Making the decision to meet with a financial advisor represents a significant step toward achieving your financial objectives. Whether you're planning for retirement, managing investments, or addressing complex tax strategies, a professional partnership can provide the personalized guidance necessary to navigate today's financial landscape. Understanding how to prepare for this meeting and what to expect can help you establish a productive relationship that aligns with your unique goals and lifestyle. This guide walks you through the essential considerations for maximizing the value of your advisory relationship.

Understanding the Value of Professional Financial Guidance

Financial advisory services have evolved substantially over the past decade. The shift toward virtual-first models has made professional guidance more accessible than ever before, eliminating geographical barriers while maintaining the personalized attention clients need.

When you meet with a financial advisor, you're accessing expertise across multiple disciplines. These professionals bring knowledge in areas such as retirement planning, investment management, tax optimization, and estate planning. Rather than attempting to master each domain independently, you gain a coordinated strategy that addresses how these elements interconnect.

Key benefits of professional guidance include:

- Objective perspective on financial decisions

- Access to sophisticated planning tools and analytics

- Coordination between various aspects of your financial life

- Regular accountability and progress monitoring

- Adaptation to changing circumstances and regulations

The fiduciary standard adds another layer of value. Fiduciary advisors are legally obligated to prioritize your interests above their own, creating a foundation of trust that's essential for long-term planning relationships.

Preparing for Your Initial Consultation

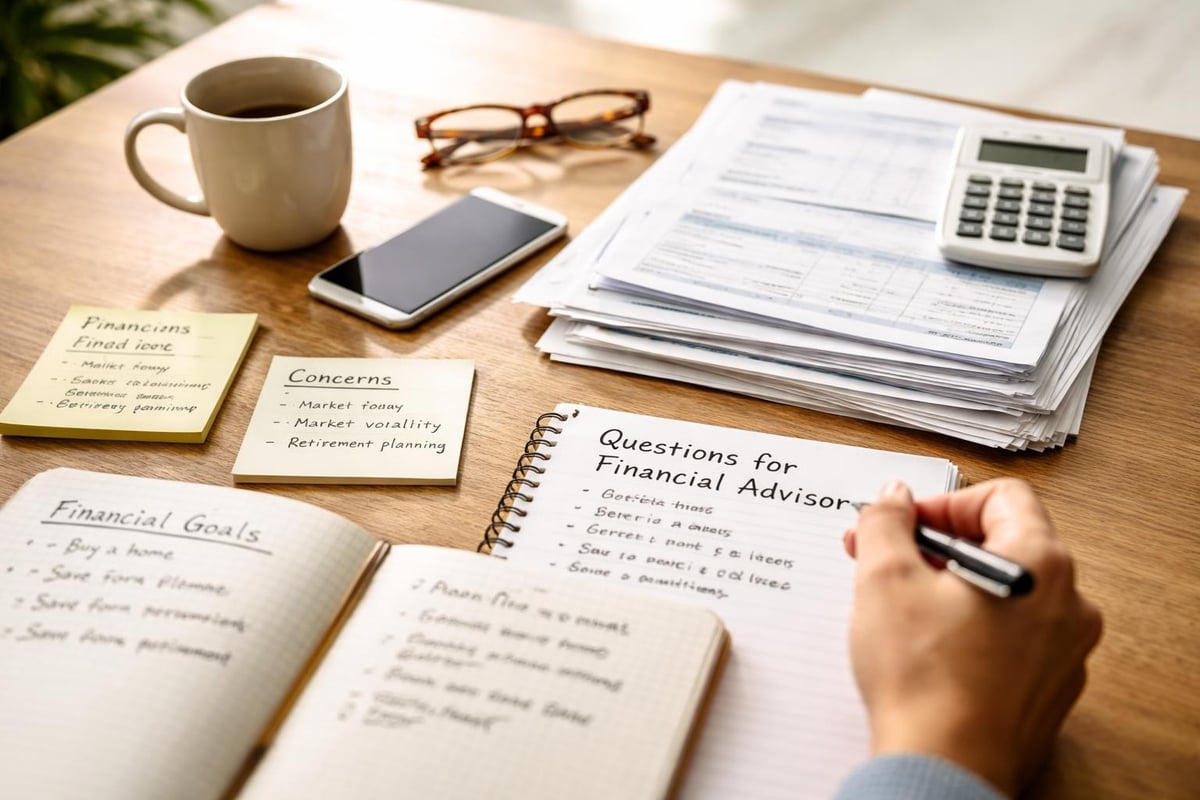

Preparation significantly influences the productivity of your first meeting. Gathering relevant financial documents before your consultation enables your advisor to provide more specific recommendations rather than general observations.

Essential Documents to Compile

Start by organizing your current financial statements. This includes bank accounts, investment portfolios, retirement accounts, and any real estate holdings. Don't worry about achieving perfect organization; the goal is providing a comprehensive snapshot of your current position.

Your document checklist should include:

- Recent statements from all investment and retirement accounts

- Current insurance policies (life, disability, long-term care)

- Tax returns from the previous two years

- Estate planning documents (wills, trusts, powers of attorney)

- Employee benefits summaries

- Outstanding debt information (mortgages, loans, credit cards)

Beyond documentation, defining your financial goals represents perhaps the most critical preparation step. Consider both short-term objectives (one to three years) and long-term aspirations (ten years or more). These might include retirement at a specific age, funding education, purchasing property, or leaving a legacy.

Clarifying Your Financial Philosophy

Understanding your own preferences and concerns helps advisors tailor their approach. Reflect on questions such as: How comfortable are you with investment risk? What keeps you awake at night financially? Have you experienced financial setbacks that influence your current thinking?

Your relationship with money often stems from personal experiences, family background, and individual values. Sharing this context during your initial consultation helps advisors understand not just what you want to achieve, but why those goals matter to you.

What to Expect During Your Meeting

The structure of your initial consultation typically follows a discovery-focused approach. Rather than presenting immediate solutions, quality advisors invest time understanding your complete financial picture and personal circumstances.

| Meeting Phase | Duration | Primary Focus |

|---|---|---|

| Introduction & Relationship Building | 10-15 minutes | Establishing rapport, explaining process |

| Financial Discovery | 30-40 minutes | Reviewing documents, discussing goals |

| Preliminary Assessment | 15-20 minutes | Identifying opportunities and concerns |

| Next Steps Discussion | 10-15 minutes | Outlining recommendation timeline |

Most initial consultations last between 60 and 90 minutes. Virtual meetings through platforms like Zoom have become standard practice, offering convenience without sacrificing the personal connection necessary for effective planning.

Working with a financial advisor involves open communication about sensitive topics. Your advisor will likely ask detailed questions about income, expenses, assets, debts, and family dynamics. This information remains confidential and enables personalized recommendations aligned with your specific situation.

Questions to Ask Your Potential Advisor

Selecting the right advisor requires careful evaluation. The questions you ask during your initial meeting reveal important information about their approach, qualifications, and compatibility with your needs.

Credentials and Experience

Start by understanding their professional background. What certifications do they hold? How long have they been practicing? What types of clients do they typically work with? Advisors who specialize in situations similar to yours often provide more relevant insights.

Essential qualification questions:

- What professional designations have you earned (CFP®, CFA, etc.)?

- How do you stay current with changing regulations and strategies?

- What is your experience with clients in my age range or financial situation?

- Are you a fiduciary at all times when working with clients?

Service Model and Communication

Understanding how the relationship will function on a practical level prevents future misunderstandings. How frequently will you meet? What communication methods does the advisor use? How quickly can you expect responses to questions?

The shift toward virtual-first advisory services has changed traditional service models. Many clients appreciate the flexibility of video consultations combined with secure document sharing platforms, though preferences vary.

Compensation Structure

Transparency regarding fees establishes trust from the beginning. Advisors may charge through various models: assets under management (AUM) percentages, flat annual fees, hourly rates, or project-based pricing. Each structure has implications for how recommendations might be influenced.

Understanding fee structures helps you evaluate the relationship's total cost. Don't hesitate to ask for specific numbers based on your situation rather than hypothetical examples.

Building a Productive Long-Term Partnership

The initial meeting represents just the beginning of your advisory relationship. The most valuable outcomes emerge through ongoing collaboration as your life circumstances evolve and financial markets change.

Setting Realistic Expectations

Financial planning isn't a one-time transaction but rather a continuous process. Markets fluctuate, tax laws change, families grow, and careers evolve. Your financial strategy should adapt accordingly through regular reviews and adjustments.

Quality advisors set clear expectations about what they can and cannot control. They can provide informed guidance, disciplined investment approaches, and strategic planning. They cannot guarantee specific investment returns or eliminate all financial uncertainty.

Establishing Communication Rhythms

Determine a review schedule that fits your preferences and situation complexity. Some clients benefit from quarterly check-ins, while others prefer semi-annual or annual comprehensive reviews. Between scheduled meetings, you should feel comfortable reaching out with questions or concerns as they arise.

Technology enables more frequent touchpoints without requiring formal meetings. Many advisory firms provide client portals where you can monitor accounts, review reports, and access planning documents whenever convenient.

Addressing Specific Life Situations

Different life stages and circumstances require tailored approaches when you meet with a financial advisor. The priorities of a young professional differ substantially from those of someone approaching retirement or managing inherited wealth.

Pre-Retirement Planning

For individuals within 10-15 years of retirement, planning intensity typically increases. Conversations shift from accumulation strategies to distribution planning. How will you convert savings into sustainable income? What role will Social Security play? How should healthcare costs factor into your planning?

Retirement planning strategies must address sequence of returns risk, tax-efficient withdrawal strategies, and estate considerations. These complex topics benefit significantly from professional guidance tailored to your specific timeline and resources.

Business Owners and High-Earning Professionals

Entrepreneurs and professionals with substantial income face unique challenges. Business succession planning, concentrated stock positions, and advanced tax strategies require specialized expertise. Your advisor should understand how business interests integrate with personal financial goals.

Estate planning takes on added complexity for business owners. Protecting your business while providing for family members and minimizing tax implications requires careful coordination between your advisory team and estate planning attorney.

Maximizing the Value of Advisory Services

Getting the most from your advisory relationship requires active participation. While your advisor provides expertise and recommendations, you maintain responsibility for decisions affecting your financial future.

Providing Complete Information

Advisors can only offer appropriate guidance based on the information you share. Withholding details about assets, debts, or goals prevents comprehensive planning. This includes discussing uncomfortable topics such as family conflicts, health concerns, or financial mistakes from your past.

Updating your advisor about life changes enables timely adjustments. Marriage, divorce, inheritance, job changes, and health issues all carry financial implications that may require strategy modifications.

Following Through on Recommendations

Implementing financial strategies requires action beyond the planning meeting. Whether opening new accounts, adjusting beneficiaries, or updating estate documents, these tasks demand your attention. Your advisor can guide the process, but you must complete the necessary steps.

Some recommendations may feel uncomfortable initially. Increasing retirement contributions might strain current cash flow. Purchasing insurance addresses risks you'd prefer not to consider. Trusting the strategic reasoning behind recommendations helps you move forward despite natural hesitation.

Maintaining Reasonable Expectations During Market Volatility

Financial markets experience regular fluctuations. When you meet with a financial advisor to review performance during volatile periods, focus on whether your strategy remains aligned with long-term objectives rather than short-term returns.

Advisors help maintain perspective during market stress. Having established a relationship before turbulence occurs makes it easier to stay disciplined when emotions run high. This behavioral coaching often provides as much value as investment selection.

Evaluating the Advisor-Client Fit

Not every advisor is the right match for every client. Chemistry, communication style, and philosophical alignment all influence relationship effectiveness. Assessing these factors honestly helps ensure you're building a partnership that serves your interests.

Communication Compatibility

Does your advisor communicate in ways you understand and appreciate? Some clients prefer detailed technical explanations, while others want simplified overviews focused on action items. Neither approach is superior, but alignment with your preference matters.

Response time and accessibility also factor into satisfaction. If you value immediate responses to questions, ensure your advisor's practice accommodates this expectation. Conversely, if you prefer minimal contact between scheduled reviews, communicate this preference clearly.

Philosophical Alignment

Your advisor's investment philosophy should resonate with your own beliefs and risk tolerance. If you prefer conservative approaches but your advisor consistently recommends aggressive strategies, tension will emerge. Similarly, tax philosophy, estate planning approaches, and risk management perspectives should align.

This alignment extends to personalized financial guidance that respects your values. Whether you prioritize sustainable investing, charitable giving, or family wealth transfer, your advisor should incorporate these priorities into recommendations.

Preparing for Subsequent Meetings

After your initial consultation, ongoing meetings maintain momentum and adapt your plan to changing circumstances. Taking preparatory steps before each review session ensures productive use of time.

Pre-meeting preparation checklist:

- Review progress toward previously established goals

- Note any life changes since your last meeting

- Compile questions or concerns that have emerged

- Update income or expense changes

- Consider whether your risk tolerance has shifted

Bringing updated account statements helps identify any accounts your advisor doesn't manage directly. This complete picture enables holistic advice rather than recommendations based on partial information.

Understanding the Ongoing Relationship

The advisory relationship evolves beyond initial planning into ongoing partnership. Regular reviews assess progress, identify new opportunities, and adjust strategies as needed. This continuous process adapts to both external changes (market conditions, tax law modifications) and personal developments (career transitions, family changes).

| Review Type | Frequency | Primary Purpose |

|---|---|---|

| Comprehensive Review | Annual | Full plan assessment, goal progress, strategy updates |

| Portfolio Review | Quarterly/Semi-annual | Investment performance, rebalancing needs, allocation |

| Ad Hoc Consultation | As needed | Specific questions, life changes, urgent concerns |

| Tax Planning Session | Pre-year-end | Optimization opportunities, estimated payments, withholding |

Quality advisory relationships adapt to your changing needs over time. The strategies appropriate during your accumulation years differ from those needed during retirement. Your advisor should proactively recommend adjustments rather than maintaining static approaches.

Technology and Virtual Advisory Services

The financial advisory industry has embraced technology, making it easier than ever to meet with a financial advisor regardless of location. Video conferencing, secure document sharing, and digital planning tools provide convenience without sacrificing service quality.

Virtual meetings eliminate travel time and enable flexible scheduling. You can participate from your home or office, accessing documents digitally rather than managing paper files. This approach particularly benefits clients with demanding schedules or those who prefer the comfort of familiar surroundings during financial discussions.

Despite technological advances, the relationship remains fundamentally personal. Video meetings preserve the face-to-face connection essential for discussing sensitive financial matters while offering logistical advantages traditional office meetings cannot match.

Special Considerations for Different Advisory Needs

When you meet with a financial advisor, the conversation scope depends on your specific requirements. Some clients need comprehensive planning addressing all financial aspects, while others seek guidance on particular issues.

Investment Management Focus

Clients primarily seeking investment management often have solid financial foundations but want professional portfolio oversight. Discussions center on asset allocation, risk management, rebalancing strategies, and performance monitoring.

Even investment-focused relationships benefit from periodic broader planning reviews. Tax implications, estate considerations, and retirement planning all intersect with investment decisions.

Tax Strategy Integration

Tax planning strategies significantly impact wealth accumulation and preservation. Advisors who coordinate with tax professionals or possess tax expertise themselves help you navigate complex situations such as Roth conversions, required minimum distributions, charitable giving strategies, and capital gains management.

The relationship between your financial advisor and CPA should be collaborative. Ensuring both professionals communicate prevents conflicting advice and enables coordinated strategies that optimize your overall financial picture.

Estate Planning Coordination

While attorneys draft legal documents, financial advisors play crucial roles in estate planning by quantifying needs, modeling scenarios, and coordinating asset titling with estate objectives. This collaboration ensures your estate plan functions as intended while minimizing unnecessary tax burden.

Discussions about legacy goals can feel uncomfortable but provide important guidance for comprehensive planning. How do you want assets distributed? What values do you want to instill in heirs? Are charitable intentions part of your vision?

Meeting with a financial advisor offers the opportunity to gain clarity, confidence, and direction regarding your financial future. The most successful relationships begin with thorough preparation, honest communication, and alignment on goals and philosophy. Brookwood Investment Group provides fiduciary guidance through a virtual-first approach, offering personalized strategies for retirement planning, investment management, estate planning, and tax optimization tailored to your unique circumstances and lifestyle.