Finding the right financial professional to manage your wealth and retirement planning requires more than just a recommendation from a friend or an online search. Before entrusting anyone with your financial future, conducting a thorough registered investment advisor lookup is essential to verify credentials, check disciplinary history, and confirm regulatory compliance. This verification process protects you from potential fraud, ensures your advisor operates under fiduciary standards, and provides transparency into their professional background. Understanding how to effectively research investment advisors empowers you to make informed decisions about who guides your financial journey.

Understanding the Registered Investment Advisor Landscape

Registered Investment Advisors (RIAs) operate under a fiduciary standard, meaning they are legally obligated to act in your best interests. This distinguishes them from broker-dealers who may operate under a less stringent suitability standard. When you perform a registered investment advisor lookup, you're accessing public records that reveal critical information about the advisor's qualifications, business practices, and regulatory compliance.

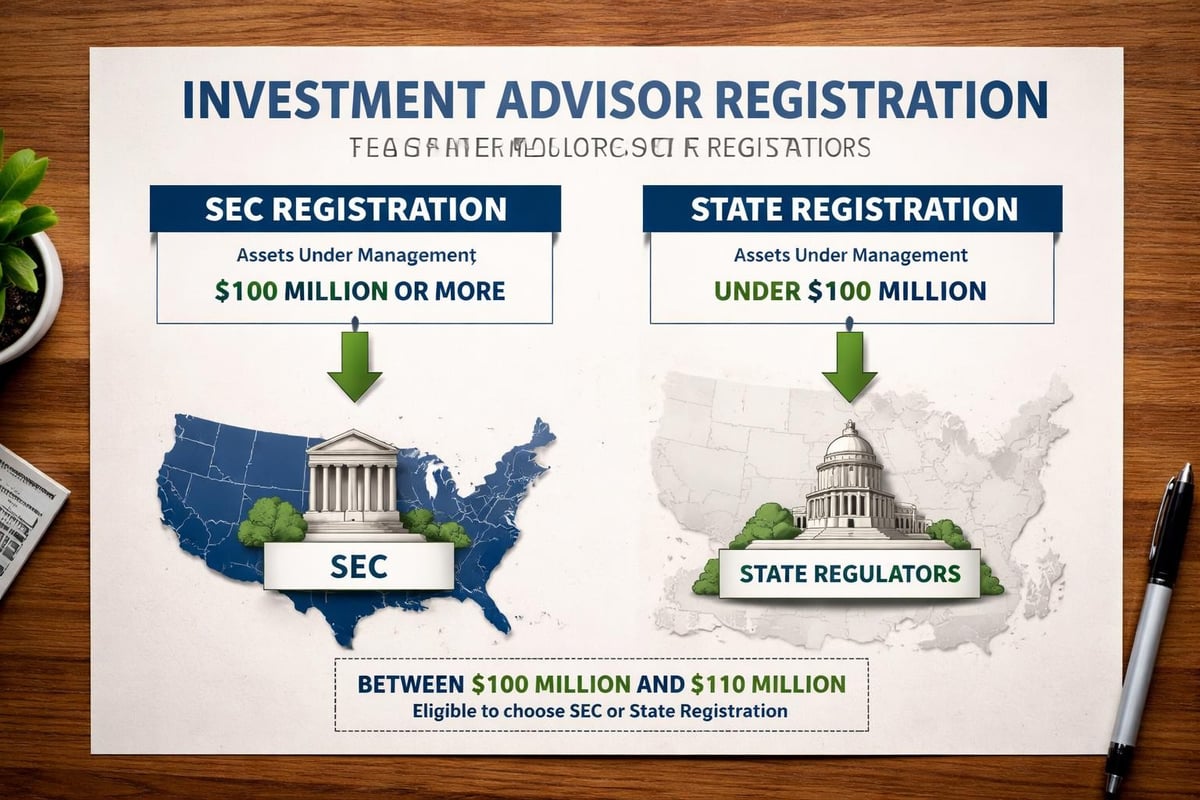

The regulatory framework for RIAs involves both federal and state oversight. Advisors managing $110 million or more in assets typically register with the Securities and Exchange Commission (SEC), while those managing less register with their state securities regulator. This dual-level system ensures that regardless of firm size, advisors maintain proper registration and transparency.

Key distinctions between RIAs and other financial professionals include:

- Fiduciary duty to clients at all times

- Comprehensive disclosure requirements through Form ADV

- Fee-based compensation structures rather than commission-driven models

- Regular regulatory examinations and compliance obligations

Understanding these differences helps you appreciate why a registered investment advisor lookup matters. When you work with Brookwood Investment Group, you're partnering with a fiduciary firm that prioritizes transparency and your best interests in every recommendation.

Where to Conduct Your Registered Investment Advisor Lookup

Several official databases provide free access to advisor registration information. The most comprehensive resource is the SEC's Investment Adviser Public Disclosure (IAPD) website, which allows you to search for both firms and individual advisors. This database connects to the Investment Adviser Registration Depository (IARD), the electronic filing system that maintains current registration data.

FINRA’s BrokerCheck serves as another valuable tool, particularly for advisors who maintain both RIA registration and broker-dealer licenses. This dual registration is common in the industry, and BrokerCheck provides employment history, professional qualifications, and disclosure events spanning multiple years.

Primary Lookup Resources

| Database | Best For | Information Available |

|---|---|---|

| SEC IAPD | RIA firms and individuals | Form ADV, disciplinary history, assets under management |

| FINRA BrokerCheck | Broker-dealers and dual-registered advisors | Employment history, licenses, disclosures |

| State Regulators | Smaller RIAs and state-specific issues | Local registration, complaints, enforcement actions |

State securities regulators maintain their own databases for advisors registered at the state level. For example, the California Department of Financial Protection and Innovation offers specific guidance for verifying advisors operating in California. Many states provide similar resources tailored to their jurisdiction.

When performing your lookup, start with the firm name and then verify individual advisors associated with that firm. This two-step approach ensures comprehensive due diligence. Cross-referencing multiple databases strengthens your research, as each may contain unique information or different update schedules.

Decoding Form ADV: Your Most Valuable Resource

Form ADV represents the cornerstone document in any registered investment advisor lookup. This disclosure form contains two main parts that reveal extensive information about an advisor's business practices, conflicts of interest, and disciplinary history. Part 1 provides detailed business information, while Part 2 offers a narrative brochure describing services, fees, and potential conflicts.

Part 2A includes critical sections describing the advisor's investment strategies, risk factors, and fee schedules. This narrative format makes it accessible to investors without specialized financial knowledge. Part 2B provides biographical information about individual advisors, including their educational background, professional designations, and any disciplinary events.

Key sections to review in Form ADV:

- Item 4: Advisory business description and client types

- Item 5: Fee structures and compensation arrangements

- Item 9: Disciplinary information about the firm

- Item 10: Other financial industry activities and affiliations

- Item 11: Code of ethics and personal trading policies

Pay particular attention to how the advisor charges fees. Understand whether fees are asset-based, hourly, flat-rate, or commission-based. Fee transparency directly impacts your returns over time, and understanding the structure helps you compare different advisors effectively. Fiduciary planning approaches typically emphasize transparent, conflict-free fee arrangements.

What Red Flags to Watch For During Your Search

During your registered investment advisor lookup, certain warning signs should prompt additional scrutiny or reconsideration. Disciplinary history represents the most obvious concern, but the context matters significantly. A single minor disclosure from many years ago differs substantially from recent or repeated violations.

Customer complaints require careful evaluation. Review the nature of complaints, how they were resolved, and whether patterns emerge across multiple clients. Some complaints may reflect misunderstandings rather than professional misconduct, while others indicate serious problems with the advisor's practices.

Common Red Flags in Advisor Backgrounds

- Multiple employment changes within short timeframes

- Gaps in employment history without explanation

- Bankruptcy or financial difficulties

- Criminal convictions or pending legal matters

- Regulatory suspensions or sanctions

- Customer complaints involving fraud or misappropriation

Unregistered advisors represent the most serious red flag. Anyone providing investment advice for compensation must maintain appropriate registration unless they qualify for specific exemptions. The SEC’s investor education resources emphasize verifying registration before engaging any financial professional.

Verify professional designations claimed by advisors. Some credentials require rigorous education and testing, while others are essentially purchased titles with minimal requirements. The registered investment advisor lookup process should include confirming that claimed designations are legitimate and current.

Evaluating Advisor Qualifications Beyond Registration

While a registered investment advisor lookup confirms regulatory compliance, assessing qualifications requires examining education, experience, and specializations. Professional certifications like CFP (Certified Financial Planner), CFA (Chartered Financial Analyst), or CPA (Certified Public Accountant) indicate specialized knowledge and ongoing education commitments.

Experience matters significantly in financial planning. Consider how long the advisor has been practicing, what market cycles they've navigated, and whether their experience aligns with your needs. An advisor specializing in retirement planning and estate planning brings different expertise than one focused primarily on young professionals.

Review the advisor's typical client profile. Advisors often specialize in serving specific demographics or wealth levels. Ensuring alignment between their typical client and your situation increases the likelihood of receiving relevant, tailored guidance. Some firms focus exclusively on high net worth financial advisors services, while others serve a broader range of clients.

Questions to ask when evaluating qualifications:

- What professional designations do you hold, and are they current?

- How many years have you been advising clients?

- What percentage of your clients have similar financial situations to mine?

- Do you have specific expertise in areas relevant to my needs?

- What continuing education do you complete annually?

The virtual-first model that some advisory firms employ doesn't diminish the importance of qualifications. Technology enables broader access to experienced advisors regardless of geographic location, expanding your options during your registered investment advisor lookup.

Understanding Fiduciary vs. Suitability Standards

The distinction between fiduciary and suitability standards fundamentally affects the advice you receive. A registered investment advisor lookup helps you identify advisors bound by the stricter fiduciary standard, which requires acting in your best interests at all times. This obligation extends beyond merely recommending suitable investments to actively avoiding conflicts of interest.

Broker-dealers operating under the suitability standard must ensure recommendations are appropriate for your situation but aren't necessarily the best option available. They may recommend products that generate higher commissions if those products still meet the suitability threshold. This difference becomes particularly important when considering fiduciary investment approaches.

| Standard | Legal Obligation | Conflict of Interest Management | Best For |

|---|---|---|---|

| Fiduciary | Act in client's best interest | Must avoid or fully disclose conflicts | Comprehensive financial planning |

| Suitability | Recommend appropriate products | Must disclose material conflicts | Transaction-based services |

Some advisors hold both RIA and broker-dealer licenses, operating as "dual-registered" professionals. In these cases, the standard applied depends on the capacity in which they're acting during each interaction. This arrangement can create confusion about which standard applies, making transparency essential.

When conducting your registered investment advisor lookup, verify whether the advisor operates exclusively as a fiduciary or switches between standards. FINRA’s investor education resources provide guidance on understanding these distinctions and asking the right questions.

State-Specific Registration Requirements and Lookups

While federal registration through the SEC covers larger advisory firms, many advisors register at the state level. Each state maintains its own securities regulator responsible for overseeing smaller RIAs and enforcing state securities laws. Your registered investment advisor lookup should include checking with your state regulator, particularly if working with a smaller local firm.

State requirements vary significantly regarding registration thresholds, filing procedures, and disclosure obligations. Some states impose additional requirements beyond federal standards, including bonding requirements, financial statement filings, or specific educational prerequisites. These variations mean a thorough lookup process includes both federal and state databases.

State resources like those provided by South Carolina and Indiana demonstrate how different jurisdictions offer investor education and verification tools. These state-specific resources often include complaint history and enforcement actions not immediately visible in federal databases.

Benefits of checking state regulatory databases:

- Access to state-specific disciplinary actions

- Information on advisors below federal registration thresholds

- State complaint histories and resolution details

- Local enforcement actions and cease-and-desist orders

For advisors operating in multiple states, registration requirements become more complex. They may need to register in each state where they have clients or qualify for exemptions based on client count or other factors. Verifying multi-state registration ensures your advisor maintains proper licensing regardless of your location.

How Often to Perform Advisor Background Checks

A registered investment advisor lookup shouldn't be a one-time event. Periodic verification ensures your advisor maintains proper registration and hasn't incurred new disciplinary actions. Regulatory status can change, and advisors may face new customer complaints or enforcement actions after you initially verified their credentials.

Annual reviews represent a reasonable frequency for most clients. This schedule aligns with typical advisory relationship reviews and provides opportunities to reassess whether your advisor still meets your needs. Set calendar reminders to conduct these checks, treating them as routine maintenance of your financial relationships.

Immediate verification becomes necessary when certain triggering events occur. If your advisor changes firms, updates their fee structure significantly, or you hear concerning news about their practice, conduct a fresh registered investment advisor lookup immediately. These transitions may affect their registration status or reveal new disclosure items.

Monitor for these specific changes during periodic checks:

- New customer complaints or arbitrations

- Regulatory sanctions or enforcement actions

- Changes in business structure or ownership

- Updates to fee schedules or service offerings

- New conflicts of interest disclosures

- Changes in professional designations or licenses

Technology makes periodic verification increasingly convenient. Many regulatory databases offer alert services that notify you of changes to an advisor's registration or disclosure information. Leveraging these tools reduces the burden of manual checking while maintaining oversight.

Integrating Lookup Results Into Your Decision Process

After completing your registered investment advisor lookup, synthesize the information into actionable insights. A clean regulatory record represents an important baseline, but it doesn't automatically mean an advisor is the right fit for your specific needs. Consider the lookup results alongside other factors like investment philosophy, communication style, and service structure.

Schedule initial consultations with advisors who pass your background check. Use these meetings to verify information discovered during your lookup and assess intangible factors like rapport and communication effectiveness. Prepare specific questions based on Form ADV disclosures, particularly regarding any conflicts of interest or disciplinary history.

Compare multiple advisors systematically. Create a standardized evaluation matrix that scores each advisor across important criteria including regulatory history, qualifications, fee structure, services offered, and personal compatibility. This structured approach prevents emotional decision-making and ensures you consider all relevant factors.

Essential topics to discuss during initial meetings:

- Detailed explanation of fee structures and total costs

- Investment philosophy and approach to risk management

- Communication frequency and reporting practices

- Team structure and continuity planning

- Specific experience relevant to your situation

- How they handle conflicts of interest

Remember that working as a financial advisor involves building long-term relationships. The registered investment advisor lookup provides crucial data, but successful partnerships also require alignment on values, communication preferences, and financial goals. Combine objective verification with subjective assessment to make well-rounded decisions.

Special Considerations for Virtual Advisory Relationships

The rise of virtual-first advisory firms expands your options beyond local advisors, but it also requires adapting your registered investment advisor lookup process. Geographic distance doesn't eliminate regulatory oversight, as advisors must still maintain proper registration in states where they have clients. Verify that virtual advisors are registered in your state of residence.

Technology platforms used by virtual advisors warrant evaluation. Assess their security protocols, data encryption practices, and business continuity plans. While these factors don't appear in traditional registered investment advisor lookup databases, they're essential for protecting your information and ensuring service continuity.

Virtual relationships may actually enhance transparency in some ways. Digital communication creates documented records of advice and recommendations, while online portals provide 24/7 access to account information and planning documents. These features can strengthen accountability and client service compared to traditional in-person models.

Consider how a virtual-first firm like those offering financial planning and investment management services maintains client relationships. Effective virtual advisors utilize video conferencing, secure messaging, and collaborative planning tools to create personal connections despite physical distance. Evaluate whether their technology and communication approach meet your preferences.

Understanding Enforcement Actions and Disciplinary History

When your registered investment advisor lookup reveals disciplinary history, understanding the severity and context becomes crucial. Not all enforcement actions carry equal weight. Minor procedural violations differ significantly from fraud or client harm. Review the specific allegations, findings, and sanctions imposed.

Regulatory bodies including the SEC, FINRA, and state securities regulators can impose various sanctions ranging from fines to permanent bars from the industry. The severity of the sanction generally reflects the seriousness of the violation. Multiple minor violations may indicate systemic compliance problems even if no single incident seems severe.

Consider how the advisor responded to disciplinary actions. Did they accept responsibility and implement corrective measures? Have they maintained a clean record since the incident? An isolated event from many years ago, followed by consistent compliance, differs from recent or ongoing problems.

Customer complaints require similar contextual analysis. The registered investment advisor lookup may show settled complaints that don't necessarily indicate wrongdoing. Some clients file complaints based on market losses during downturns, even when the advisor followed appropriate procedures. Review complaint details to assess validity and patterns.

Red flags in disciplinary history:

- Multiple complaints with similar allegations

- Findings of fraud or misappropriation

- Recent enforcement actions (within past 5 years)

- Patterns of violation despite previous sanctions

- Settlements involving significant monetary damages

Advisors should willingly discuss any disciplinary history during initial consultations. Transparency about past issues and explanations of remedial actions demonstrate integrity. Reluctance to address disclosed items or discrepancies between Form ADV and verbal explanations warrant serious concern.

Verifying Professional Designations and Credentials

Many advisors display professional designations that suggest specialized expertise. Your registered investment advisor lookup should include verifying these credentials through the organizations that grant them. Some designations require rigorous education, examination, and ongoing continuing education, while others have minimal standards.

The CFP (Certified Financial Planner) designation represents one of the most respected credentials, requiring comprehensive education, examination, experience, and ethical standards. Verify CFP credentials through the CFP Board's website. Similarly, CFA (Chartered Financial Analyst) credentials can be verified through the CFA Institute.

Be wary of obscure or unfamiliar designations. Some credentials are created primarily for marketing purposes rather than representing genuine expertise. Research any designation you don't recognize, including who grants it, what requirements exist, and whether ongoing education is mandatory.

Questions to ask about professional credentials:

- Which organization grants this designation?

- What education and examination requirements did you complete?

- How long have you held this credential?

- What continuing education maintains the designation?

- Does this credential require adherence to ethical standards?

Tax-related services require specific credentials. Advisors offering tax planning should have appropriate credentials like CPA (Certified Public Accountant) or EA (Enrolled Agent) if they provide tax preparation services. Understanding the scope of their qualifications prevents assuming expertise beyond their actual credentials. Some firms integrate financial advisor and CPA services through specialized professionals.

The Role of Third-Party Ratings and Reviews

While your registered investment advisor lookup focuses on regulatory databases, third-party ratings and client reviews provide additional perspective. However, approach these sources with appropriate skepticism, as rating methodologies vary widely and may emphasize factors irrelevant to your needs.

Some rating systems primarily measure assets under management or revenue rather than client outcomes or service quality. Others may charge advisors for inclusion or enhanced placement, creating potential conflicts. Understand the rating methodology before placing significant weight on any ranking or award.

Client reviews on independent platforms offer valuable insights into service quality, communication practices, and overall client satisfaction. Look for detailed reviews describing specific experiences rather than generic praise. Patterns across multiple reviews provide more reliable information than individual testimonials.

Consider the source and motivation behind reviews. Some platforms verify that reviewers are actual clients, while others accept anonymous submissions. Verified reviews carry more credibility. Be aware that extremely positive reviews clustered together may indicate solicited testimonials rather than organic feedback.

| Review Source | Verification Level | Reliability | Best Use |

|---|---|---|---|

| Regulatory databases | Official records | High | Credential verification |

| Client testimonials on advisor websites | Self-selected | Low | Understanding service approach |

| Independent review platforms | Varies by platform | Medium | Gauging client satisfaction |

| Professional rankings | Methodology-dependent | Medium | Identifying established firms |

Balance third-party information with your own research and direct interaction. No rating system or review collection replaces thorough due diligence through a registered investment advisor lookup and personal evaluation of fit with your needs.

Conducting a thorough registered investment advisor lookup represents a critical step in selecting a financial professional who will guide your wealth management and retirement planning. This verification process protects your interests by confirming credentials, revealing potential red flags, and ensuring regulatory compliance. Armed with knowledge of where to search, what to review, and how to interpret findings, you can confidently evaluate advisors and make informed decisions about your financial future. Brookwood Investment Group maintains full transparency as a registered fiduciary advisor, with credentials and background readily verifiable through official regulatory databases, ensuring you have complete confidence in the guidance you receive. Contact us today to begin building your personalized financial strategy with a team committed to acting in your best interests.