals of up to $10,000 for qualified first-time home buyers. This lifetime limit applies to purchases for yourself, your spouse, children, grandchildren, or parents.

Medical Expenses and Insurance

Unreimbursed medical expenses exceeding 7.5% of your adjusted gross income qualify for penalty-free withdrawals. Additionally, if you're unemployed, you can use rollover IRA funds to pay health insurance premiums without penalty.

Substantially Equal Periodic Payments

Section 72(t) allows you to take substantially equal periodic payments (SEPP) based on your life expectancy without penalty. However, you must continue these payments for at least five years or until you reach 59½, whichever is longer.

The specific rules and exceptions to early withdrawal penalties require careful analysis to ensure compliance and avoid unexpected tax consequences.

Tax Implications of Rollover IRA Withdrawals

Understanding the tax treatment of your rollover IRA withdrawal is crucial for accurate financial planning and avoiding surprises during tax season.

Traditional Rollover IRA Taxation

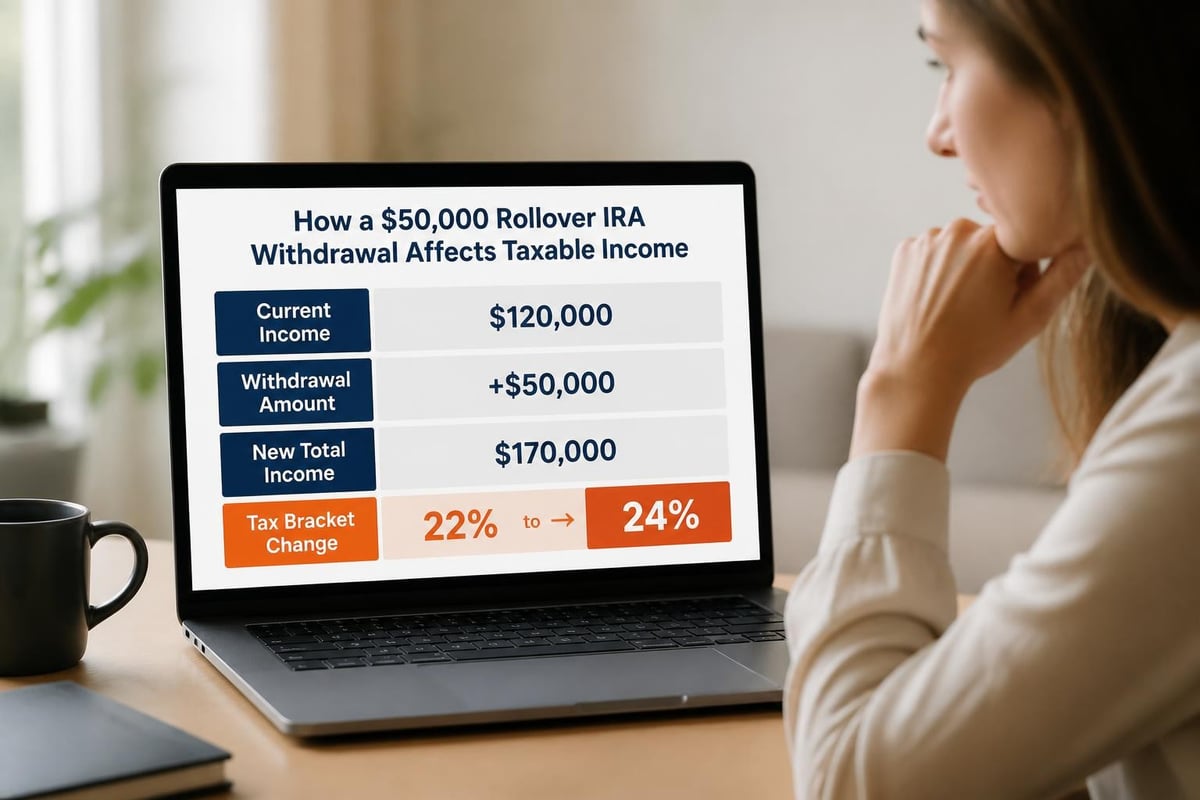

Withdrawals from traditional rollover IRAs are taxed as ordinary income at your current tax rate. Since contributions to the original 401(k) or traditional IRA were made with pre-tax dollars, the IRS taxes the entire distribution amount.

Your withdrawal amount adds to your gross income for the year, potentially pushing you into a higher tax bracket. This bracket creep can result in paying more taxes on both the withdrawal and your other income sources.

Roth Conversion Considerations

Converting a traditional rollover IRA to a Roth IRA creates a taxable event in the conversion year. However, qualified distributions from Roth IRAs after age 59½ are tax-free, provided the account has been open for at least five years.

Considerations before rolling your 401(k) into a Roth IRA include current versus future tax rates, time horizon until retirement, and your ability to pay conversion taxes from non-retirement assets.

State Tax Considerations

While federal tax rules apply uniformly, state tax treatment of retirement account withdrawals varies significantly. Some states don't tax retirement income at all, while others offer partial exemptions based on age or income level.

If you're considering relocation during retirement, state tax policies on IRA withdrawals should factor into your decision. Consulting with fiduciary planning professionals can help you understand these geographic tax differences.

Strategic Withdrawal Planning

Developing a thoughtful approach to rollover IRA withdrawal timing and amounts can minimize taxes and preserve wealth for future needs.

Assessing Your Cash Flow Needs

Before initiating any withdrawal, evaluate your comprehensive financial situation:

- Review current expenses and income sources

- Identify short-term cash requirements versus long-term goals

- Explore alternative funding sources that might be more tax-efficient

- Calculate the true cost of withdrawal including taxes and penalties

Tax-Loss Harvesting Coordination

If you maintain taxable investment accounts alongside your rollover IRA, coordinate withdrawals with tax-loss harvesting strategies. Offsetting capital gains with losses in taxable accounts while taking IRA distributions can optimize your overall tax picture.

Multi-Year Tax Planning

Consider spreading large withdrawals across multiple tax years to avoid bracket creep. This approach works particularly well during early retirement years before RMDs begin and Social Security benefits start.

| Strategy | Tax Efficiency | Complexity | Best For |

|---|---|---|---|

| Single large withdrawal | Low | Simple | Immediate major expense |

| Multi-year distribution | High | Moderate | Flexible timeline |

| Roth conversion ladder | Very High | Complex | Long-term planning |

| 72(t) SEPP | Moderate | Complex | Early retirees under 59½ |

Understanding traditional IRA contribution and distribution rules helps you develop strategies that align with your specific circumstances.

Required Minimum Distributions

RMDs represent mandatory withdrawals that begin at age 72, fundamentally changing how you access and manage your rollover IRA funds.

Calculating Your RMD

The IRS provides life expectancy tables to calculate your annual RMD. You divide your December 31 account balance from the previous year by the distribution period corresponding to your age.

For example, at age 72 with a $500,000 account balance, using the IRS Uniform Lifetime Table with a distribution period of 27.4:

$500,000 ÷ 27.4 = $18,248 (approximate RMD)

RMD Timing Strategies

While your first RMD can be delayed until April 1 of the year following the year you turn 72, this delay means taking two distributions in one tax year. This concentration of income might push you into a higher tax bracket.

Most financial professionals recommend taking your first RMD in the year you turn 72 to spread the tax burden more evenly. Detailed guidance on IRA withdrawals and required distributions can help you understand your specific obligations.

Qualified Charitable Distributions

If you're charitably inclined, Qualified Charitable Distributions (QCDs) allow you to satisfy your RMD while excluding the distribution from taxable income. You can donate up to $100,000 annually directly from your IRA to qualified charities.

This strategy provides several advantages:

- Satisfies RMD requirements

- Reduces adjusted gross income

- May help avoid Medicare premium increases

- Allows tax benefits even if you don't itemize deductions

Common Rollover IRA Withdrawal Mistakes

Avoiding these frequent errors can save thousands in unnecessary taxes and penalties while preserving your retirement security.

Missing the 60-Day Deadline

For indirect rollovers, depositing funds into your new IRA within 60 days is critical. Missing this deadline converts the distribution into a taxable withdrawal subject to income taxes and potential penalties.

The IRS rarely grants extensions unless extraordinary circumstances prevented timely completion. Natural disasters, serious illness, or postal errors might qualify, but you must apply for a waiver and provide supporting documentation.

Ignoring State-Specific Rules

Some states impose additional penalties or have different age thresholds for penalty-free withdrawals. Research your state's specific regulations or work with advisors familiar with local tax codes.

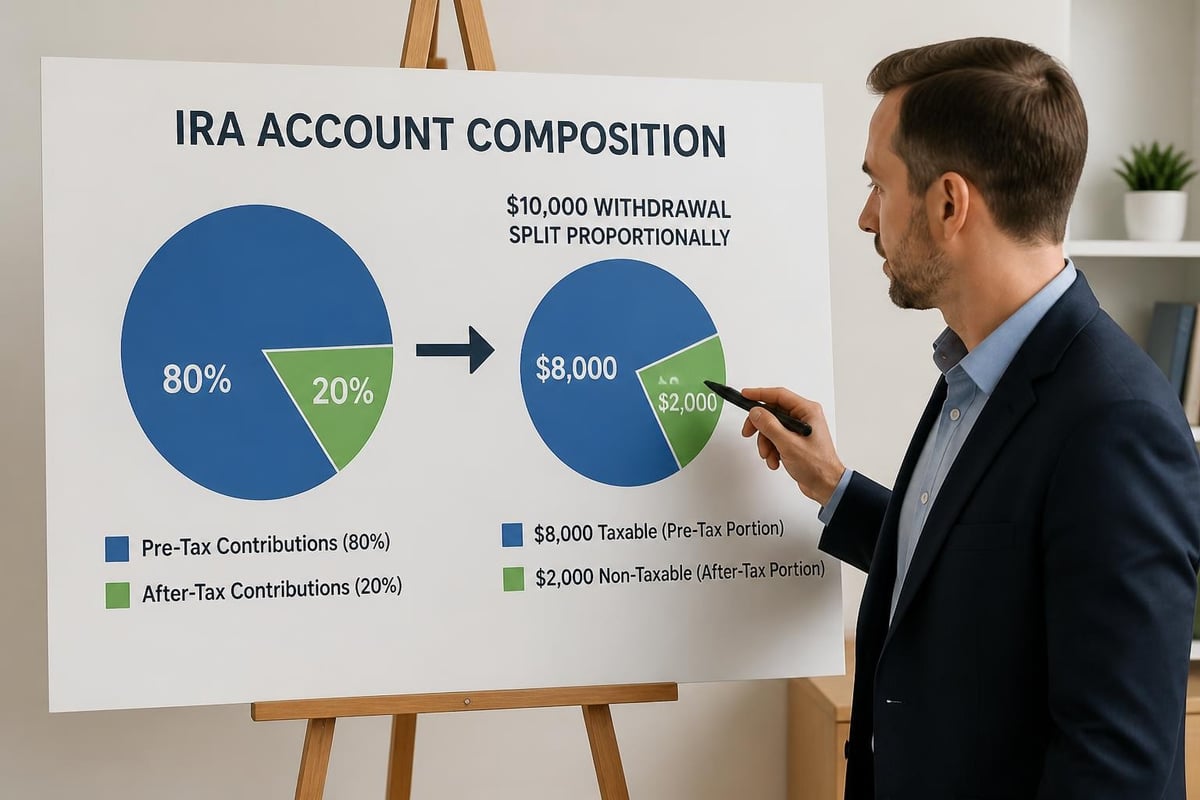

Overlooking Pro-Rata Rules

If you have both pre-tax and after-tax dollars in your IRA (such as from non-deductible contributions), the IRS applies pro-rata rules. You can't selectively withdraw only after-tax contributions to avoid taxes-each distribution includes a proportional mix of taxable and non-taxable funds.

Taking Unnecessary Early Withdrawals

Before making a rollover IRA withdrawal, explore alternatives like:

- Emergency fund savings

- Home equity lines of credit

- Personal loans

- Taxable investment account withdrawals

- Part-time work or gig economy opportunities

Each alternative has trade-offs, but preserving tax-advantaged retirement accounts should be prioritized when possible. Your financial services team can help evaluate which funding sources make the most sense for your situation.

Documentation and Reporting Requirements

Proper documentation of your rollover IRA withdrawal ensures compliance and simplifies tax filing.

Form 1099-R

Your IRA custodian issues Form 1099-R annually, reporting all distributions from your account. This form includes:

- Total distribution amount

- Taxable amount

- Distribution code indicating the type of withdrawal

- Federal and state tax withholding amounts

IRS Form 5329

If you qualify for an early withdrawal exception, you may need to file Form 5329 with your tax return to claim the exemption. This form calculates any additional taxes on early distributions and documents your qualification for penalty relief.

Maintaining Personal Records

Keep detailed records of:

- Rollover contribution statements

- Distribution requests and confirmations

- Tax returns showing IRA contributions and withdrawals

- Documentation supporting penalty exceptions (education receipts, home purchase contracts, medical bills)

These records become invaluable if the IRS questions your withdrawal reporting or if you need to reconstruct your cost basis years later.

Coordinating Withdrawals with Other Retirement Income

A rollover IRA withdrawal rarely occurs in isolation. Coordinating distributions with other income sources optimizes your tax situation and ensures sustainable cash flow throughout retirement.

Social Security Timing

When you claim Social Security benefits affects your overall tax picture. Up to 85% of Social Security benefits become taxable based on your combined income, which includes IRA withdrawals.

Strategically timing IRA distributions relative to Social Security claiming can minimize taxes on your benefits while meeting spending needs.

Pension Income Coordination

If you receive pension income, it's taxed as ordinary income like IRA distributions. Balancing withdrawals from multiple sources helps manage your marginal tax rate effectively.

Medicare Premium Considerations

Your modified adjusted gross income (MAGI) from two years prior determines Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amounts (IRMAA). Large IRA withdrawals can push you into higher premium brackets, effectively increasing the cost of your distribution.

Understanding these interconnected financial decisions helps you approach retirement income planning holistically rather than viewing each account in isolation.

Working with Financial Professionals

The complexity of rollover IRA withdrawal rules, tax implications, and strategic planning often warrants professional guidance.

Fiduciary Advisors

Working with a fiduciary advisor ensures recommendations prioritize your best interests. Fiduciaries must disclose conflicts of interest and provide advice aligned with your financial goals rather than commission-based product sales.

Tax Professionals

CPAs and enrolled agents specializing in retirement taxation can model various withdrawal scenarios, showing the tax impact of different strategies. Their expertise proves particularly valuable when coordinating complex situations like Roth conversions, business ownership, or multi-state tax obligations.

Comprehensive Planning Approach

The most effective retirement planning integrates investment management, tax strategy, estate planning, and risk management. This holistic view ensures withdrawal decisions support your broader financial objectives rather than creating unintended consequences elsewhere in your plan.

Professionals experienced in customized planning can adapt strategies to your unique circumstances, family situation, health considerations, and legacy goals.

Technology and Tools for Withdrawal Planning

Modern technology provides powerful resources for modeling rollover IRA withdrawal scenarios and tracking distributions.

Online Calculators

Numerous online tools calculate:

- RMD amounts based on current account balances

- Tax impact of various withdrawal amounts

- Penalty-free exception eligibility

- Long-term account projections with different distribution rates

Portfolio Management Software

Comprehensive platforms integrate all your financial accounts, providing a unified view of assets, liabilities, income, and expenses. These systems can model withdrawal strategies across multiple accounts simultaneously.

Tax Planning Software

Advanced tax software projects future tax liability based on different income scenarios. By inputting potential IRA withdrawals, you can see exactly how distributions affect your overall tax situation before committing to a strategy.

While technology provides valuable insights, it complements rather than replaces professional advice. The nuances of your specific situation often require expert interpretation that algorithms can't fully capture.

Impact of Life Changes on Withdrawal Strategy

Major life events often necessitate reassessing your rollover IRA withdrawal approach.

Divorce

Divorce settlements may require transferring IRA assets to a former spouse. Properly executed transfers via qualified domestic relations orders (QDROs) avoid taxes and penalties, but errors can trigger significant tax consequences.

Health Issues

Serious illness or disability might qualify you for penalty-free withdrawals. Additionally, increased medical expenses could create legitimate needs for accessing retirement funds earlier than originally planned.

Inheritance

Inheriting additional assets or an unexpected windfall might reduce your need for IRA withdrawals, allowing tax-deferred growth to continue. Conversely, estate settlement expenses might create short-term liquidity needs requiring distributions.

Career Changes

Returning to work after retirement or starting a business creates new income that might affect the optimal timing and amount of IRA withdrawals. Higher earned income could push you into higher tax brackets, making IRA distributions less attractive in those years.

Regularly reviewing your withdrawal strategy ensures it remains aligned with your evolving circumstances and goals.

Navigating rollover IRA withdrawal rules requires understanding age thresholds, penalty exceptions, tax implications, and strategic planning opportunities. The decisions you make about accessing these funds can significantly impact your long-term financial security and tax liability. Brookwood Investment Group offers personalized guidance through these complex decisions, helping you develop withdrawal strategies aligned with your unique goals and circumstances. Schedule a consultation at Brookwood Investment Group to explore how professional planning can optimize your retirement income strategy while minimizing unnecessary taxes and penalties.