Understanding the rules and requirements surrounding a t rowe price 401k withdrawal can significantly impact your retirement income strategy and long-term financial health. Whether you're approaching retirement age, experiencing a financial hardship, or contemplating an early distribution, navigating the withdrawal process requires careful consideration of tax implications, penalty structures, and timing strategies. This comprehensive guide explores the essential aspects of withdrawing funds from your T. Rowe Price 401k account, helping you make informed decisions aligned with your financial objectives.

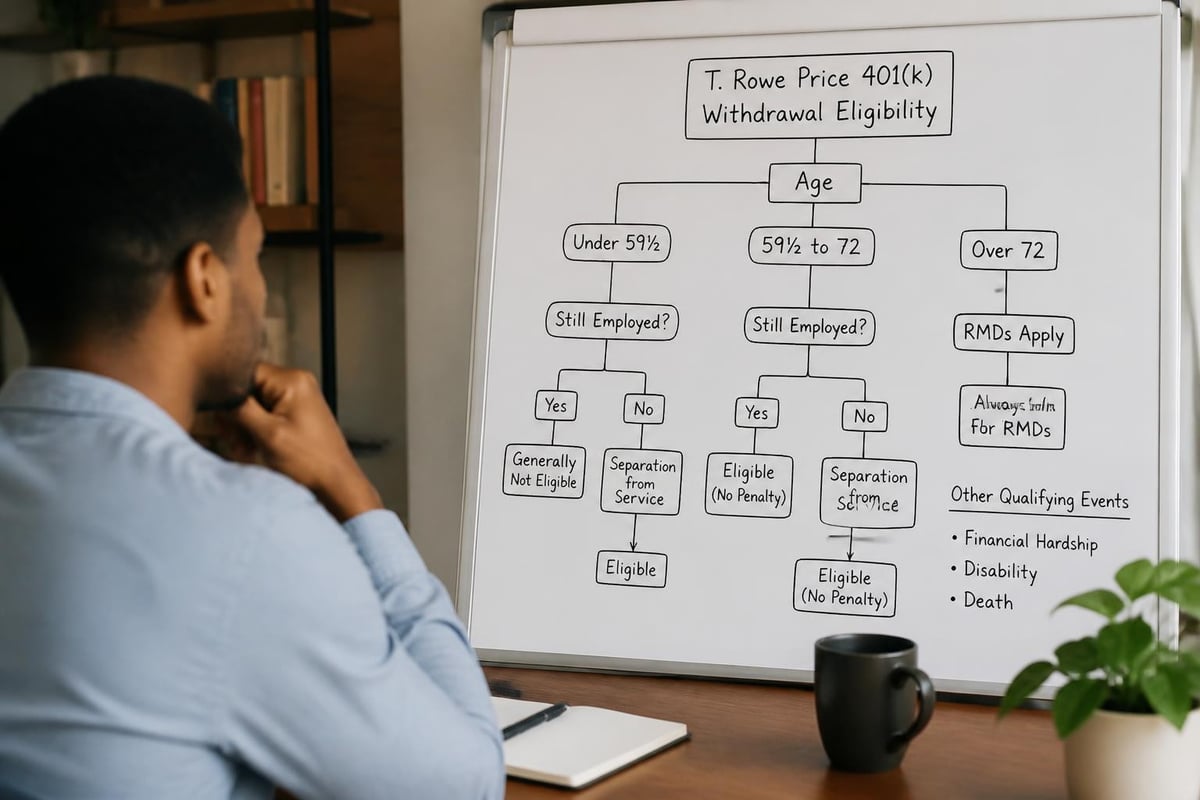

Understanding T Rowe Price 401k Withdrawal Eligibility

Accessing funds from your T. Rowe Price 401k account depends on several qualifying factors that determine both your eligibility and the potential tax consequences. The Internal Revenue Service establishes specific circumstances under which participants may withdraw funds from their retirement accounts.

Age-Based Withdrawal Rules

The most straightforward path to accessing your 401k funds involves reaching certain age milestones. At age 59½, you gain the ability to take distributions from your account without incurring the standard 10% early withdrawal penalty, though income taxes still apply to traditional 401k withdrawals.

Key age milestones include:

- Age 55: Qualify for penalty-free withdrawals under the Rule of 55 if you separate from your employer

- Age 59½: Standard penalty-free withdrawal age regardless of employment status

- Age 73: Required Minimum Distributions (RMDs) must begin for traditional 401k accounts

- Age 75: RMD rules may change based on legislative updates

The Rule of 55 provides specific advantages for individuals who leave their employer during or after the year they turn 55, allowing earlier access to retirement funds without penalties. Understanding key milestone ages in retirement helps you plan withdrawal timing strategically.

Employment Status Requirements

Your current employment relationship with the company sponsoring your T. Rowe Price 401k plan affects withdrawal options significantly. Active employees generally face more restrictions on accessing their funds compared to separated employees.

While employed, you may only access funds through hardship withdrawals or loans (if your plan permits). After termination, separation, or retirement, you gain broader distribution options including lump-sum withdrawals, systematic distributions, or rollover opportunities.

Types of T Rowe Price 401k Withdrawal Options

T. Rowe Price offers several distribution methods to accommodate different financial needs and retirement strategies. Each withdrawal type carries distinct tax treatment and procedural requirements.

Standard Distributions

Standard distributions represent the most common withdrawal method for separated or retired participants. You can request a full account liquidation or partial withdrawals based on your cash flow requirements.

| Distribution Type | Timing | Tax Treatment | Best For |

|---|---|---|---|

| Lump Sum | One-time payment | Fully taxable in year received | Immediate large expenses |

| Systematic Withdrawals | Regular intervals | Taxed as received | Ongoing income needs |

| Partial Withdrawals | As needed | Taxed per withdrawal | Flexible income planning |

| Required Minimum Distributions | Annual after age 73 | Taxed as ordinary income | Mandatory compliance |

Hardship Withdrawals

Hardship withdrawals allow access to funds while still employed, but only under specific IRS-approved circumstances. T. Rowe Price requires documentation proving immediate and heavy financial need.

Qualifying hardship reasons include:

- Medical expenses exceeding 7.5% of adjusted gross income

- Costs directly related to purchase of primary residence

- Tuition and educational fees for the next 12 months

- Payments to prevent eviction or foreclosure

- Funeral expenses for family members

- Certain expenses for repair of primary residence damage

The penalties on early withdrawals may apply even for hardship situations if you're under age 59½, making this option costly from a tax perspective.

Loans as an Alternative to Withdrawal

Before pursuing a t rowe price 401k withdrawal, consider whether your plan permits loans. Borrowing from your 401k allows temporary access to funds without triggering taxes or penalties, provided you repay according to plan terms.

Loan limits typically cap at 50% of your vested balance or $50,000, whichever is less. Repayment periods generally extend five years, except for loans used to purchase a primary residence.

Tax Implications and Penalty Structures

Understanding the tax consequences of your t rowe price 401k withdrawal helps you estimate the actual proceeds you'll receive and plan for potential tax liabilities.

Federal Income Tax Withholding

T. Rowe Price automatically withholds 20% for federal income taxes on most distributions, though your actual tax liability may differ based on your total income and tax bracket. You'll receive a 1099-R form reporting the distribution, which you must include when filing your tax return.

The withdrawn amount counts as ordinary income in the year you receive it, potentially pushing you into a higher tax bracket. Strategic timing of withdrawals across multiple tax years may reduce overall tax burden.

Early Withdrawal Penalty Exceptions

While the 10% early withdrawal penalty applies to most distributions taken before age 59½, several exceptions exist that may apply to your situation.

Penalty-free early withdrawal exceptions:

- Separation from service at age 55 or older

- Total and permanent disability

- Substantially equal periodic payments (SEPP/72(t) distributions)

- Qualified Domestic Relations Order (QDRO) for divorce settlements

- IRS levy on the 401k plan

- Medical expenses exceeding 7.5% of AGI

- Death of the participant

For a comprehensive overview of 401k withdrawal rules and penalties, consider consulting qualified financial professionals who understand your complete financial picture.

The T Rowe Price 401k Withdrawal Process

Initiating a withdrawal from your T. Rowe Price 401k account involves several procedural steps designed to verify your identity, confirm eligibility, and ensure proper tax reporting.

Step-by-Step Withdrawal Procedure

- Access your T. Rowe Price account through their website or contact their retirement services department

- Verify your eligibility for the type of distribution you're requesting

- Review tax withholding options and adjust if necessary

- Select your distribution method (check, direct deposit, or rollover)

- Complete required documentation including distribution request forms

- Submit supporting documentation for hardship withdrawals if applicable

- Confirm processing timeline which typically ranges from 5-10 business days

For those considering moving funds to another retirement account, understanding how to complete the rollover distribution form ensures accurate processing and avoids unintended tax consequences.

Required Documentation

T. Rowe Price requires specific documentation depending on your withdrawal type. Standard distributions typically need only basic identification and beneficiary confirmation, while hardship withdrawals demand proof of financial need.

Gather these materials before initiating your request:

- Government-issued photo identification

- Spouse consent form (if married and required by plan)

- Hardship documentation (bills, contracts, or statements)

- Beneficiary designation form (if outdated)

- Banking information for direct deposit

Processing Timelines and Payment Methods

Most t rowe price 401k withdrawal requests process within 7-10 business days after T. Rowe Price receives complete documentation. Complex situations involving outstanding loans or pending transactions may extend this timeline.

Available payment methods include:

- Direct deposit to your bank account (fastest option)

- Paper check mailed to address on file

- Wire transfer for urgent situations (may incur fees)

- Direct rollover to another qualified retirement plan or IRA

Strategic Considerations for Retirement Income Planning

Withdrawing funds from your T. Rowe Price 401k represents just one component of comprehensive retirement income strategy. Thoughtful planning considers tax efficiency, longevity risk, and income sequencing across multiple account types.

Withdrawal Sequencing Strategies

Financial professionals often recommend specific ordering when drawing from multiple retirement accounts to optimize tax efficiency and preserve assets. This approach, called withdrawal sequencing, considers the tax characteristics of different account types.

| Account Type | Tax Treatment | Typical Priority | Strategic Consideration |

|---|---|---|---|

| Taxable Brokerage | Capital gains rates | First | Lowest tax rates, most flexibility |

| Tax-Deferred 401k/IRA | Ordinary income | Second | Required distributions after age 73 |

| Roth IRA/401k | Tax-free | Last | Maximum growth potential, no RMDs |

| Health Savings Account | Tax-free for medical | Variable | Medical expense coverage |

Working with fiduciary advisors who prioritize your interests helps develop personalized withdrawal strategies aligned with your specific circumstances.

Coordinating With Other Income Sources

Your t rowe price 401k withdrawal strategy should coordinate with Social Security benefits, pension income, investment accounts, and other revenue streams. Optimizing the timing and amount of each income source can significantly impact lifetime tax liability.

Consider delaying Social Security benefits while using 401k distributions to bridge income gaps in early retirement. This strategy allows Social Security benefits to grow 8% annually until age 70 while potentially keeping you in lower tax brackets.

Required Minimum Distribution Planning

Once you reach age 73, federal law mandates annual withdrawals from traditional 401k accounts based on IRS life expectancy tables. Failing to take RMDs results in a substantial penalty of 25% of the amount you should have withdrawn (reduced to 10% if corrected promptly).

Calculate your RMD by dividing your account balance as of December 31 of the prior year by the applicable distribution period from IRS tables. T. Rowe Price typically provides RMD calculations and can automate distributions to ensure compliance.

Alternatives to 401k Withdrawals

Before committing to a t rowe price 401k withdrawal, explore alternative strategies that may better serve your financial objectives while preserving retirement assets.

Rollover Options

Rolling your T. Rowe Price 401k into an Individual Retirement Account (IRA) provides continued tax-deferred growth with potentially broader investment options and more flexible withdrawal rules. Direct rollovers avoid withholding taxes and eliminate rollover-related penalties.

Rollover advantages include:

- Expanded investment choices beyond plan offerings

- Potential for lower fees with competitive IRA providers

- Simplified account management by consolidating multiple retirement accounts

- Continued tax-deferred growth without forced distributions

For detailed guidance on accessing 401k funds through various methods, consider both immediate withdrawal needs and long-term retirement security.

Roth Conversion Opportunities

Converting traditional 401k funds to Roth accounts triggers immediate tax liability but provides tax-free growth and withdrawals in retirement. This strategy works particularly well during lower-income years when your tax bracket is temporarily reduced.

Strategic Roth conversions during early retirement (before Social Security and RMDs begin) can reduce future required distributions and create tax-free income for later years. Consult with professionals who understand estate planning advantages to evaluate whether this approach aligns with your legacy goals.

Maintaining the Account

Leaving funds in your T. Rowe Price 401k after separation may provide advantages in certain situations. Some 401k plans offer institutional pricing on investments not available to retail investors, and 401k accounts receive stronger creditor protections than IRAs under federal law.

Additionally, participants who separate from service at age 55 or later can access 401k funds penalty-free, whereas IRA withdrawals require waiting until age 59½. This five-year difference can prove valuable for early retirees.

Common Mistakes to Avoid

Many individuals encounter costly errors when managing their t rowe price 401k withdrawal. Understanding these common pitfalls helps you protect your retirement assets and minimize unnecessary expenses.

Underestimating Tax Impact

One of the most frequent mistakes involves failing to account for the full tax burden of 401k withdrawals. Remember that the 20% automatic withholding may not cover your entire tax liability, especially for large distributions.

If you withdraw all of your 401k funds, the entire amount becomes taxable income in that year, potentially pushing you into the highest tax brackets and triggering additional taxes on Social Security benefits and Medicare premiums.

Violating the 60-Day Rollover Rule

When taking a distribution with the intent to roll it over to another retirement account, you must complete the transaction within 60 days to avoid taxes and penalties. Missing this deadline by even one day converts the distribution into a taxable withdrawal.

Direct rollovers from T. Rowe Price to your new custodian eliminate this risk entirely by moving funds directly between institutions without the money passing through your hands.

Ignoring State Tax Obligations

While federal tax withholding is automatic, state income tax requirements vary significantly. Some states impose additional withholding requirements or penalties for early distributions, while others provide preferential treatment for retirement income.

Research your state's specific treatment of 401k distributions and adjust your withholding accordingly to avoid unexpected tax bills or overpayment of taxes throughout the year.

Failing to Update Beneficiaries

Before requesting a t rowe price 401k withdrawal, verify that your beneficiary designations reflect your current wishes. Life changes including marriage, divorce, births, and deaths may necessitate updates to ensure assets transfer according to your intentions.

Beneficiary designations supersede will instructions for retirement accounts, making these forms critical estate planning documents that deserve regular review.

Coordinating Withdrawals With Comprehensive Financial Planning

Your retirement withdrawal strategy extends beyond simple distribution mechanics to encompass tax planning, investment management, and estate considerations. Developing personalized strategies requires understanding how 401k withdrawals interact with your complete financial picture.

Tax Strategy Integration

Effective tax strategies consider not only current-year tax liability but also multi-year planning that optimizes lifetime tax efficiency. This might include strategically timing large withdrawals during low-income years or spreading distributions across multiple years to avoid bracket creep.

Professional guidance helps identify opportunities for tax-loss harvesting in taxable accounts, charitable giving strategies that offset distribution income, and timing considerations that minimize taxation on Social Security benefits.

Investment Management During Distribution Phase

Transitioning from accumulation to distribution requires different investment approaches that balance growth objectives with income needs and risk management. Understanding when you can access retirement funds helps structure portfolios appropriately for your timeline.

Asset allocation shifts toward more conservative positions as you draw down retirement accounts, but completely abandoning growth investments may jeopardize long-term purchasing power. Regular portfolio rebalancing ensures withdrawals come from appropriate asset classes while maintaining target allocations.

Healthcare and Medicare Considerations

Large 401k withdrawals can increase your Modified Adjusted Gross Income (MAGI), potentially triggering higher Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amounts (IRMAA). These surcharges apply based on income from two years prior, requiring forward-looking planning.

Consider spreading large distributions across multiple years or timing them before Medicare enrollment to minimize premium impacts. For detailed guidance on withdrawing money from T Rowe Price 401k accounts, evaluate both immediate needs and long-term healthcare cost implications.

Working With Financial Professionals

Navigating the complexities of retirement account distributions benefits significantly from professional guidance tailored to your unique circumstances. Qualified advisors provide personalized analysis that considers your complete financial situation rather than isolated transactions.

The Fiduciary Advantage

Working with fiduciary advisors ensures that recommendations prioritize your interests above all other considerations. This legal and ethical standard creates alignment between your goals and the guidance you receive.

Comprehensive retirement planning services integrate 401k withdrawal strategies with Social Security optimization, tax planning, estate considerations, and investment management to create cohesive strategies supporting your retirement objectives.

Virtual Advisory Benefits

Modern technology enables effective financial planning without geographic constraints. Virtual-first advisory relationships provide convenient access to professional guidance through video conferences, secure document sharing, and digital collaboration tools.

This approach offers flexibility for busy professionals while maintaining the personalized attention necessary for complex financial decisions like timing and structuring retirement account withdrawals.

Ongoing Plan Adjustments

Retirement planning requires regular reassessment as circumstances change, markets fluctuate, and tax laws evolve. Establishing relationships with advisors who provide continuous monitoring helps ensure your withdrawal strategy remains appropriate throughout retirement.

Annual reviews examine whether distribution amounts still meet your needs, verify RMD compliance, assess tax efficiency, and adjust strategies based on legislative changes or personal circumstances.

Understanding t rowe price 401k withdrawal rules, tax implications, and strategic timing helps you make informed decisions that support your retirement income needs while minimizing unnecessary costs. Whether you're approaching retirement, experiencing unexpected financial needs, or planning long-term distribution strategies, careful consideration of all factors ensures optimal outcomes. Brookwood Investment Group provides personalized, fiduciary guidance to help you navigate these complex decisions, integrating 401k withdrawal strategies with comprehensive retirement planning, tax optimization, and investment management tailored to your unique goals and circumstances.