High-income earners frequently face challenges when building tax-advantaged retirement portfolios due to IRS income restrictions on direct Roth IRA contributions. The backdoor Roth IRA strategy has emerged as a powerful technique that allows individuals earning above threshold limits to access the significant benefits of Roth IRA accounts, including tax-free growth and tax-free qualified withdrawals in retirement. Understanding this sophisticated approach requires careful attention to contribution rules, tax implications, and timing considerations.

Understanding Income Limits and the Backdoor Strategy

The IRS establishes strict income limits for direct Roth IRA contributions each year. For 2026, single filers with modified adjusted gross income above $161,000 and married couples filing jointly earning more than $240,000 face reduced or eliminated contribution eligibility. These thresholds create significant barriers for physicians, executives, business owners, and other high-earning professionals.

The backdoor Roth IRA strategy provides a legitimate workaround that enables these individuals to build Roth accounts regardless of income level. This approach involves two distinct steps: making a non-deductible contribution to a traditional IRA, then converting that contribution to a Roth IRA. Since the IRS does not impose income limits on traditional IRA contributions or Roth conversions, this two-step process effectively circumvents the direct contribution restrictions.

How Traditional IRA Rules Enable This Strategy

Traditional IRAs accept contributions from anyone with earned income, regardless of how much they earn. While high-income earners typically cannot deduct these contributions on their tax returns when they also participate in workplace retirement plans, they can still make non-deductible contributions up to the annual limit.

For 2026, the contribution limit remains $7,000 for individuals under age 50, with an additional $1,000 catch-up contribution allowed for those 50 and older. These limits apply across all IRA accounts combined, meaning you must coordinate contributions between traditional and Roth IRAs to avoid exceeding the maximum.

Executing a Backdoor Roth IRA Conversion

Implementing this strategy requires methodical execution to maintain compliance and minimize tax complications. The mechanics of executing a backdoor Roth IRA conversion involve specific steps that should be completed with precision.

Step-by-step conversion process:

- Open a traditional IRA if you don't already have one designated for this purpose

- Make a non-deductible contribution to the traditional IRA and document it properly on Form 8606

- Wait briefly for the contribution to clear and settle in your account

- Execute the Roth conversion by instructing your custodian to transfer the funds

- Report the conversion on your tax return using Form 8606 to track basis

The timing between contribution and conversion has been subject to debate. While some advisors previously recommended waiting several months, the IRS has not established a specific waiting period. Many practitioners now suggest converting shortly after contribution to minimize potential earnings that would be taxable upon conversion.

Tax Implications and Form 8606

When you convert funds from a traditional IRA to a Roth IRA, you must pay ordinary income tax on any amount that hasn't already been taxed. For a straightforward backdoor Roth IRA where you contribute and immediately convert, the taxable amount should be minimal-only any small earnings generated between contribution and conversion.

Form 8606 serves as your official record of non-deductible IRA contributions. This form tracks your basis in traditional IRAs, which represents the after-tax money you've contributed. Accurate completion of this form each year proves essential for avoiding double taxation and maintaining clear records.

| Tax Scenario | Contribution | Earnings Before Conversion | Taxable Amount |

|---|---|---|---|

| Immediate conversion | $7,000 | $15 | $15 |

| 3-month delay | $7,000 | $250 | $250 |

| 1-year delay | $7,000 | $700 | $700 |

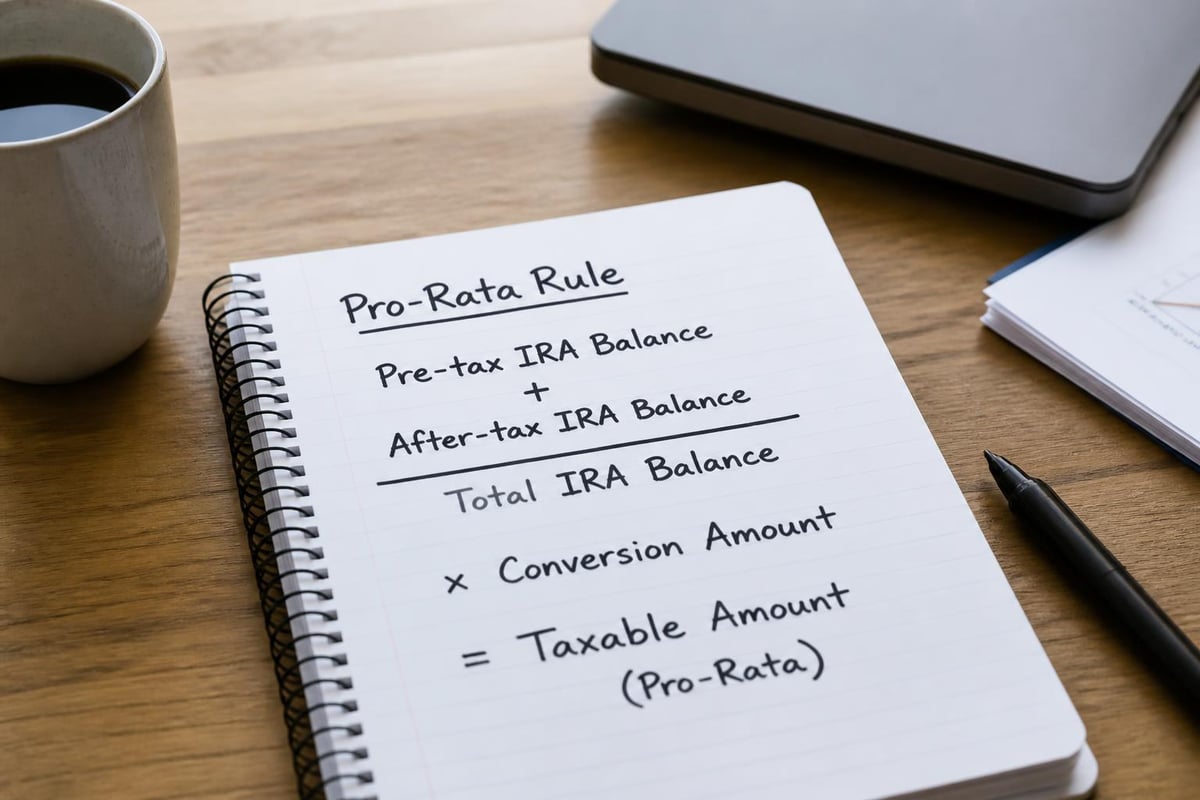

The Pro-Rata Rule and Its Impact

The most significant complication in backdoor Roth IRA planning involves the pro-rata rule, which can create substantial unexpected tax bills. This rule requires that when you convert traditional IRA funds to a Roth, you must calculate the taxable portion based on the ratio of pre-tax to after-tax dollars across all your traditional, SEP, and SIMPLE IRA accounts combined.

Consider an example: You have $93,000 in an existing traditional IRA from pre-tax contributions and make a new $7,000 non-deductible contribution, giving you $100,000 total. When you convert the $7,000, the IRS views this as converting 7% of your total IRA balance, not just the recent contribution. Since only 7% of your total balance consists of after-tax money, 93% of your conversion-approximately $6,510-becomes taxable income.

Strategies to Navigate the Pro-Rata Rule

High-income professionals can employ several approaches to minimize pro-rata rule complications:

- Roll pre-tax IRA funds into a 401(k) if your employer plan accepts incoming rollovers

- Complete the rollover before year-end when you plan to execute the conversion

- Maintain separate tracking of after-tax contributions through diligent Form 8606 filing

- Consider the mega backdoor Roth as an alternative if available through your employer

Working with fiduciary advisors who understand these nuances ensures you structure conversions in the most tax-efficient manner possible.

Mega Backdoor Roth IRA Strategy

For individuals seeking to contribute significantly more than the standard IRA limits, the mega backdoor Roth IRA strategy offers compelling opportunities. This advanced approach utilizes after-tax 401(k) contributions beyond the standard employee deferral limit.

In 2026, the total 401(k) contribution limit across all sources reaches $70,000 for those under 50 ($77,500 for those 50 and older). After maximizing employee deferrals at $23,500 and receiving any employer match, you may have room to make additional after-tax contributions if your plan allows.

Requirements for mega backdoor Roth implementation:

- Employer 401(k) plan must permit after-tax contributions

- Plan must allow in-service distributions or in-plan Roth conversions

- Total contributions cannot exceed annual 401(k) limits

- Timing considerations to minimize earnings taxation

Not all employer plans offer these features, making this strategy more limited in availability. However, for those with access, the mega backdoor Roth can facilitate annual Roth contributions of $30,000 to $40,000 or more, dramatically accelerating tax-free retirement savings accumulation.

Tax Planning Considerations

Understanding the tax implications of backdoor Roth IRA conversions requires a comprehensive view of your entire financial situation. Tax implications during conversion extend beyond just the conversion amount itself.

The additional taxable income from conversions may push you into a higher marginal tax bracket, trigger the 3.8% Net Investment Income Tax, or affect other income-based benefits and credits. Coordinating conversion timing with retirement planning strategies becomes essential.

Optimal Timing for Conversions

Several factors influence when to execute backdoor Roth IRA conversions:

| Timing Factor | Consideration | Impact |

|---|---|---|

| Income fluctuations | Execute during lower-income years | Reduces marginal tax rate on conversion |

| Market volatility | Convert when account values decline | Minimizes taxable amount |

| Year-end planning | Complete before December 31 | Allows full tax-year preparation |

| Multi-year strategy | Spread conversions across years | Manages tax bracket creep |

Converting earlier in your career when income might be lower, or during years with unusual deductions or losses, can optimize the tax efficiency of this strategy. Strategic tax planning integrates these conversions with your broader financial objectives.

Estate Planning Benefits

Beyond immediate tax advantages, the backdoor Roth IRA strategy offers valuable estate planning benefits that extend to your heirs. Backdoor Roth IRAs for estate planning purposes deserve consideration in comprehensive wealth transfer strategies.

Roth IRAs do not require distributions during the original owner's lifetime, allowing assets to grow tax-free for decades. Upon inheritance, beneficiaries can continue enjoying tax-free qualified distributions, though they generally must empty inherited Roth IRAs within 10 years under current SECURE Act rules.

This tax-free distribution feature provides significant advantages over inherited traditional IRAs, where beneficiaries must pay ordinary income tax on all distributions. For high-earning heirs in elevated tax brackets, inheriting Roth assets rather than traditional IRA assets can preserve substantially more wealth.

Common Mistakes to Avoid

Even experienced investors make errors when implementing backdoor Roth IRA strategies. Awareness of common pitfalls helps ensure successful execution.

Frequently encountered mistakes:

- Failing to file Form 8606 creates no record of non-deductible contributions

- Waiting too long between contribution and conversion generates unnecessary taxable earnings

- Overlooking existing traditional IRA balances triggers unexpected pro-rata taxation

- Missing the contribution deadline of the tax filing deadline including extensions

- Commingling deductible and non-deductible contributions complicates basis tracking

Many of these errors can be corrected, but prevention through proper planning and professional guidance remains preferable. Working with experienced financial advisors who regularly implement these strategies significantly reduces error risk.

Documentation and Record-Keeping

Maintaining thorough documentation throughout the backdoor Roth IRA process protects you during tax filing and potential IRS inquiries. Essential records include:

- Contribution confirmation statements from your IRA custodian

- Conversion documentation showing the date and amount transferred

- All Form 8606 filings from every year you make non-deductible contributions

- Worksheets calculating any pro-rata amounts

- Correspondence with custodians regarding the transactions

These records prove particularly important if you maintain IRAs across multiple institutions or have made both deductible and non-deductible contributions over the years.

Evaluating Whether This Strategy Fits Your Situation

Not every high-income earner benefits equally from backdoor Roth IRA conversions. Assessing whether this strategy aligns with your financial goals requires analyzing multiple personal factors.

Favorable scenarios for backdoor Roth implementation:

- Your income exceeds direct Roth IRA contribution limits

- You have minimal or no existing pre-tax IRA balances

- You expect to be in a similar or higher tax bracket in retirement

- You've maximized other tax-advantaged retirement accounts

- You seek estate planning benefits for heirs

Conversely, if you maintain substantial traditional IRA balances that cannot be rolled into a 401(k), the pro-rata rule might make backdoor Roth conversions less attractive. Similarly, if you anticipate significantly lower retirement income and tax rates, the immediate tax cost of conversions might outweigh future benefits.

Integration with Broader Retirement Planning

The backdoor Roth IRA represents just one component of comprehensive retirement planning. When evaluating Roth conversion strategies, consider how this approach complements other retirement savings vehicles.

Maintaining tax diversification across different account types-traditional retirement accounts, Roth accounts, and taxable investment accounts-provides flexibility in managing retirement income and taxes. This diversification allows you to strategically source withdrawals from different account types based on annual tax situations.

High-income professionals typically maximize 401(k) contributions, contribute to Health Savings Accounts when eligible, and then turn to backdoor Roth IRAs as an additional tax-advantaged savings opportunity. For those catching up on retirement savings, this layered approach accelerates wealth accumulation across multiple tax treatments.

Annual Review and Adjustments

Tax laws, income limits, and personal circumstances change regularly, requiring annual review of your backdoor Roth IRA strategy. Congress periodically considers legislation that could eliminate or modify the backdoor Roth approach, though such changes have not materialized as of 2026.

Reviewing your strategy each year ensures you:

- Adjust for updated contribution limits and income thresholds

- Reassess pro-rata rule implications if IRA balances have changed

- Optimize conversion timing based on current-year income projections

- Maintain accurate documentation and filing compliance

- Integrate new tax law changes affecting retirement accounts

Regular consultation with qualified financial advisors who monitor legislative developments keeps your strategy current and compliant.

Professional Guidance and Implementation

Given the complexity of backdoor Roth IRA planning, professional assistance often proves valuable. Tax professionals and financial advisors bring expertise in navigating pro-rata calculations, optimizing timing, and coordinating conversions with broader financial strategies.

Breaking down the backdoor Roth IRA strategy with professional guidance helps ensure accurate execution. Advisors can model the tax impact of conversions, identify opportunities to minimize complications, and integrate this strategy with estate planning, tax planning, and investment management.

Selecting advisors who work in a fiduciary capacity ensures they prioritize your best interests when recommending whether and how to implement backdoor Roth conversions. These professionals consider your complete financial picture rather than focusing narrowly on a single strategy.

The coordination required between contribution timing, conversion execution, tax reporting, and investment management across multiple accounts justifies the value of professional oversight. Many investors find that the tax savings and error avoidance achieved through professional guidance exceed advisory fees.

The backdoor Roth IRA strategy offers high-income earners a valuable pathway to access tax-free retirement growth and create lasting estate planning benefits, though proper execution requires careful attention to contribution rules, pro-rata calculations, and tax reporting requirements. Brookwood Investment Group specializes in helping clients navigate sophisticated retirement planning strategies like backdoor Roth conversions, integrating these techniques with personalized tax planning, investment management, and estate planning services tailored to your unique financial situation. Schedule a consultation with Brookwood Investment Group to explore how backdoor Roth IRA planning fits within your comprehensive financial strategy.