Finding the right personal financial advisor near me has evolved significantly in recent years, particularly with the rise of virtual-first advisory firms that combine personalized guidance with technological convenience. Whether you're planning for retirement, managing investments, or developing comprehensive wealth strategies, selecting a qualified advisor who understands your unique financial situation is a critical decision that can impact your long-term financial well-being. This guide explores the essential factors to consider when searching for a personal financial advisor, the credentials and qualifications that matter most, and how modern advisory relationships work in 2026.

Understanding What a Personal Financial Advisor Does

A personal financial advisor provides tailored guidance on various aspects of your financial life. These professionals analyze your current financial situation, help you identify goals, and develop strategies to achieve those objectives over time.

Financial advisors typically offer services in several key areas:

- Retirement planning to help you build adequate savings and create distribution strategies

- Investment management involving portfolio construction and ongoing monitoring

- Estate planning coordination to help preserve wealth for future generations

- Tax strategy development to potentially optimize your tax situation

- Risk management through insurance analysis and protection planning

The scope of services can vary significantly depending on the advisor's expertise and business model. Some advisors specialize in particular areas, while others provide comprehensive financial planning that addresses all aspects of your financial life.

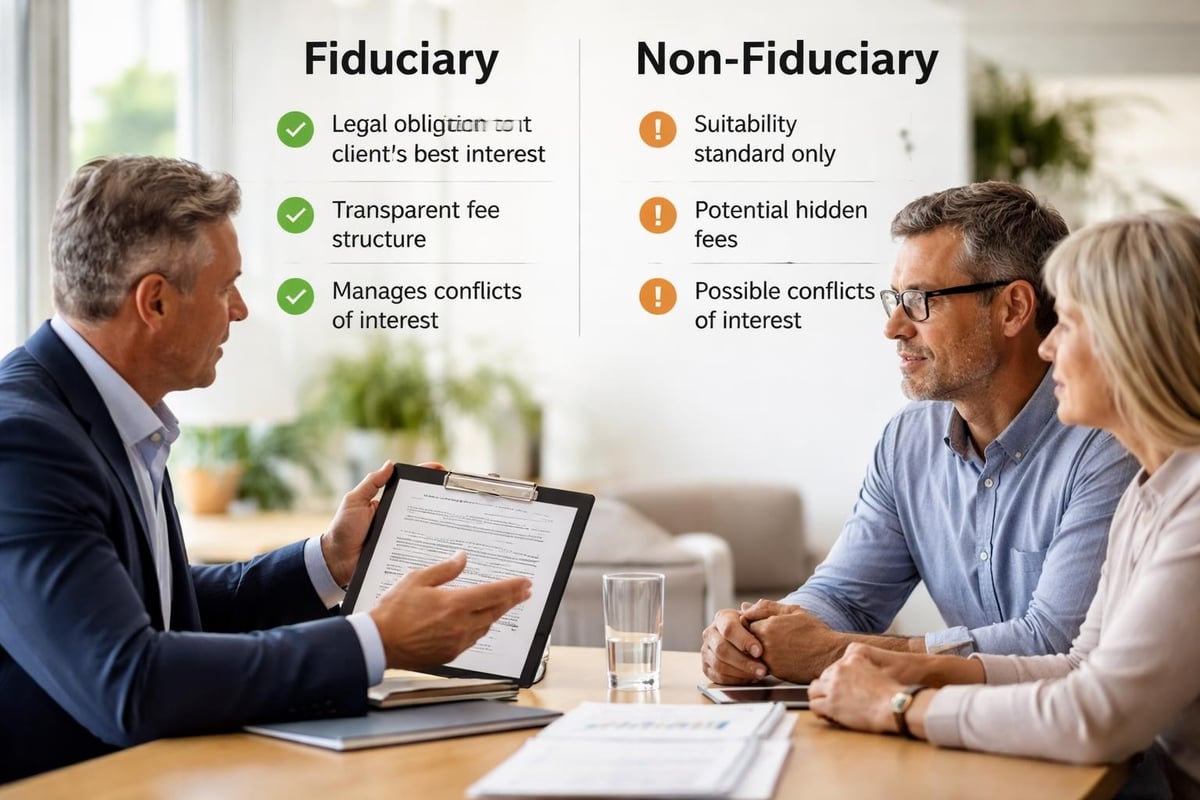

The Fiduciary Standard

When searching for a personal financial advisor near me, understanding the fiduciary standard is essential. Fiduciary advisors are legally obligated to act in your best interest at all times, placing your needs ahead of their own compensation or business interests.

This standard differs from the suitability standard, where recommendations must simply be suitable for your situation but not necessarily optimal. Understanding fee structures and fiduciary responsibilities helps ensure your advisor's recommendations align with your financial objectives rather than commission-based incentives.

Evaluating Credentials and Qualifications

Professional credentials provide valuable insight into an advisor's training, expertise, and commitment to ongoing education. Several designations carry particular significance in the financial advisory industry.

Key Professional Designations

| Designation | Full Name | Focus Area | Requirements |

|---|---|---|---|

| CFP® | Certified Financial Planner | Comprehensive planning | Education, exam, experience, ethics |

| CFA® | Chartered Financial Analyst | Investment analysis | Three rigorous exams, work experience |

| ChFC® | Chartered Financial Consultant | Financial planning | Eight college-level courses |

| CPA/PFS | Personal Financial Specialist | Tax-focused planning | CPA license plus financial planning exam |

The CFP® designation represents one of the most comprehensive certifications for personal financial advisors. Professionals holding this credential have completed extensive coursework covering retirement planning, estate planning, tax planning, and investment management. They must also maintain ongoing education requirements and adhere to strict ethical standards.

Beyond formal credentials, consider the advisor's experience working with clients in situations similar to yours. An advisor who regularly works with business owners, for instance, may bring different insights than one who primarily serves retirees.

Comparing Fee Structures and Compensation Models

How your personal financial advisor near me gets compensated directly impacts the advice you receive and your overall costs. Several common fee structures exist in the industry today.

Fee-only advisors charge directly for their services through hourly rates, flat fees, or a percentage of assets under management (AUM). This model eliminates potential conflicts of interest related to product sales or commissions.

Commission-based advisors earn compensation when you purchase financial products they recommend. While this can result in lower upfront costs, it may create incentives that don't always align with your best interests.

Fee-based advisors combine both approaches, charging fees for planning services while also earning commissions on certain products. This hybrid model requires careful scrutiny to understand all compensation sources.

Asset-based fees typically range from 0.50% to 1.50% annually, with larger portfolios often receiving lower percentage rates. For personalized guidance on fiduciary planning approaches, understanding these fee structures helps you evaluate the total cost of advisory services.

The Virtual Advisory Experience in 2026

Geographic proximity has become less relevant when searching for a personal financial advisor near me. Virtual-first advisory firms now deliver comprehensive financial guidance through secure digital platforms, video conferencing, and cloud-based document sharing.

This shift offers several advantages:

- Broader advisor selection beyond your immediate geographic area

- Flexible meeting schedules that accommodate busy lifestyles

- Digital collaboration tools for real-time plan updates and tracking

- Reduced overhead costs potentially resulting in more competitive fees

- Seamless document exchange through secure portals

Virtual advisory relationships maintain the personalized attention of traditional face-to-face meetings while adding convenience and accessibility. Many clients appreciate the ability to schedule consultations around their work and family commitments without commuting to an office.

Security measures have advanced significantly, with advisors implementing multi-factor authentication, encrypted communications, and secure file-sharing systems that often exceed the protection of paper-based processes.

Asking the Right Questions During Initial Consultations

The interview process helps you evaluate whether a potential personal financial advisor near me fits your needs and preferences. Conducting thorough interviews allows you to assess both technical competence and personal compatibility.

Essential Questions to Ask

-

What are your qualifications and credentials? Request specific information about education, designations, and years of experience.

-

Are you a fiduciary for all services you provide? Confirm the advisor will always act in your best interest.

-

How do you charge for your services? Get detailed explanations of all fees, including any third-party compensation.

-

What services do you offer? Understand whether they provide comprehensive planning or focus on specific areas.

-

Who will work with me directly? Clarify whether you'll interact with the lead advisor or support staff.

-

How often will we communicate? Establish expectations for review meetings and ongoing contact.

-

What is your investment philosophy? Ensure their approach aligns with your risk tolerance and goals.

-

Can you provide references? Speaking with current clients offers valuable perspective.

Take notes during these conversations and compare responses across multiple advisors. The right fit involves both professional qualifications and personal rapport that makes you comfortable discussing sensitive financial matters.

Verifying Background and Regulatory History

Due diligence extends beyond credentials to include regulatory compliance and disciplinary history. Several resources help you research potential advisors thoroughly.

BrokerCheck from FINRA provides detailed information about registered securities professionals, including employment history, qualifications, and any regulatory actions or customer complaints.

Investment Adviser Public Disclosure (IAPD) offers similar information for registered investment advisors, including their Form ADV, which discloses business practices, fees, and potential conflicts of interest.

State securities regulators also maintain records and can provide additional information about advisors operating in your state. Conducting background checks helps identify any red flags before entering an advisory relationship.

Review the Form ADV Part 2 carefully, as it reveals important details about the advisor's services, fee schedules, and business practices. This document must be provided to prospective clients and updated annually.

Specialized Advisory Services for Unique Situations

Your specific circumstances may benefit from specialized expertise beyond general financial planning. Several niches exist within the advisory industry.

Common Specializations

- Business owner financial planning addressing succession, exit strategies, and executive compensation

- High net worth advisory focusing on complex estate planning and tax strategies

- Retirement income planning specializing in distribution strategies and longevity risk

- Expatriate financial guidance navigating cross-border taxation and investment issues

- Faith-based financial planning incorporating values into financial decisions

For individuals seeking advisors who share specific values, designations like the Certified Kingdom Advisor (CKA) indicate advisors who integrate faith principles into financial guidance.

Specialized knowledge becomes particularly valuable when dealing with complex situations like business valuations, multi-generational wealth transfer, or coordinating financial strategies across international borders. Consider whether your situation requires niche expertise when evaluating potential advisors.

Building a Comprehensive Financial Planning Team

While your personal financial advisor near me serves as the primary coordinator, comprehensive financial planning often involves multiple professionals working collaboratively.

A complete advisory team might include:

Certified Public Accountant (CPA) for tax preparation, planning, and compliance matters. The relationship between financial advisors and CPAs creates opportunities for integrated tax-aware investment strategies.

Estate Planning Attorney to draft wills, trusts, and other legal documents that protect your assets and ensure proper wealth transfer according to your wishes.

Insurance Specialist who analyzes coverage needs for life, disability, long-term care, and property protection.

Mortgage Broker or Banker when real estate decisions involve significant financial implications.

The best advisory relationships involve professionals who communicate with each other (with your permission) to ensure all aspects of your financial life work together cohesively. Your primary advisor can often facilitate these connections and coordinate the overall strategy.

Understanding the Client-Advisor Relationship Timeline

The relationship with your personal financial advisor near me typically follows a structured progression from initial engagement through ongoing management.

Typical Engagement Process

-

Discovery Meeting: Initial conversation to discuss your situation, goals, and concerns (often complimentary)

-

Data Gathering: Comprehensive collection of financial information, including assets, liabilities, income, and expenses

-

Analysis Phase: Advisor reviews data, identifies opportunities and challenges, and develops recommendations

-

Plan Presentation: Detailed review of proposed strategies with explanations and projected outcomes

-

Implementation: Executing recommendations, which may include opening accounts or initiating transactions

-

Ongoing Monitoring: Regular reviews to track progress, adjust strategies, and address life changes

The frequency of ongoing reviews varies by advisor and client preference. Quarterly check-ins work well for some relationships, while others prefer semi-annual or annual comprehensive reviews with ad-hoc contact as needed.

Life events like marriage, career changes, inheritance, or major purchases should trigger additional conversations with your advisor to adjust plans accordingly.

Technology Tools Enhancing Advisory Services

Modern financial advisors leverage sophisticated technology platforms to enhance service delivery and client experience. These tools have become standard in the industry by 2026.

Financial planning software creates detailed projections showing how different decisions impact your long-term financial trajectory. These programs model various scenarios, helping you visualize trade-offs between current spending and future security.

Portfolio management systems track investments in real-time, automatically rebalancing when allocations drift from targets and generating performance reports that clarify how your portfolio is working toward your goals.

Client portals provide 24/7 access to account information, financial plans, and important documents. Many platforms include secure messaging features for convenient communication with your advisor.

Aggregation tools consolidate information from multiple financial institutions into a single dashboard, giving both you and your advisor a complete picture of your financial situation without manual data entry.

These technological capabilities enable more efficient service delivery while maintaining the personalized guidance that characterizes effective advisory relationships. For those exploring comprehensive services, understanding available technology helps set appropriate expectations.

Red Flags to Watch During Your Search

Certain warning signs indicate potential problems with a personal financial advisor near me. Awareness of these red flags helps protect you from unsuitable relationships or potentially problematic situations.

Guaranteed returns represent a major warning sign. No legitimate advisor can guarantee specific investment performance, as markets involve inherent uncertainty and risk.

Pressure tactics pushing you to make immediate decisions without adequate time for consideration suggest the advisor prioritizes their interests over yours.

Vague fee explanations that avoid direct answers about compensation should raise concerns. Transparent advisors readily explain how they're paid.

Lack of credentials or unwillingness to provide regulatory information may indicate insufficient qualifications or attempts to hide disciplinary history.

Overly complex strategies that you don't understand after reasonable explanation could signal either poor communication skills or unnecessarily complicated approaches designed to justify higher fees.

Promises of exclusive opportunities or investments only available through specific advisors often involve higher risks or conflicts of interest that may not align with your situation.

Trust your instincts during the evaluation process. If something feels uncomfortable or unclear, seek clarification or consider other advisors before committing to a relationship.

Evaluating Performance and Service Quality

Once you've established a relationship with a personal financial advisor near me, ongoing evaluation ensures the partnership continues meeting your needs effectively.

Performance assessment involves multiple dimensions beyond simple investment returns:

| Evaluation Factor | What to Consider | Review Frequency |

|---|---|---|

| Investment Performance | Returns relative to benchmarks and risk level | Quarterly |

| Communication Quality | Responsiveness, clarity, proactive outreach | Ongoing |

| Plan Progress | Movement toward stated goals | Semi-annually |

| Service Level | Meeting frequency, report quality, accessibility | Annually |

| Value Perception | Benefits received relative to fees paid | Annually |

Investment performance should be evaluated against appropriate benchmarks that reflect your portfolio's risk profile and asset allocation. Comparing your returns to unrelated indices provides little meaningful information about whether your advisor is adding value.

Consider both quantitative metrics and qualitative factors. An advisor who communicates clearly, responds promptly, and helps you stay disciplined during market volatility adds significant value that doesn't appear in performance reports.

Regular assessment helps identify when adjustments to the relationship or potentially changing advisors might serve your interests better. Your financial situation and needs evolve, and your advisory relationship should evolve accordingly.

Making the Transition to a New Advisor

Changing financial advisors, while sometimes necessary, involves important considerations and practical steps to ensure a smooth transition.

Valid reasons for changing advisors include poor communication, underperformance relative to expectations, misaligned investment philosophy, life changes requiring different expertise, or discovering more suitable service models.

The transition process typically involves:

- Providing written notice to your current advisor according to any agreement terms

- Opening new accounts with your chosen advisor before closing existing ones

- Transferring assets through ACAT (Automated Customer Account Transfer) for securities

- Updating beneficiary designations and account registrations

- Reviewing and updating your financial plan with the new advisor

Tax considerations matter during transitions. Avoid unnecessary taxable events by transferring securities in-kind when possible rather than liquidating and repurchasing. Retirement accounts can be transferred without tax consequences if handled properly.

Document the reasons for your change and ensure all account transfers complete successfully. Keep records from your previous advisor for tax purposes and future reference.

Regional Considerations Versus Virtual Access

While searching for a personal financial advisor near me suggests geographic preference, understanding the trade-offs between local and virtual advisors helps you make informed decisions.

Local advisors offer potential advantages:

- Face-to-face meetings for those who prefer in-person interaction

- Familiarity with regional economic conditions and local tax considerations

- Possible connections to local professional networks (attorneys, CPAs)

- Community presence and established local reputation

Virtual-first advisors provide different benefits:

- Access to specialized expertise regardless of location

- Typically lower overhead costs potentially reflected in fees

- Scheduling flexibility without commuting time

- Often more robust technology platforms and digital tools

Geographic location matters less than it once did for most financial planning needs. Federal tax laws, investment markets, and estate planning principles apply nationally. State-specific considerations like income taxes or estate taxes may benefit from local knowledge, though competent advisors can research and address these factors regardless of location.

The quality of the advisor, their expertise, fee structure, and personal fit matter more than physical proximity for most clients in 2026. Many successful advisory relationships operate entirely virtually, with clients and advisors never meeting in person.

Starting Your Search Strategy

Developing a systematic approach to finding your personal financial advisor near me increases the likelihood of identifying the right professional for your needs.

Begin with referrals from trusted sources like family members, colleagues, or other professionals like attorneys and accountants who work with financial advisors regularly. Personal recommendations from people in similar financial situations carry particular weight.

Professional associations maintain directories of qualified advisors:

- National Association of Personal Financial Advisors (NAPFA) for fee-only planners

- Financial Planning Association (FPA) for CFP® professionals

- CFA Institute for investment-focused advisors

Online research through advisor websites, regulatory databases, and third-party platforms provides additional information. Review the advisor's published content, client testimonials, and professional background.

Initial screening should narrow your list to three to five candidates worth interviewing in depth. This manageable number allows thorough evaluation without overwhelming the decision process.

Create a comparison spreadsheet documenting each advisor's credentials, fee structure, services offered, and your impressions from initial conversations. This systematic approach helps you weigh factors objectively rather than making decisions based solely on personality or single factors.

For those interested in exploring estate planning advantages or retirement planning strategies, identifying advisors with demonstrated expertise in these areas should be a priority in your search.

Understanding Advisor Business Models

The structure of an advisory firm influences service delivery, potential conflicts of interest, and your overall experience. Several common business models exist in the financial advisory industry.

Independent registered investment advisors (RIAs) operate their own firms, maintaining custody relationships with third-party custodians like Schwab, Fidelity, or TD Ameritrade. This structure typically provides advisors with flexibility in product selection and fee structures.

Broker-dealer affiliated advisors work within firms that maintain trading and custody capabilities. These relationships may involve product restrictions or revenue-sharing arrangements that create potential conflicts.

Hybrid advisors maintain both RIA and broker-dealer registrations, allowing them to provide fee-based planning while also offering commission-based products when appropriate.

Robo-advisors with human support combine automated investment management with access to human advisors for questions and guidance. This model typically serves clients with simpler needs at lower price points.

Each model has appropriate applications depending on your situation. Complex financial circumstances generally benefit from independent advisors with broader flexibility, while straightforward situations might work well with lower-cost automated solutions supplemented by occasional human guidance.

Understanding how your advisor's business model works helps you recognize potential limitations or conflicts that might affect the recommendations you receive.

Selecting the right personal financial advisor near me requires careful consideration of credentials, compensation models, service offerings, and personal compatibility. The most successful advisory relationships combine technical expertise with clear communication, aligned values, and a genuine commitment to your financial well-being. Whether you choose a local advisor or embrace the flexibility of virtual-first services, prioritizing fiduciary responsibility and transparent fee structures helps ensure the guidance you receive serves your best interests. If you're ready to explore how personalized financial planning can help you achieve your retirement, investment, and estate planning goals, Brookwood Investment Group LLC offers fiduciary guidance tailored to your unique situation through a convenient virtual-first approach.