Entering retirement represents a significant financial transition, but the way you withdraw funds from your retirement accounts can dramatically impact your lifetime tax burden. Many retirees focus exclusively on accumulating assets during their working years, only to overlook the critical importance of withdrawal sequencing and tax planning during distribution. Understanding tax efficient retirement withdrawal strategies can help preserve wealth, reduce unnecessary tax liabilities, and extend the longevity of your retirement portfolio while maintaining your desired lifestyle.

Understanding the Tax Treatment of Different Account Types

Before implementing any withdrawal strategy, it's essential to understand how different retirement accounts are taxed. Your retirement savings likely span multiple account types, each with distinct tax characteristics that influence withdrawal decisions.

Traditional Tax-Deferred Accounts

Traditional IRAs and 401(k) plans represent the foundation of many retirement portfolios. Contributions to these accounts typically reduce taxable income in the year they're made, allowing investments to grow tax-deferred until withdrawal.

Key characteristics include:

- Withdrawals taxed as ordinary income at current tax rates

- Required minimum distributions (RMDs) beginning at age 73 (as of 2026)

- Early withdrawal penalties before age 59½ with certain exceptions

- No maximum income limits during distribution phase

The tax treatment of these accounts makes timing particularly important. Withdrawing too much in a single year can push you into higher tax brackets, while strategic distributions can help manage your overall tax liability.

Roth Accounts and Tax-Free Growth

Roth IRAs and Roth 401(k)s offer tax-free growth and distributions, provided certain conditions are met. While contributions are made with after-tax dollars, qualified withdrawals generate no additional tax liability.

These accounts provide significant advantages during retirement because they don't count toward taxable income calculations. This characteristic makes them valuable for managing tax diversification strategies and avoiding income-related surcharges.

| Account Type | Contribution Tax Treatment | Growth Tax Treatment | Withdrawal Tax Treatment | RMD Required |

|---|---|---|---|---|

| Traditional IRA | Tax-deductible | Tax-deferred | Ordinary income | Yes, age 73 |

| Roth IRA | After-tax | Tax-free | Tax-free (qualified) | No |

| Taxable Brokerage | After-tax | Taxable annually | Capital gains rates | No |

| HSA | Tax-deductible | Tax-free | Tax-free (medical) | No |

The Foundation: Withdrawal Sequencing Strategy

One of the most fundamental tax efficient retirement withdrawal strategies involves the order in which you tap different account types. Traditional wisdom suggests a specific sequence, though individual circumstances may warrant adjustments.

Standard Sequencing Approach

Many financial professionals recommend withdrawing from taxable accounts first, followed by tax-deferred accounts, and finally Roth accounts. This approach allows tax-advantaged accounts maximum time to grow while using the most tax-efficient sources first.

Taxable accounts offer several advantages as the first withdrawal source:

- Long-term capital gains receive preferential tax treatment compared to ordinary income

- Step-up in basis at death provides estate planning benefits

- Tax-loss harvesting opportunities can offset gains

- No required minimum distributions

- Flexibility in controlling annual taxable income

After depleting taxable accounts, the strategy typically shifts to traditional tax-deferred accounts. This sequence helps satisfy RMD requirements while preserving Roth assets for later years when other income sources may diminish.

Strategic Deviations from Standard Sequencing

However, strict adherence to this sequence may not always optimize tax efficiency. Consider scenarios where early Roth conversions or intentional tax-deferred withdrawals in low-income years can reduce lifetime tax liability.

For instance, retirees who stop working before claiming Social Security may experience several low-income years. During this window, strategically withdrawing from traditional accounts or converting to Roth IRAs can fill lower tax brackets efficiently.

Leveraging Tax Bracket Management

Understanding your position within the federal tax bracket structure enables sophisticated withdrawal planning. The goal is to recognize opportunities to accelerate or defer income based on current and projected future tax rates.

Filling Lower Tax Brackets Strategically

Rather than minimizing current-year taxes, focus on minimizing lifetime tax obligations. SmartAsset’s analysis of tax-efficient strategies demonstrates how filling lower tax brackets with traditional IRA distributions can prevent larger mandatory withdrawals later.

Consider a married couple filing jointly in 2026 with $60,000 in annual expenses. If they only withdraw what they need, they might stay in the 12% tax bracket. However, deliberately withdrawing additional funds up to the top of the 22% bracket-and converting the excess to a Roth IRA-could reduce future RMDs and prevent bracket creep when distributions become mandatory.

This approach becomes particularly valuable when:

- Current income falls below typical levels (early retirement years)

- Future income will increase due to RMDs, pensions, or Social Security

- Tax rates are expected to rise in future years

- Medicare Income-Related Monthly Adjustment Amount (IRMAA) thresholds are not at risk

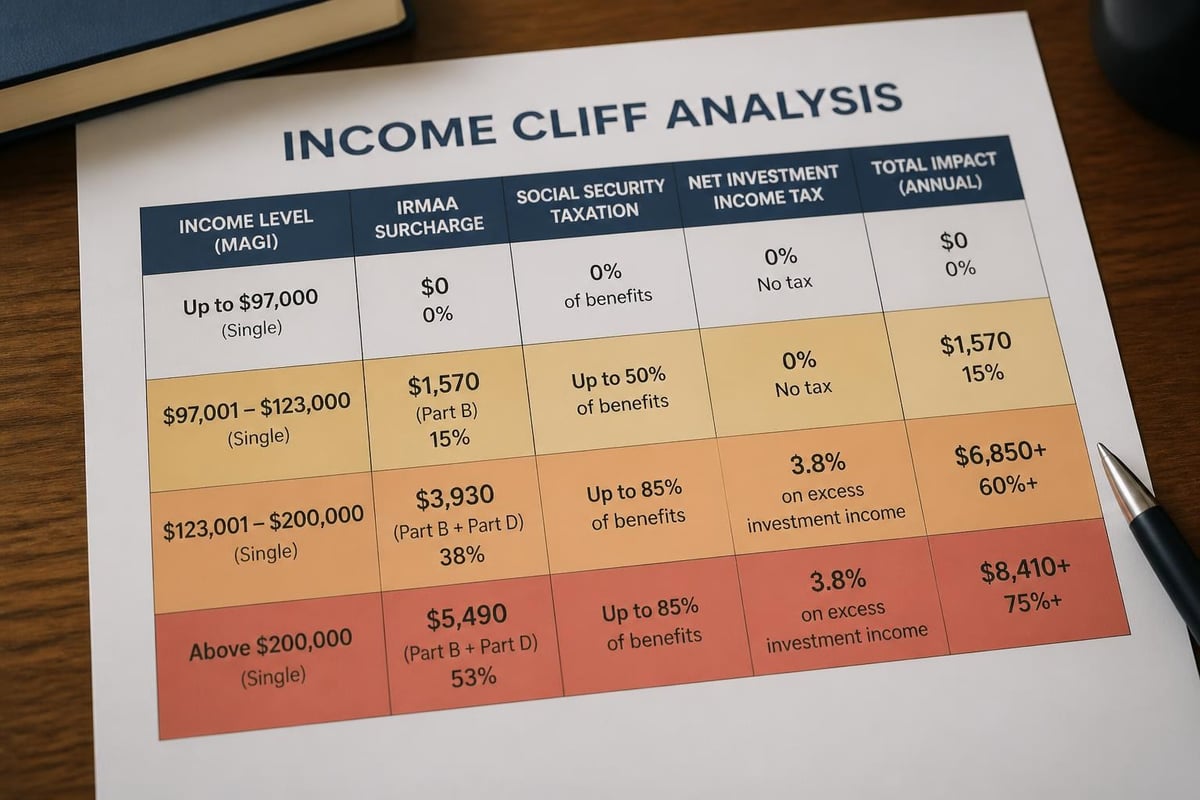

Avoiding Tax Torpedoes and Income Cliffs

Certain income thresholds trigger disproportionate tax consequences. The retirement rule of one more dollar illustrates how seemingly small income increases can trigger IRMAA surcharges, increased taxation of Social Security benefits, or loss of tax credits.

| Income Trigger | Consequence | Strategy to Avoid |

|---|---|---|

| IRMAA Thresholds | Higher Medicare premiums | Manage MAGI through Roth conversions |

| Social Security Taxation | Up to 85% of benefits taxable | Coordinate withdrawals with benefit timing |

| ACA Premium Credits | Loss of subsidies (if applicable) | Strategic income timing before Medicare |

| Net Investment Income Tax | Additional 3.8% surtax | Manage MAGI below $250,000 (married) |

Roth Conversion Strategies During Retirement

Roth conversions represent a powerful tool within tax efficient retirement withdrawal strategies. By converting traditional IRA assets to Roth accounts, you pay taxes now to secure tax-free growth and distributions later.

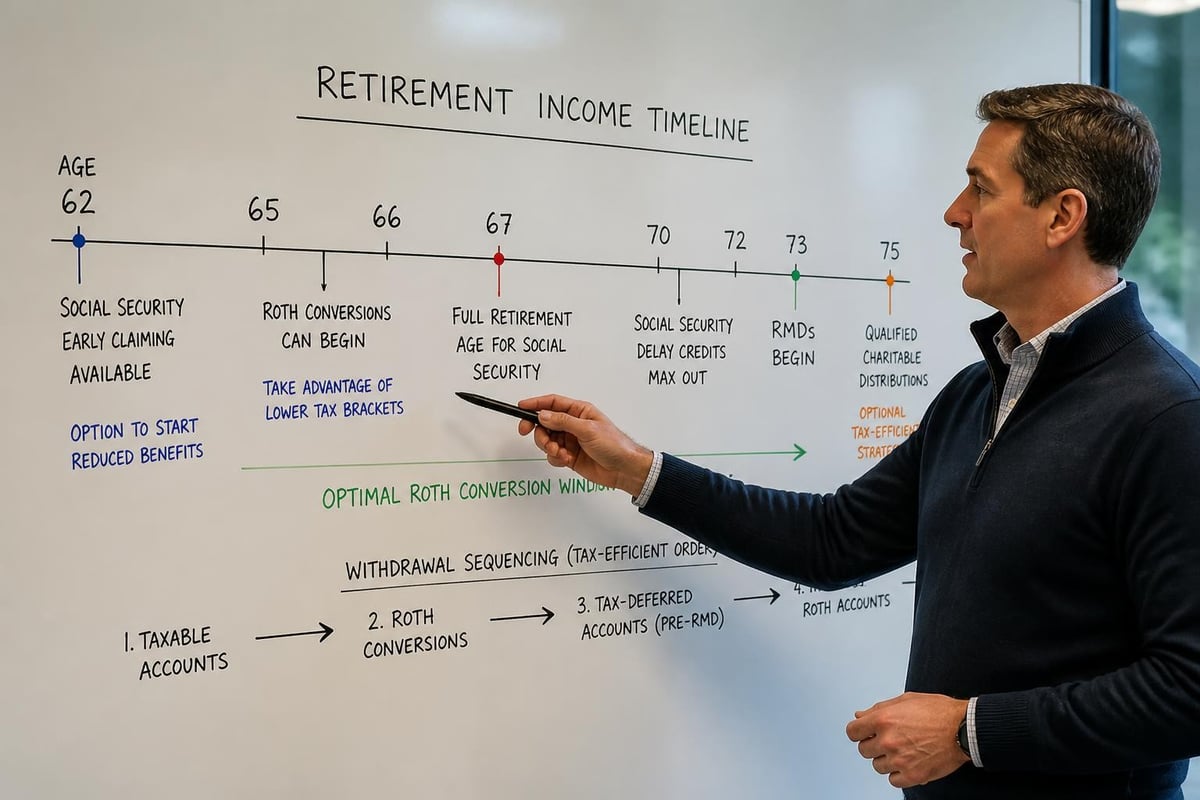

Optimal Conversion Windows

The most advantageous conversion opportunities often occur during specific retirement phases. Early retirement years before RMDs begin and before claiming Social Security typically offer the lowest marginal tax rates.

Three prime conversion windows include:

- The early retirement gap (age 60-73): After employment income ceases but before RMDs and Social Security begin

- Market downturn periods: Convert depreciated assets at lower tax cost with greater recovery potential

- Temporary income dips: Years with unusual deductions or lower income due to life circumstances

Working with a fiduciary advisor can help identify these windows and model the long-term tax impact of conversion decisions.

Multi-Year Conversion Planning

Rather than converting large amounts in a single year, spreading conversions across multiple years can optimize tax efficiency. This approach fills lower tax brackets annually without pushing into higher marginal rates.

Fidelity’s analysis of tax-savvy withdrawals emphasizes the importance of projecting multi-year tax scenarios. Converting $50,000 annually over five years at the 22% rate may result in significantly lower total taxes than converting $250,000 at once and triggering the 32% bracket.

Managing Required Minimum Distributions

Once you reach age 73, RMDs from traditional retirement accounts become mandatory. Failure to take RMDs results in a steep 25% penalty (reduced to 10% if corrected within two years), making compliance essential.

RMD Calculation and Timing

RMDs are calculated by dividing the prior year-end account balance by an IRS life expectancy factor. The first RMD must be taken by April 1 of the year following the year you turn 73, with subsequent distributions required by December 31 annually.

Strategic considerations include:

- Delaying the first RMD to April 1 means taking two distributions in one tax year

- Aggregating RMDs from multiple IRAs allows withdrawal from selected accounts

- Satisfying RMDs through qualified charitable distributions (QCDs) reduces taxable income

- Planning for RMD increases as life expectancy factors decrease with age

Qualified Charitable Distributions

For charitably inclined retirees age 70½ or older, QCDs offer exceptional tax efficiency. These direct transfers from IRAs to qualified charities (up to $105,000 annually in 2026) satisfy RMD requirements without increasing adjusted gross income.

This strategy provides multiple benefits beyond standard charitable deductions because QCDs:

- Reduce MAGI for IRMAA and other income-based calculations

- Don't require itemizing deductions to receive tax benefits

- Lower future RMDs by reducing IRA balances

- Avoid state income taxes in most jurisdictions

Coordinating Social Security with Withdrawal Strategies

Social Security claiming decisions significantly impact tax efficient retirement withdrawal strategies. The timing of benefits affects not only the benefit amount but also the taxation of both Social Security and other retirement income.

Provisional Income and Social Security Taxation

Social Security benefits become taxable when provisional income exceeds certain thresholds ($32,000 for married filing jointly, $25,000 for single filers). Provisional income includes adjusted gross income, tax-exempt interest, and one-half of Social Security benefits.

Understanding these thresholds helps coordinate withdrawals strategically. For instance, taking larger traditional IRA distributions before claiming Social Security can reduce future RMDs without triggering Social Security taxation during those years.

Delayed Claiming and Withdrawal Sequencing

Delaying Social Security beyond full retirement age increases benefits by approximately 8% annually until age 70. This delay creates a withdrawal opportunity where you can:

- Draw down taxable and tax-deferred accounts during the delay period

- Fill lower tax brackets with Roth conversions

- Reduce future RMDs that would coincide with Social Security benefits

- Maximize the inflation-adjusted guaranteed income source

Principal’s guide on tax-savvy withdrawals highlights how coordinating these decisions can optimize both benefit amounts and lifetime tax efficiency.

Location Optimization and Asset Placement

Beyond withdrawal sequencing, the types of investments held in different account types affect tax efficiency. Asset location strategies place investments in accounts that minimize tax drag on returns.

Tax-Efficient Asset Location Principles

Different investments generate different types of taxable income. Bonds produce ordinary income, while stocks may generate qualified dividends and long-term capital gains. Placing tax-inefficient investments in tax-advantaged accounts and tax-efficient investments in taxable accounts can reduce overall tax burden.

Optimal placement guidelines:

- Tax-deferred accounts: Bonds, REITs, actively managed funds generating short-term gains

- Roth accounts: High-growth stocks, investments with greatest appreciation potential

- Taxable accounts: Tax-managed funds, municipal bonds, buy-and-hold stock positions

This approach requires periodic rebalancing consideration, as tax-loss harvesting in taxable accounts and strategic distributions from retirement accounts must work together within your overall retirement planning strategy.

Municipal Bonds and Tax-Exempt Income

Municipal bonds offer tax-exempt interest at the federal level, and often at state levels for in-state bonds. However, their optimal placement depends on individual circumstances.

For retirees in high tax brackets with substantial taxable income, municipal bonds in taxable accounts may offer superior after-tax returns. Conversely, those in lower brackets might achieve better results with taxable bonds in retirement accounts and tax-efficient equities in taxable accounts.

Health Savings Accounts as Retirement Tools

Health Savings Accounts (HSAs) represent a highly tax-efficient retirement vehicle often overlooked in withdrawal planning. These accounts offer triple tax advantages: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

HSA Advantages in Retirement

After age 65, HSAs become even more flexible. While withdrawals for non-medical expenses incur ordinary income tax (similar to traditional IRAs), there's no penalty. This flexibility allows HSAs to function as supplemental retirement accounts while maintaining their primary benefit for healthcare costs.

Strategic HSA approaches include:

- Maximizing contributions during working years when eligible

- Preserving HSA assets by paying medical expenses from other sources

- Allowing investments to grow tax-free throughout retirement

- Using HSA funds for Medicare premiums, long-term care insurance, and qualified medical expenses

- Keeping detailed records of unreimbursed medical expenses for later tax-free withdrawals

Healthcare represents one of the largest expense categories in retirement. Research on retirement planning consistently shows that medical costs can significantly impact financial security, making HSA preservation a valuable component of tax efficient retirement withdrawal strategies.

Estate Planning Considerations in Withdrawal Strategy

Withdrawal decisions affect not only lifetime tax efficiency but also estate planning outcomes and legacy goals. Different account types receive different treatment for beneficiaries, influencing optimal withdrawal sequencing.

Step-Up in Basis Benefits

Taxable accounts receive a step-up in cost basis at death, eliminating built-in capital gains for heirs. This characteristic makes taxable accounts valuable estate planning tools, particularly when legacy goals are important.

Conversely, traditional retirement accounts transfer to beneficiaries as taxable income, with most non-spouse beneficiaries required to deplete inherited IRAs within 10 years under current rules. This creates substantial tax burdens for heirs receiving large traditional IRAs.

Roth Accounts and Legacy Planning

Roth IRAs pass to beneficiaries tax-free and don't require RMDs during the owner's lifetime, making them exceptional legacy assets. Heirs inherit the same tax-free status, though they face the 10-year distribution requirement.

For retirees with sufficient income from other sources, preserving Roth assets for heirs while spending down traditional IRAs can optimize both lifetime and multigenerational tax efficiency. This approach requires coordination with comprehensive estate planning to align withdrawal strategies with overall legacy objectives.

Tax-Loss Harvesting and Withdrawal Coordination

Within taxable accounts, tax-loss harvesting provides ongoing opportunities to reduce tax liability during retirement. This strategy involves selling investments at a loss to offset capital gains and up to $3,000 of ordinary income annually.

Implementing Tax-Loss Harvesting in Retirement

During retirement, tax-loss harvesting coordinates with withdrawal strategies by:

- Offsetting gains from required rebalancing activities

- Creating opportunities to realize gains at 0% long-term capital gains rate

- Generating losses that carry forward to offset future gains

- Maintaining desired asset allocation while improving tax efficiency

Harvested losses can offset gains from any source, including mutual fund distributions, making this strategy particularly valuable for retirees with significant taxable account holdings.

Avoiding Wash Sale Rules

When harvesting losses, awareness of wash sale rules is essential. Purchasing substantially identical securities within 30 days before or after a sale disallows the loss deduction. Working with experienced financial advisors helps navigate these rules while maintaining appropriate portfolio positioning.

State Tax Considerations

While federal tax planning receives primary attention, state income tax differences can significantly impact optimal withdrawal strategies. Some states don't tax retirement income, while others offer specific exemptions or preferential treatment for certain income types.

State-Specific Retirement Tax Treatment

State tax treatment varies considerably across the country. Some states exempt Social Security benefits, pension income, or retirement account distributions up to certain amounts. Others tax all income sources equally.

For retirees with flexibility in establishing residency, state tax differences might influence location decisions. Even for those staying in current locations, understanding state-specific rules optimizes withdrawal sequencing.

Common state tax variations include:

- Social Security benefit exemptions (many states)

- Pension income exclusions or credits

- Differential treatment of in-state versus out-of-state pensions

- IRA and 401(k) distribution exemptions up to specific thresholds

- No state income tax (nine states as of 2026)

Dynamic Withdrawal Strategies and Periodic Review

Tax efficient retirement withdrawal strategies require regular review and adjustment. Tax laws change, personal circumstances evolve, and market performance affects account balances and distribution needs.

Annual Strategy Review Components

Effective withdrawal planning includes reviewing several factors annually:

- Tax law changes affecting rates, thresholds, or account rules

- Portfolio performance and rebalancing needs

- Income projections for current and future years

- Life changes affecting expenses, health, or family situation

- RMD calculations and Roth conversion opportunities

Avoiding common retirement tax traps requires proactive planning rather than reactive decision-making. Annual reviews allow adjustments before situations create unavoidable tax consequences.

Working with Financial Professionals

The complexity of coordinating multiple account types, tax rules, RMD requirements, Social Security claiming, and estate planning objectives often warrants professional guidance. Fiduciary advisors provide objective advice focused on client interests rather than product sales.

Professional support becomes particularly valuable when:

- Managing multiple income sources with varying tax treatments

- Planning complex Roth conversion strategies

- Coordinating withdrawals with estate planning goals

- Navigating state tax implications of relocation or multiple residences

- Implementing sophisticated strategies like QCDs or tax-loss harvesting

Inflation and Purchasing Power Protection

Beyond tax efficiency, withdrawal strategies must maintain purchasing power throughout retirement. Inflation erodes fixed income streams, making growth-oriented investments essential even during distribution years.

Balancing Tax Efficiency with Growth Needs

While tax minimization is important, over-emphasizing current tax reduction can compromise long-term financial security. Maintaining appropriate equity exposure, even when it generates taxable gains, often proves necessary for portfolio longevity.

This balance requires considering:

- Inflation-adjusted spending needs over 20-30+ year retirements

- Sequence of returns risk in early retirement years

- Portfolio allocation appropriate for distribution phase

- Withdrawal rate sustainability based on portfolio size and market conditions

Research on retirement withdrawal models examines sustainable withdrawal rates, though individual circumstances and flexibility significantly impact appropriate strategies.

Implementing tax efficient retirement withdrawal strategies requires understanding multiple account types, tax rules, and planning techniques while coordinating these elements with your unique financial situation and goals. These strategies work together to minimize lifetime tax obligations, extend portfolio longevity, and preserve wealth for legacy objectives. Brookwood Investment Group LLC specializes in creating personalized withdrawal strategies that align with your retirement vision, providing ongoing guidance to adapt as circumstances and tax laws evolve.