Transitioning from wealth accumulation to income distribution represents one of the most significant financial shifts retirees face. Selecting the best retirement income funds requires careful evaluation of risk tolerance, income needs, and long-term sustainability. As retirees navigate 2026's investment landscape, understanding how various fund structures generate income, manage volatility, and preserve capital becomes essential for maintaining financial independence throughout retirement.

Understanding Retirement Income Fund Categories

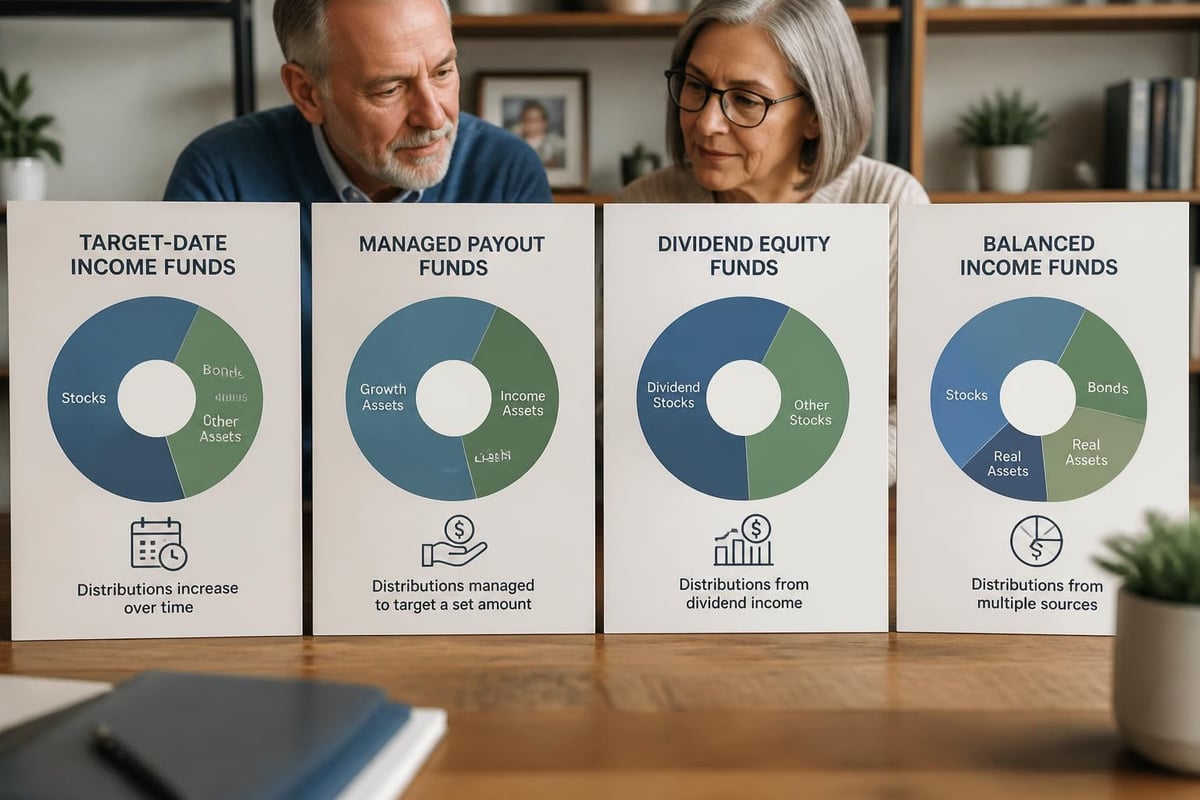

Retirement income funds come in several distinct categories, each designed to address different aspects of generating sustainable cash flow. Target-date income funds automatically adjust asset allocation to become more conservative over time, while managed distribution funds provide systematic monthly or quarterly payments. Understanding these structural differences helps investors align fund selection with their specific income requirements.

Target-date retirement income funds typically maintain a fixed allocation once they reach their target date, usually around 30-40% equities and 60-70% bonds and cash equivalents. These funds appeal to retirees seeking a simplified, hands-off approach to portfolio management.

Managed payout funds operate differently by establishing a specific distribution rate, often between 3-5% annually. Fund managers determine the payout schedule and adjust the portfolio to sustain these distributions while attempting to preserve principal.

How Income Generation Strategies Differ

Different fund categories employ varying strategies to generate income:

- Dividend-focused equity funds invest in established companies with strong dividend payment histories

- Bond funds generate income through interest payments from government, municipal, or corporate debt

- Balanced funds combine dividend stocks and bonds to create multiple income streams

- Multi-asset funds incorporate real estate investment trusts, preferred stocks, and alternative investments

The Vanguard Target Retirement Income Fund exemplifies how major providers structure these products, maintaining approximately 30% stock allocation alongside bond and short-term reserves to balance growth potential with income stability.

Evaluating the Best Retirement Income Funds

When assessing potential retirement income funds, several quantitative and qualitative factors deserve thorough examination. Fund performance over complete market cycles provides more meaningful insights than short-term returns, particularly during periods of market stress.

| Evaluation Criteria | Why It Matters | Target Benchmark |

|---|---|---|

| Distribution Yield | Measures annual income generated | 3-5% for balanced funds |

| Expense Ratio | Impacts net returns over time | Below 0.75% preferred |

| Distribution Consistency | Indicates sustainability | 5+ years stable payments |

| Total Return | Combines income and growth | Matches or exceeds inflation |

| Volatility (Standard Deviation) | Assesses risk level | Lower than pure equity funds |

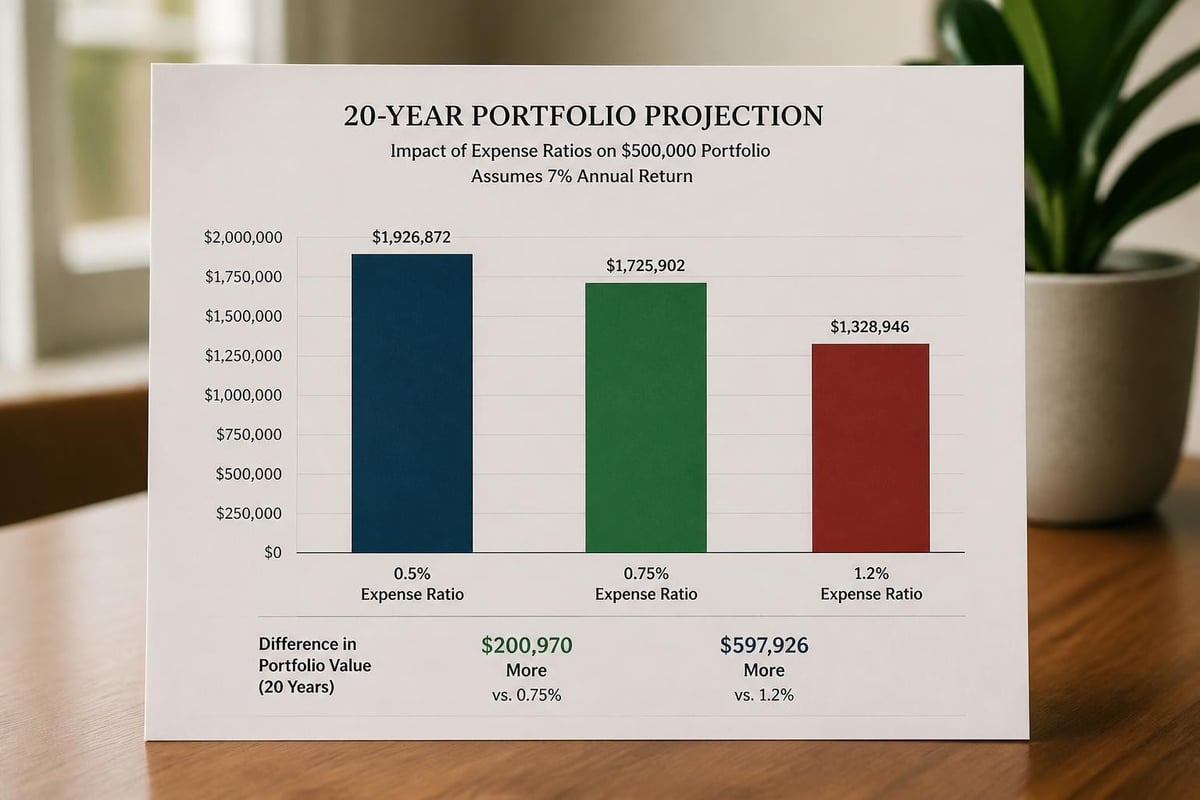

The expense ratio significantly impacts long-term outcomes. A fund charging 1.2% versus one charging 0.5% can reduce portfolio value by hundreds of thousands of dollars over a 20-30 year retirement.

Distribution Sustainability Analysis

Understanding how funds maintain distributions helps assess long-term viability. Some funds distribute only earned income from dividends and interest, while others include return of capital, which gradually reduces the principal balance. Return of capital distributions aren't inherently problematic, but investors should understand this mechanism.

Funds that consistently distribute more than they earn through dividends and capital gains may eventually reduce payments or deplete assets. Reviewing the fund's distribution sources in annual reports reveals whether payments come from sustainable income or principal erosion.

Working with fiduciary advisory services helps investors analyze these complex distribution mechanics and understand their long-term implications.

Top Fund Categories for Retirement Income in 2026

The landscape of best retirement income funds includes several proven categories that have demonstrated consistent performance across varying market conditions. Each category serves different investor needs based on risk tolerance, income requirements, and time horizon.

Conservative Allocation Funds

Conservative allocation funds maintain 20-40% equity exposure while emphasizing high-quality bonds and stable-value investments. These funds prioritize capital preservation while generating moderate income, making them suitable for retirees with lower risk tolerance or those in early retirement stages.

Conservative retirement investments typically include short-to-intermediate term bond funds, high-quality corporate bonds, and dividend-paying blue-chip stocks. These components work together to provide steady income while minimizing principal volatility.

Dividend Growth Funds

Rather than focusing solely on current yield, dividend growth funds invest in companies with histories of regularly increasing dividend payments. This approach helps retirement income keep pace with inflation over time, addressing one of retirees' primary concerns.

These funds typically invest in established companies across sectors including:

- Consumer staples with pricing power

- Healthcare companies with recurring revenue models

- Financial institutions with strong capital positions

- Utilities with regulated rate structures

- Technology firms generating substantial free cash flow

The combination of current income and dividend growth potential makes these funds valuable components within a broader retirement income strategy.

Multi-Sector Bond Funds

Multi-sector bond funds provide diversification across various fixed-income categories, reducing concentration risk while seeking to optimize income generation. Fund managers actively adjust allocations between government bonds, investment-grade corporate bonds, high-yield bonds, and international debt based on market conditions.

This flexibility allows professional managers to navigate changing interest rate environments, credit cycles, and economic conditions while maintaining consistent income distributions.

Implementing a Retirement Income Fund Strategy

Successful implementation extends beyond simply selecting high-performing funds. Strategic portfolio construction considers how different funds interact, total fee impact, tax efficiency, and withdrawal sequencing. These factors collectively determine whether a retirement income strategy successfully sustains purchasing power throughout retirement.

The Bucket Approach Integration

Many financial advisors recommend integrating retirement income funds within a bucket strategy framework. This approach divides assets into time-based segments:

- Immediate needs bucket (0-2 years): Money market funds and short-term bonds

- Short-term bucket (2-5 years): Conservative income funds and intermediate bonds

- Medium-term bucket (5-10 years): Balanced income funds with moderate equity exposure

- Long-term bucket (10+ years): Growth-oriented funds including dividend growth strategies

This structure ensures sufficient liquidity for near-term expenses while maintaining growth potential for later retirement years. The retirement income strategies outlined by financial planning experts emphasize this time-segmented approach.

Tax-Efficient Fund Placement

Where you hold retirement income funds significantly impacts after-tax returns. Tax-deferred accounts like traditional IRAs and 401(k)s suit taxable bond funds and REITs, while taxable accounts work better for tax-efficient equity income funds and municipal bond funds.

| Account Type | Optimal Fund Placement | Reasoning |

|---|---|---|

| Traditional IRA/401(k) | Taxable bond funds, REITs | Shields high ordinary income from current taxation |

| Roth IRA | Dividend growth funds | Tax-free growth benefits long-term appreciation |

| Taxable Brokerage | Municipal bonds, qualified dividends | Preferential tax treatment already exists |

| Health Savings Account | Conservative balanced funds | Triple tax advantage for medical expenses |

Retirement planning professionals help optimize this fund placement strategy based on individual tax situations and income needs.

Risk Management Considerations

While seeking the best retirement income funds, risk management remains paramount. Retiree portfolios face unique vulnerabilities including sequence of returns risk, inflation erosion, and longevity risk. Building appropriate safeguards into fund selection helps mitigate these threats.

Sequence of Returns Risk

Market downturns early in retirement create disproportionate damage when combined with ongoing withdrawals. Selling assets during market declines locks in losses and reduces the portfolio's recovery potential. Income-focused funds help address this risk by generating distributions without forced asset sales.

Funds maintaining adequate cash reserves and shorter-duration bonds provide flexibility during market stress. This liquidity allows retirees to draw income from stable sources rather than selling equity positions at disadvantageous prices.

Inflation Protection Mechanisms

Inflation represents a persistent threat to retirement purchasing power. A 3% annual inflation rate reduces purchasing power by approximately 45% over 20 years. The best retirement income funds incorporate inflation mitigation strategies through several mechanisms.

Treasury Inflation-Protected Securities (TIPS) adjust principal values based on Consumer Price Index changes, ensuring bond values keep pace with inflation. Some retirement income funds maintain 10-20% TIPS allocations specifically for inflation protection.

Dividend growth stocks historically outpace inflation as companies increase dividends over time. Quality companies raise dividends at rates exceeding inflation, providing natural inflation hedging within equity allocations.

Real estate exposure through REITs offers another inflation hedge, as property values and rents typically rise with general price levels.

Understanding how different investment management approaches address inflation helps retirees select appropriate fund combinations.

Active Versus Passive Retirement Income Funds

The active versus passive management debate takes on different dimensions within retirement income investing. While passive index funds offer lower costs, actively managed income funds may provide valuable expertise in areas like credit analysis, duration management, and dividend sustainability assessment.

When Active Management Adds Value

Active management potentially benefits retirement income investors in several scenarios:

- High-yield bond markets where credit analysis identifies default risks

- Dividend stock selection separating sustainable payers from dividend traps

- Duration management adjusting bond maturity profiles as interest rates change

- Sector rotation shifting allocations based on economic cycles

These value-added activities justify higher fees when managers consistently demonstrate skill. However, many actively managed funds fail to outperform after accounting for their higher expense ratios.

The Case for Index-Based Income Funds

Low-cost index funds tracking dividend aristocrats, investment-grade bonds, or balanced allocations offer compelling alternatives. Their transparency, low turnover, and minimal expenses support long-term wealth preservation.

For retirees implementing systematic withdrawal strategies, low-cost index funds combined with disciplined rebalancing often produce outcomes comparable to actively managed alternatives while retaining more assets through reduced fee drag.

The optimal 401(k) investment options discussion highlights both approaches within employer-sponsored retirement accounts.

Monitoring and Adjusting Your Income Fund Portfolio

Retirement income planning requires ongoing attention rather than set-and-forget implementation. Regular portfolio reviews ensure funds continue meeting income needs, risk parameters remain appropriate, and asset allocation aligns with changing market conditions and personal circumstances.

Quarterly Review Checklist

Effective portfolio monitoring follows a structured approach:

- Verify distribution consistency: Confirm funds maintain expected payment schedules

- Assess yield changes: Monitor whether yields remain within target ranges

- Review total returns: Evaluate whether portfolio value keeps pace with withdrawal rates

- Check expense ratios: Ensure fees haven't increased unexpectedly

- Examine holdings changes: Review significant shifts in fund composition

These reviews identify potential issues before they significantly impact retirement security. Working with financial planning and investment management professionals provides objective oversight and expertise in interpreting portfolio data.

When to Consider Fund Replacements

Several triggers warrant considering fund replacements within a retirement income portfolio:

- Sustained distribution cuts suggesting sustainability problems

- Manager changes at actively managed funds with strong track records

- Significant expense ratio increases reducing net returns

- Strategy drift where fund deviates from stated objectives

- Better alternatives emerging with superior risk-adjusted returns

However, excessive trading introduces transaction costs and potential tax consequences. Establishing clear criteria for fund changes prevents reactive decision-making based on short-term performance fluctuations.

Integration with Other Retirement Income Sources

The best retirement income funds function as components within comprehensive retirement income plans rather than standalone solutions. Coordinating fund distributions with Social Security benefits, pension payments, and annuity income creates a more robust and tax-efficient retirement income stream.

Coordinating Multiple Income Sources

Strategic coordination involves timing and sequencing decisions across various income sources:

Social Security optimization considers whether delaying benefits to age 70 makes sense when retirement income funds can bridge the gap. The guaranteed 8% annual increase from delayed claiming often justifies drawing from investments during early retirement years.

Pension decisions including lump-sum versus annuity elections interact with retirement income fund needs. Retirees with substantial guaranteed income may accept more volatility in fund selections, while those without pensions might prioritize stability.

Required Minimum Distributions (RMDs) beginning at age 73 in 2026 force withdrawals from tax-deferred accounts. Planning fund placements and withdrawal sequencing around RMDs optimizes tax efficiency.

Planning advice from experienced advisors helps navigate these complex coordination challenges.

Healthcare Cost Considerations

Healthcare expenses represent significant and unpredictable retirement costs. Medicare premiums, supplemental insurance, prescription drugs, and long-term care needs require dedicated funding consideration within retirement income planning.

Some retirees dedicate specific fund allocations to healthcare expenses, using conservative bond funds or money market vehicles for near-term medical costs while maintaining growth-oriented positions for potential long-term care needs decades into retirement.

Common Mistakes When Selecting Retirement Income Funds

Even experienced investors make predictable errors when building retirement income portfolios. Understanding these common pitfalls helps retirees avoid costly mistakes that jeopardize long-term financial security.

Chasing Yield Without Risk Assessment

The highest-yielding funds often carry elevated risks including credit risk, interest rate sensitivity, or concentration in volatile sectors. A fund yielding 8% might seem attractive compared to one yielding 4%, but understanding the risk-return tradeoff proves essential.

High yields sometimes signal:

- Elevated default risk in high-yield bond funds

- Dividend sustainability questions in equity income funds

- Return of capital distributions that gradually deplete principal

- Leverage usage amplifying both gains and losses

Proper due diligence examines why a fund offers above-market yields rather than simply accepting distributions at face value.

Ignoring Total Return

Focusing exclusively on distribution yield while ignoring capital appreciation or depreciation provides an incomplete picture. A fund distributing 5% annually while losing 3% in principal value delivers only 2% total return. Conversely, a fund yielding 3% while appreciating 4% provides 7% total return.

Retirement income funds designed for cash flow balance distribution rates with total return objectives to maintain purchasing power throughout retirement.

Excessive Portfolio Complexity

Holding too many overlapping funds creates unnecessary complexity without meaningful diversification benefits. A portfolio with fifteen different income funds likely contains significant overlap, making performance tracking difficult and increasing total expenses.

Most retirees achieve adequate diversification with 4-8 carefully selected funds spanning different asset classes and strategies. Simplicity facilitates better decision-making and reduces the cognitive burden of portfolio management.

Fund Selection Resources and Research Tools

Identifying the best retirement income funds requires access to quality research and analytical tools. Several resources help investors evaluate fund options, compare performance metrics, and understand portfolio holdings.

Professional Rating Services

Morningstar, Lipper, and other rating services provide independent fund analysis including:

- Risk-adjusted return measurements

- Peer group comparisons

- Manager tenure and experience

- Portfolio holdings transparency

- Fee analysis and total cost projections

These services assign ratings based on historical performance, but past results don't guarantee future outcomes. Using ratings as screening tools rather than definitive selection criteria produces better outcomes.

Fund Company Resources

Major fund families provide extensive educational materials, research reports, and portfolio analysis tools. Vanguard, Fidelity, T. Rowe Price, and other providers offer retirement income calculators, distribution projection tools, and asset allocation guidance.

These resources, while valuable, naturally promote the provider's own fund offerings. Cross-referencing multiple sources and maintaining objectivity during research prevents undue influence from any single provider's marketing materials.

Working with Fiduciary Advisors

Fiduciary planning professionals legally obligate themselves to act in clients' best interests, providing unbiased guidance without conflicts of interest from product sales commissions. This structural advantage proves particularly valuable when selecting retirement income funds from thousands of available options.

Experienced advisors bring expertise in areas including tax optimization, estate planning integration, risk management, and behavioral coaching that extends well beyond simple fund selection. The value of comprehensive advice often exceeds its cost through improved outcomes and avoided mistakes.

Selecting the best retirement income funds requires balancing multiple objectives including sustainable income generation, capital preservation, inflation protection, and appropriate risk management. Success depends on understanding fund structures, evaluating options objectively, and integrating selections within comprehensive retirement income strategies.

Brookwood Investment Group LLC provides personalized guidance through the complexities of retirement income planning, helping clients build portfolios aligned with their unique goals, risk tolerance, and income needs. As a fiduciary advisory firm, Brookwood offers objective recommendations on fund selection, portfolio construction, and ongoing monitoring to support confident retirement living. Contact Brookwood Investment Group today to discuss how professional financial guidance can help secure your retirement income strategy.