Selecting a retirement plan provider represents one of the most significant decisions business owners make for their organizations. The paychex 401k platform has emerged as a comprehensive solution for companies seeking to integrate retirement benefits with their existing payroll infrastructure. Understanding how these plans function, their administrative features, and their potential impact on employee retention can help business owners make informed decisions about their retirement offerings. This guide examines the structure, benefits, and considerations associated with Paychex retirement services to provide clarity for decision-makers evaluating their options.

Understanding Paychex 401k Plan Options

Paychex offers multiple retirement plan configurations designed to accommodate businesses of varying sizes and complexity levels. The platform provides traditional 401(k) plans, Safe Harbor options, and more specialized solutions tailored to specific organizational needs.

Traditional 401k Plans

The standard paychex 401k operates as an employer-sponsored retirement savings vehicle allowing employees to contribute pre-tax dollars from their paychecks. Employers can choose to match employee contributions according to predetermined formulas, creating a valuable benefit that supports long-term financial security.

These plans include several key components:

- Automatic payroll deduction integration

- Investment menu selection and management

- Compliance monitoring and reporting

- Participant education resources

- Loan and hardship withdrawal provisions

The Paychex retirement services platform centralizes these functions within a single administrative interface, reducing the complexity business owners face when managing multiple vendor relationships.

Pooled Employer Plans

One innovative option within the paychex 401k ecosystem is the Pooled Employer Plan (PEP) structure. This arrangement allows multiple unrelated employers to participate in a single retirement plan, distributing administrative responsibilities and fiduciary obligations across the pool.

| Feature | Traditional 401k | Pooled Employer Plan |

|---|---|---|

| Fiduciary Responsibility | Employer bears primary responsibility | Shared with pooled plan provider |

| Administrative Costs | Higher per-participant expenses | Economies of scale reduce costs |

| Compliance Testing | Individual employer testing | Pooled testing across participants |

| Plan Design Flexibility | Full customization available | Standardized structure |

The Pooled Employer Plans offered through Paychex may be particularly attractive for smaller businesses that lack dedicated human resources departments. This structure transfers certain compliance burdens to the pooled plan provider, potentially reducing the risk exposure for individual employers.

Solo 401k Solutions

Business owners without employees beyond themselves and their spouses can access Solo 401k arrangements through the paychex 401k platform. These plans offer substantially higher contribution limits than traditional IRAs, allowing self-employed professionals to accelerate their retirement savings.

Solo participants can contribute in dual capacities:

- Employee deferrals up to $23,500 in 2026 (or $31,000 for those age 50+)

- Employer profit-sharing contributions up to 25% of compensation

- Combined maximum contribution of $70,000 annually (or $77,500 with catch-up)

This structure provides significant tax advantages for high-earning sole proprietors and single-member LLCs seeking to maximize their retirement contributions.

Administrative Features and Technology

The operational efficiency of any retirement plan depends heavily on its administrative platform. The paychex 401k system integrates with the company's broader suite of human capital management tools, creating potential workflow advantages for businesses already using Paychex for payroll processing.

Payroll Integration

Seamless connection between payroll and retirement plan administration eliminates duplicate data entry and reduces error rates. When employees adjust their contribution percentages, those changes flow automatically through the payroll system, ensuring accurate deductions occur without manual intervention.

Key integration benefits include:

- Real-time contribution calculations

- Automated compliance limit monitoring

- Simplified reconciliation processes

- Reduced administrative time requirements

This integration proves particularly valuable during year-end processing when businesses must generate accurate reporting for tax purposes and regulatory filings.

Participant Portal Access

Modern retirement plan participants expect on-demand access to their account information. The paychex 401k platform provides digital portals where employees can review their balances, adjust contribution rates, modify investment allocations, and access educational resources.

The participant experience includes mobile application access, allowing employees to monitor their retirement progress regardless of location. This accessibility supports engagement with the plan, potentially leading to higher participation rates and improved retirement readiness among the workforce.

Investment Options and Fiduciary Considerations

Investment selection represents a critical component of any retirement plan's value proposition. The paychex 401k typically offers tiered investment menus ranging from basic options suitable for novice investors to more sophisticated choices for experienced participants.

Investment Menu Structure

Most plans include:

- Target-date funds aligned with retirement timelines

- Index funds tracking major market benchmarks

- Actively managed mutual funds across asset classes

- Stable value or money market options for conservative investors

- Self-directed brokerage windows for advanced participants (in some plans)

Plan sponsors must balance providing adequate choice with avoiding decision paralysis that can result from overwhelming participants with too many options. Research suggests that offering between 10 and 15 core investment choices optimizes both engagement and decision quality.

Fiduciary Responsibility

Employers sponsoring retirement plans assume fiduciary duties under the Employee Retirement Income Security Act (ERISA). These responsibilities include selecting and monitoring service providers, ensuring reasonable plan fees, and acting in participants' best interests when making plan-related decisions.

Working with a fiduciary advisory services provider can help business owners navigate these obligations more effectively. Independent advisors can assist with investment menu construction, fee benchmarking, and ongoing plan monitoring to help ensure compliance with regulatory requirements.

The paychex 401k platform includes tools designed to support fiduciary compliance, but ultimate responsibility remains with the plan sponsor. Understanding this distinction is essential for business owners evaluating whether to engage additional advisory support.

Cost Structure and Fee Transparency

Retirement plan costs impact both employers and employees. Understanding the fee architecture within a paychex 401k helps business owners evaluate the total cost of offering retirement benefits and compare alternatives effectively.

Fee Components

Retirement plan expenses typically divide into several categories:

| Fee Type | Description | Typical Payer |

|---|---|---|

| Plan Administration | Recordkeeping, compliance testing, reporting | Employer or shared |

| Investment Management | Fund expense ratios | Participant |

| Advisory Services | Investment selection, monitoring, education | Varies by arrangement |

| Transaction Fees | Loans, distributions, QDROs | Participant |

Transparency regarding these costs has increased significantly following Department of Labor regulations requiring detailed fee disclosure. The paychex 401k platform provides fee reporting tools that help satisfy these disclosure obligations.

Cost Comparison Considerations

When evaluating whether a paychex 401k represents a cost-effective solution, business owners should consider total plan expenses relative to the service package received. Reviews of Paychex services note that bundled pricing can offer advantages for companies using multiple Paychex products, though standalone retirement plan costs may vary based on plan size and complexity.

Benchmarking against industry standards helps determine whether plan fees fall within reasonable ranges. Plans with fewer than 100 participants typically experience higher per-participant costs due to fixed administrative expenses being spread across smaller populations.

Compliance and Testing Requirements

Regulatory compliance represents an ongoing obligation for retirement plan sponsors. The paychex 401k includes compliance monitoring tools designed to help employers meet their testing and reporting obligations.

Annual Testing Protocols

Non-Safe Harbor plans must complete several annual tests:

- Actual Deferral Percentage (ADP) Test: Ensures highly compensated employees don't defer disproportionately compared to non-highly compensated employees

- Actual Contribution Percentage (ACP) Test: Similar to ADP but applies to matching contributions

- Top-Heavy Test: Determines whether plan benefits are too concentrated among key employees

- Coverage Test: Verifies that sufficient percentages of non-highly compensated employees benefit from the plan

Safe Harbor plan designs can eliminate ADP and ACP testing requirements by implementing required employer contributions, though this approach increases employer costs.

The paychex 401k platform automates much of the testing process, generating preliminary results and identifying potential compliance issues before they result in regulatory problems. However, plan sponsors remain responsible for understanding test results and implementing corrective actions when necessary.

Form 5500 Filing

Annual Form 5500 reporting to the Department of Labor and IRS constitutes a fundamental compliance requirement. The paychex 401k service typically includes Form 5500 preparation and filing as part of its administrative package, though sponsors should verify what services are included in their specific service agreement.

Plans with 100 or more participants require an independent audit as part of the Form 5500 filing process, adding both complexity and cost to plan administration. Understanding these requirements before implementing a plan helps business owners budget appropriately for ongoing expenses.

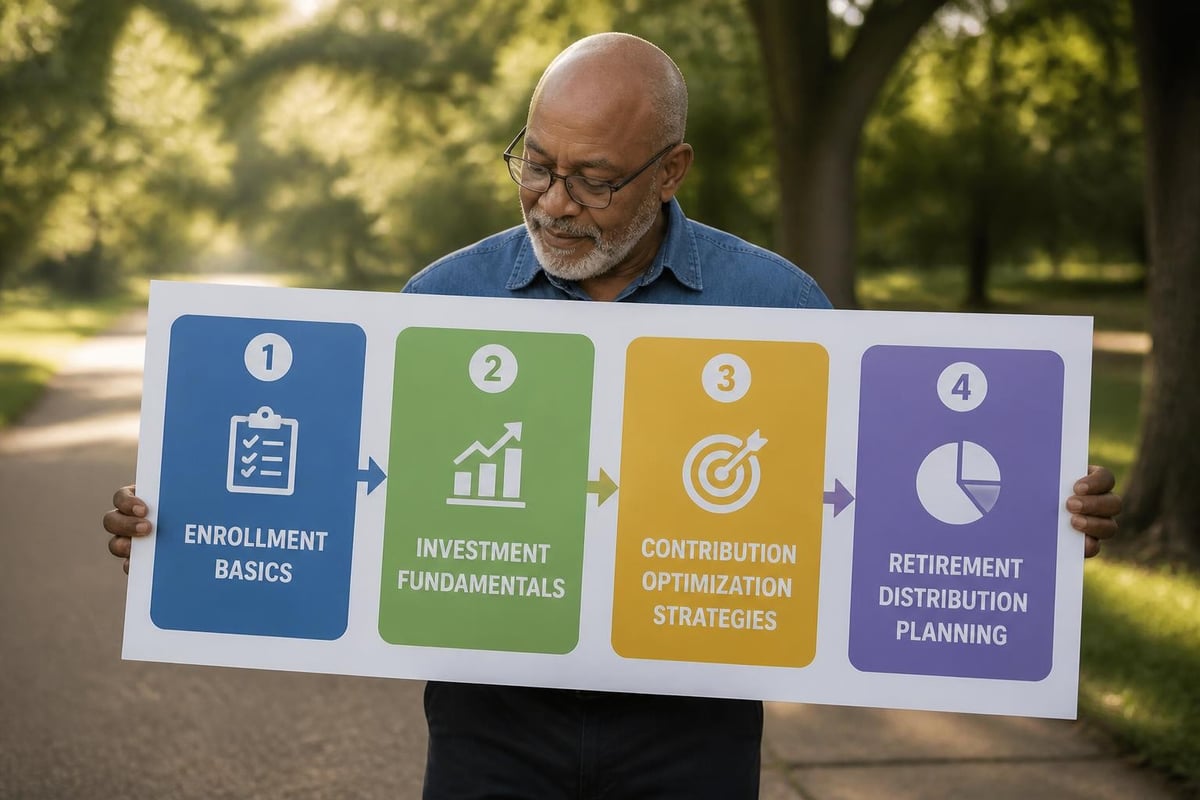

Participant Education and Engagement

Retirement plan value extends beyond merely offering the benefit. Actual participant engagement determines whether employees utilize the plan effectively to build retirement security. The paychex 401k includes educational resources designed to support participant understanding and engagement.

Educational Resources

Comprehensive retirement education addresses multiple knowledge levels:

- Basic enrollment education: Explains how to enroll, contribution mechanics, and employer matching formulas

- Investment fundamentals: Covers asset allocation principles, risk tolerance assessment, and diversification concepts

- Retirement planning: Provides tools for projecting retirement needs and evaluating progress toward goals

- Distribution planning: Explains options at retirement and strategies for converting accumulated savings into retirement income

Research consistently demonstrates that participants who engage with educational resources make better-informed decisions and achieve improved retirement outcomes. Employers benefit from this engagement through enhanced employee satisfaction and reduced financial stress among their workforce.

Auto-Enrollment Features

Behavioral economics research has revealed that default options significantly influence participant behavior. The paychex 401k supports automatic enrollment features that can substantially increase participation rates among eligible employees.

Auto-enrollment typically includes:

- Automatic deferral elections at a specified percentage (commonly 3% or 4%)

- Default investment allocation to target-date funds or balanced options

- Automatic escalation provisions increasing deferrals annually

- Opt-out procedures for employees who prefer not to participate

Plans implementing auto-enrollment often achieve participation rates exceeding 90%, compared to 60-75% for voluntary enrollment plans. This broad participation helps plans pass compliance tests more easily and ensures more employees benefit from the retirement savings opportunity.

Advisor Integration and Support

Financial advisors play increasingly important roles in retirement plan management. The Paychex partnerships with financial advisors enable professional guidance to complement administrative services.

Advisory Service Models

Advisors working with paychex 401k plans typically provide services under one of several arrangements:

3(21) Fiduciary Services: Advisor provides recommendations regarding investment menu construction and monitoring, but plan sponsor retains decision-making authority and associated liability.

3(38) Investment Manager Services: Advisor assumes discretionary authority over investment selection and monitoring, accepting fiduciary responsibility for these functions.

Non-Fiduciary Education: Advisor provides participant education and enrollment support without assuming fiduciary responsibility for investment outcomes.

Understanding these service models helps business owners determine what level of advisory support aligns with their risk tolerance and internal capabilities. Businesses with sophisticated finance teams might require less comprehensive advisory support than smaller organizations lacking internal expertise.

Coordinating Payroll and Retirement Services

One potential advantage of the paychex 401k is the integration potential when businesses use Paychex for both payroll processing and retirement plan administration. This coordination can streamline operations and reduce the number of vendor relationships requiring management.

However, business owners should avoid allowing administrative convenience to override careful evaluation of plan quality and costs. Working with independent advisors who can provide objective assessments helps ensure retirement plan decisions prioritize employee outcomes and fiduciary compliance rather than operational simplicity alone.

Those seeking retirement planning and estate planning guidance often benefit from coordinating employer retirement plan selections with their broader financial strategy, ensuring consistency across all aspects of their financial life.

User Experience and Satisfaction

Understanding how other businesses and participants experience the paychex 401k provides valuable context for decision-making. While individual experiences vary, examining patterns in user feedback can reveal strengths and potential concerns.

Positive Feedback Themes

Users frequently cite several advantages:

- Streamlined administration when bundled with Paychex payroll services

- Responsive customer service for routine inquiries

- Comprehensive reporting capabilities

- Effective integration reducing duplicate data entry

These benefits align with the platform's value proposition of creating operational efficiency through integrated human capital management systems.

Common Concerns

User reviews on various platforms also identify areas where some clients have experienced challenges. Recurring themes in critical feedback include questions about fee transparency, responsiveness during complex situations, and the learning curve associated with navigating administrative interfaces.

Prospective clients should conduct thorough due diligence, including requesting detailed fee disclosures, speaking with current clients in similar industries, and understanding service level agreements before committing to any retirement plan provider.

Comparing Paychex to Alternative Providers

The retirement plan market offers numerous provider options, each with distinct strengths. Evaluating how the paychex 401k compares to alternatives helps business owners make informed decisions aligned with their specific needs.

Provider Comparison Framework

When comparing retirement plan providers, consider:

| Evaluation Factor | Questions to Address |

|---|---|

| Service Integration | Does the provider integrate with existing payroll and HR systems? |

| Plan Design Flexibility | Can plan features be customized to match business objectives? |

| Investment Quality | Are investment options cost-effective and appropriately diversified? |

| Technology Platform | Is the participant interface intuitive and mobile-accessible? |

| Advisory Support | What level of fiduciary assistance is available? |

| Pricing Transparency | Are all fees clearly disclosed and competitively positioned? |

No single provider optimally serves all business types and sizes. A paychex 401k might represent an ideal solution for a 50-person manufacturing company using Paychex payroll services, while a technology startup with distributed remote workers might prioritize different platform capabilities.

Specialized Provider Considerations

Some businesses benefit from working with retirement plan providers specializing in their industry or employee demographic. For example, professional services firms with highly compensated partners might prioritize providers offering sophisticated plan design capabilities, while retail businesses with high employee turnover might emphasize simplicity and ease of enrollment.

Business owners considering whether a paychex 401k aligns with their needs should evaluate their specific circumstances rather than relying on generalized recommendations. Consulting with advisors experienced in retirement planning can provide personalized insights based on the business's unique characteristics.

Implementation Timeline and Process

Establishing a new retirement plan or transitioning from an existing provider involves multiple steps and coordination across various stakeholders. Understanding the typical implementation timeline for a paychex 401k helps business owners plan appropriately.

Implementation Phases

Phase 1: Plan Design (2-4 weeks)

- Determine plan structure and features

- Establish eligibility requirements and vesting schedules

- Select employer contribution formulas

- Choose investment menu

Phase 2: Documentation (2-3 weeks)

- Prepare adoption agreement

- Draft summary plan description

- Create enrollment materials

- File necessary regulatory documents

Phase 3: System Configuration (1-2 weeks)

- Configure payroll integration

- Set up participant portal

- Load employee data

- Test contribution processing

Phase 4: Employee Communication (2-4 weeks)

- Conduct enrollment meetings

- Distribute plan information

- Provide one-on-one enrollment support

- Address employee questions

The complete implementation process typically requires 8-12 weeks from initial plan design through first payroll contributions. Businesses transitioning from existing providers may require additional time to coordinate asset transfers and ensure continuity of participant accounts.

Tax Advantages for Employers and Employees

Retirement plan sponsorship generates valuable tax benefits for both businesses and their employees, creating financial advantages beyond the core retirement savings objective.

Employer Tax Benefits

Businesses offering retirement plans can access several tax advantages:

- Contribution Deductions: Employer contributions are generally deductible as business expenses, reducing taxable income

- Tax Credits: Small businesses may qualify for startup credits covering plan establishment costs

- SECURE Act Credits: Enhanced credits available for adding automatic enrollment features

- State Tax Benefits: Various states offer additional tax incentives for retirement plan sponsorship

These tax advantages can offset a portion of plan costs, improving the overall value proposition for employers. The paychex 401k platform includes reporting tools that help businesses track deductible contributions and generate documentation supporting tax filings.

Employee Tax Advantages

Participants in traditional 401k plans receive immediate tax benefits through pre-tax contributions that reduce current taxable income. A participant earning $75,000 who contributes $7,500 annually reduces their taxable income to $67,500, generating immediate tax savings.

Roth 401k options, increasingly common in paychex 401k plans, provide an alternative tax treatment. While Roth contributions don't reduce current taxable income, qualified distributions in retirement occur tax-free, potentially benefiting participants who expect higher tax rates in the future.

Understanding these tax dynamics helps employees make informed decisions about contribution strategies aligned with their individual circumstances. Providing access to financial planning and investment management resources supports more sophisticated decision-making among plan participants.

Plan Monitoring and Ongoing Management

Implementing a retirement plan represents the beginning rather than the end of sponsor responsibilities. Ongoing monitoring ensures the paychex 401k continues meeting employee needs and satisfying regulatory requirements.

Quarterly Review Activities

Regular plan reviews should address:

- Participation rate trends and engagement levels

- Investment performance relative to benchmarks

- Fee competitiveness compared to industry standards

- Compliance with contribution limits and testing requirements

- Service provider performance and responsiveness

Documenting these reviews creates evidence of prudent fiduciary oversight, an important protection should questions arise about plan management decisions.

Annual Committee Meetings

Many businesses establish retirement plan committees responsible for oversight and decision-making. These committees typically meet at least annually to review comprehensive plan metrics and make strategic decisions regarding plan design, investments, and service providers.

Annual meeting agendas commonly include:

- Review of prior year participation and contribution data

- Analysis of investment menu performance

- Evaluation of service provider performance

- Assessment of plan fee competitiveness

- Consideration of plan design modifications

- Approval of updated plan documents

Maintaining detailed meeting minutes demonstrates the disciplined oversight process regulators expect from plan sponsors.

Future Trends in Retirement Plan Administration

The retirement plan industry continues evolving in response to technological advancement, regulatory changes, and shifting participant expectations. Understanding emerging trends helps business owners anticipate how the paychex 401k and alternative platforms may develop.

Technology Integration

Artificial intelligence and machine learning are increasingly incorporated into retirement plan platforms, enabling:

- Personalized contribution recommendations based on participant characteristics

- Automated portfolio rebalancing aligned with target-date glide paths

- Predictive analytics identifying at-risk participants who may benefit from additional support

- Enhanced cybersecurity protecting participant data and account access

These technological capabilities promise to improve participant outcomes while reducing administrative burdens for plan sponsors.

Emergency Savings Integration

Recent regulatory changes permit retirement plans to include emergency savings components, allowing participants to build short-term reserves alongside long-term retirement savings. This integration acknowledges that financial security requires addressing both immediate and future needs.

The paychex 401k platform may incorporate these features as regulations develop, providing participants with more comprehensive financial wellness tools within a single administrative framework.

Lifetime Income Solutions

Growing recognition that retirement security depends not just on accumulating assets but also on effectively converting those assets into reliable income has driven increased focus on lifetime income options. More retirement plans are incorporating annuity options and other guaranteed income products to help participants address longevity risk.

Understanding how these trends might impact retirement plan design helps business owners anticipate future needs and evaluate whether their current provider demonstrates the innovation necessary to remain competitive over time.

Selecting and managing a retirement plan requires careful consideration of administrative capabilities, cost structures, and alignment with organizational objectives. The paychex 401k offers particular advantages for businesses already using Paychex services, though thorough evaluation remains essential regardless of existing vendor relationships. Working with experienced fiduciary advisors can provide the objective guidance necessary to navigate these complex decisions effectively. Brookwood Investment Group LLC offers personalized retirement planning services tailored to your unique goals, helping both business owners and individuals build comprehensive strategies that integrate employer-sponsored plans with broader financial objectives. Our virtual-first approach provides accessible expertise when you need guidance on retirement decisions that will impact your financial future.