Managing personal finances in 2026 requires more than simple budgeting skills. Between market volatility, evolving tax laws, and complex retirement vehicles, navigating your financial future demands expertise and strategic planning. A personal financial advisor serves as a professional guide who analyzes your unique circumstances, helps establish clear objectives, and develops tailored strategies to pursue your financial goals. Whether you're planning for retirement, managing investments, or structuring your estate, working with a qualified advisor can provide the clarity and direction needed to make informed decisions throughout different life stages.

Understanding the Role of a Personal Financial Advisor

A personal financial advisor provides comprehensive guidance across multiple aspects of wealth management. Unlike transactional brokers or product salespeople, these professionals take a holistic approach to your financial situation. Research from EBSCO indicates that personal financial advisors assess clients' current financial status, identify goals, and develop customized plans to help achieve those objectives.

The scope of services typically includes several key areas:

- Retirement planning to help structure income strategies for your post-working years

- Investment management focused on building portfolios aligned with your risk tolerance

- Tax strategy development to potentially enhance after-tax returns

- Estate planning coordination to help organize wealth transfer according to your wishes

- Insurance analysis to evaluate coverage needs and identify potential gaps

The Fiduciary Standard

One critical distinction when selecting a personal financial advisor involves understanding the fiduciary standard. Fiduciary advisors are legally obligated to act in their clients' best interests, putting client welfare ahead of their own compensation. This differs from the suitability standard, which only requires recommendations to be suitable rather than optimal.

When evaluating potential advisors, understanding fee-only financial advice and what it really means becomes essential. Fee-only advisors receive compensation directly from clients rather than commissions from product sales, which can help minimize potential conflicts of interest. This structure aligns the advisor's success with your progress toward financial goals.

How to Select the Right Personal Financial Advisor

Choosing a personal financial advisor represents a significant decision that impacts your financial future. The selection process requires careful evaluation of credentials, compensation structures, and service approaches. NerdWallet’s comprehensive guide on choosing a financial advisor emphasizes several critical factors to consider during your search.

Key Credentials to Verify

Professional designations signal expertise and commitment to ongoing education. The Certified Financial Planner (CFP®) credential remains widely recognized and requires rigorous examination, experience requirements, and adherence to ethical standards. Other valuable designations include Chartered Financial Analyst (CFA), Certified Public Accountant (CPA), and Chartered Financial Consultant (ChFC).

Beyond credentials, verify the advisor's registration status through regulatory databases. Most advisors register with either the Securities and Exchange Commission (SEC) or state securities regulators, depending on assets under management. This registration provides transparency through Form ADV disclosures, which detail business practices, fee structures, and any disciplinary history.

Compensation Models Explained

Personal financial advisors typically operate under one of several compensation structures:

| Compensation Type | How It Works | Potential Considerations |

|---|---|---|

| Fee-Only | Flat fees, hourly rates, or percentage of assets managed | Transparent pricing with fewer potential conflicts |

| Commission-Based | Earns commissions from product sales | May create incentives to recommend certain products |

| Fee-Based | Combination of fees and commissions | Mixed compensation requiring careful evaluation |

Understanding these structures helps you evaluate whether an advisor's recommendations might be influenced by compensation incentives. For unbiased guidance, many investors prefer fee-only advisors who operate under the fiduciary standard, similar to the approach taken by fiduciary planning professionals.

The Value of Personalized Financial Guidance

Generic financial advice rarely addresses individual circumstances effectively. A personal financial advisor tailors strategies to your specific situation, considering factors like income sources, family structure, risk tolerance, time horizon, and personal values. This customization extends beyond simple asset allocation to encompass comprehensive life planning.

Recent Gallup research reveals that Americans increasingly seek financial guidance from trusted professional advisors rather than relying solely on impersonal online resources. This trend underscores the value of human expertise in navigating complex financial decisions that algorithms alone cannot adequately address.

Building Your Financial Strategy

Working with a personal financial advisor typically begins with discovery conversations to understand your current position and future aspirations. This process involves:

- Comprehensive data gathering about assets, liabilities, income, and expenses

- Goal identification and prioritization across short-term and long-term objectives

- Risk assessment to determine appropriate investment approaches

- Strategy development incorporating retirement planning, tax considerations, and estate structuring

- Implementation and ongoing monitoring with regular reviews and adjustments

This systematic approach provides structure while remaining flexible enough to adapt as circumstances change. Major life events like career transitions, inheritances, marriage, divorce, or health changes all warrant strategy reassessment with your advisor.

Retirement Planning Expertise

Retirement planning represents one of the most complex areas where a personal financial advisor provides significant value. The transition from accumulation to distribution requires careful coordination across multiple accounts, income sources, and tax considerations. Understanding retirement planning and estate planning as interconnected disciplines helps create more comprehensive strategies.

Income Strategy Development

Creating sustainable retirement income involves more than simply withdrawing from savings. A personal financial advisor helps structure withdrawal strategies that consider:

- Social Security optimization through timing decisions that maximize lifetime benefits

- Pension distribution options when applicable, evaluating lump sum versus annuity choices

- Required minimum distribution (RMD) planning to minimize tax impact from traditional retirement accounts

- Tax-efficient withdrawal sequencing across taxable, tax-deferred, and tax-free accounts

- Longevity risk management to help ensure resources last throughout retirement

The complexity increases when coordinating these elements while preserving assets for potential long-term care needs, legacy goals, or unexpected expenses.

Investment Management in Retirement

Investment strategies typically shift as you transition into retirement. While growth remains important to combat inflation, capital preservation and income generation gain priority. A personal financial advisor adjusts asset allocation, rebalances portfolios, and monitors risk exposure relative to withdrawal needs.

This dynamic management responds to market conditions, economic trends, and changes in your situation. Rather than set-it-and-forget-it approaches, ongoing oversight helps align investments with evolving needs throughout retirement phases.

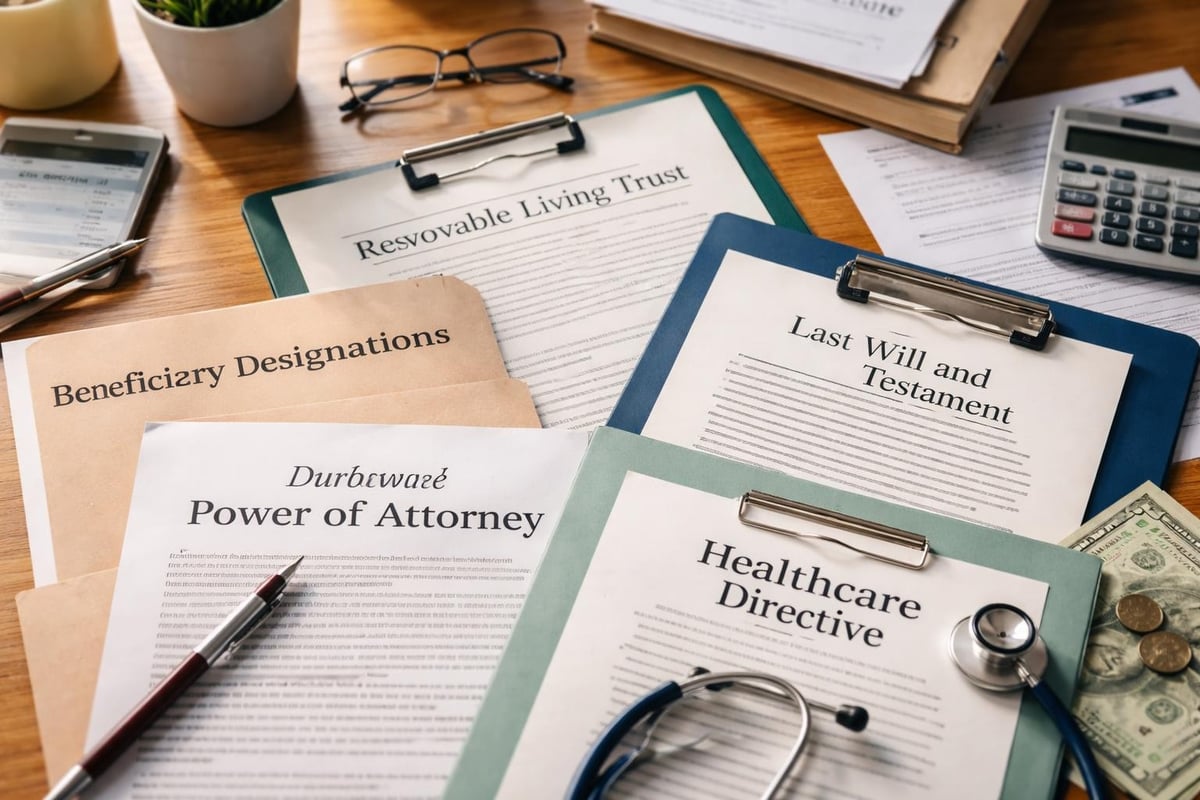

Estate Planning and Legacy Considerations

Estate planning extends beyond simple will preparation to encompass comprehensive wealth transfer strategies. A personal financial advisor coordinates with estate attorneys and tax professionals to help structure your legacy according to your values and objectives. Understanding the estate planning process reveals how financial advisors integrate estate considerations into overall planning.

Key Estate Planning Elements

Effective estate planning addresses several interconnected components:

| Estate Component | Purpose | Advisory Role |

|---|---|---|

| Will and Trusts | Direct asset distribution | Coordinate with attorneys on funding and beneficiary alignment |

| Beneficiary Designations | Transfer retirement and insurance assets | Ensure designations match overall estate goals |

| Power of Attorney | Authorize financial management if incapacitated | Help select appropriate agents and understand implications |

| Healthcare Directives | Communicate medical wishes | Support advance directive completion and family discussions |

| Tax Minimization | Reduce estate and inheritance taxes | Model tax scenarios and recommend strategies |

Your advisor helps ensure these elements work together cohesively rather than creating conflicting directives or unintended consequences.

Charitable Giving Strategies

For those with philanthropic interests, a personal financial advisor can structure giving strategies that maximize impact while potentially providing tax benefits. Options include donor-advised funds, charitable remainder trusts, qualified charitable distributions from IRAs, and strategic timing of contributions. These techniques align generosity with financial efficiency.

Tax Strategy and Planning

Tax planning represents an ongoing opportunity to potentially enhance after-tax returns and preserve more wealth. A personal financial advisor develops proactive tax strategies rather than simply reacting at year-end. This forward-looking approach considers how decisions across investments, retirement contributions, Roth conversions, and income timing affect your overall tax situation.

Proactive Tax Considerations

Effective tax planning involves year-round awareness of opportunities and risks. Strategies might include:

- Tax-loss harvesting to offset gains with strategic loss realization

- Roth conversion analysis during lower-income years before RMDs begin

- Capital gains management through timing of asset sales and holding periods

- Qualified opportunity zone investments for long-term growth potential

- Business entity structuring for entrepreneurs and business owners

Working with advisors who collaborate with CPAs or hold tax credentials themselves, such as those offering CPA financial advisor services, can provide integrated expertise across financial and tax domains.

The Virtual Advisory Experience

Technology transformation has enabled personal financial advisors to serve clients effectively without geographical constraints. Virtual-first advisory models provide personalized guidance through video conferencing, secure document sharing, and digital planning tools. This approach offers convenience while maintaining the personal relationship essential to effective financial planning.

Benefits of Virtual Financial Guidance

Modern advisory relationships leverage technology to enhance service delivery:

- Flexible meeting scheduling without commute time or location constraints

- Secure document exchange through encrypted portals protecting sensitive information

- Real-time collaboration on financial plans and projections during virtual sessions

- Broader advisor access enabling selection based on expertise rather than geography

- Efficient communication through multiple channels suited to client preferences

Survey findings indicate that financial advisors are considered the most trusted source of financial guidance, demonstrating that professional expertise maintains its value regardless of service delivery method.

Ongoing Partnership and Relationship Management

The relationship with a personal financial advisor evolves as an ongoing partnership rather than a one-time transaction. Regular review meetings provide opportunities to assess progress, adjust strategies, and address new concerns. This continuity enables advisors to develop deep understanding of client situations, preferences, and goals over time.

What to Expect from Regular Reviews

Typical review meetings cover several standard agenda items:

- Performance assessment across investment portfolios and financial goals

- Life change discussions regarding family, career, health, or other circumstances

- Strategy adjustments based on market conditions or regulatory changes

- Goal progress tracking with updates to financial plans and projections

- New opportunity evaluation for potential enhancements to existing strategies

Between scheduled reviews, proactive advisors reach out when significant market events, tax law changes, or other developments warrant client awareness. This attentive service distinguishes engaged advisory relationships from passive account management.

Evaluating Advisory Relationships

Periodic evaluation of your advisory relationship helps ensure continued alignment with your needs and expectations. Consider whether your advisor demonstrates thorough knowledge, communicates clearly, responds promptly, and proactively identifies opportunities relevant to your situation. Understanding how to vet financial advice provides frameworks for ongoing assessment.

Questions to Consider Annually

Reflect on these aspects of your advisory relationship:

- Does your advisor demonstrate understanding of your unique goals and concerns?

- Are recommendations clearly explained with rationale and alternatives presented?

- Do you receive proactive communication about relevant planning opportunities?

- Are fees transparent and reasonable relative to services provided?

- Does your advisor coordinate effectively with your other professional advisors?

Honest assessment of these factors helps determine whether your current relationship serves your best interests or whether exploring alternatives might be beneficial. Quality advisors welcome these evaluations as opportunities to strengthen client relationships and address any service gaps.

Industry Standards and Professional Organizations

Professional organizations establish standards that elevate the financial advisory profession. The National Association of Personal Financial Advisors (NAPFA) represents fee-only advisors committed to fiduciary service and comprehensive planning approaches. Membership in such organizations signals commitment to ethical standards and ongoing professional development.

Continuing Education Requirements

Reputable credentials require ongoing education to maintain current knowledge. CFP® professionals must complete 30 hours of continuing education every two years, including ethics training. This requirement ensures advisors stay informed about regulatory changes, planning strategies, and industry developments that affect client service.

When selecting a personal financial advisor, verify active credential status and ask about professional affiliations. These indicators suggest commitment to excellence beyond minimum regulatory requirements.

Making Informed Financial Decisions

Ultimately, working with a personal financial advisor empowers you to make financial decisions from an informed position. Rather than replacing your judgment, advisors provide expertise, analysis, and perspective that enhances decision-making quality. This collaborative approach respects your autonomy while leveraging professional knowledge.

The value extends beyond investment returns to encompass peace of mind, time savings, and confidence that your financial affairs align with your life goals. For many individuals and families, this comprehensive guidance represents one of the most impactful professional relationships they establish.

Finding reliable financial advice requires diligence in advisor selection, clear communication about expectations, and willingness to engage actively in the planning process. The most successful advisory relationships feature mutual respect, transparent communication, and shared commitment to pursuing your financial objectives.

Navigating today's complex financial landscape requires expertise across retirement planning, investment management, tax strategy, and estate planning. A personal financial advisor who operates as a fiduciary partner can provide the personalized guidance needed to pursue your unique goals with confidence. If you're seeking comprehensive financial advice tailored to your specific situation and delivered through convenient virtual meetings, Brookwood Investment Group LLC offers fiduciary advisory services designed around your lifestyle and objectives. Schedule a conversation to explore how personalized financial guidance might support your path forward.