Understanding the maximum income for Roth IRA eligibility is essential for anyone looking to maximize tax-advantaged retirement savings in 2026. While Roth IRAs offer significant benefits including tax-free growth and qualified withdrawals, not everyone qualifies to contribute directly. The Internal Revenue Service establishes income limits that determine whether you can make full contributions, reduced contributions, or no contributions at all. These thresholds adjust annually based on inflation, making it important to review your eligibility each year as your income changes.

Understanding Roth IRA Income Limits for 2026

The maximum income for Roth IRA contributions in 2026 depends on your tax filing status and Modified Adjusted Gross Income (MAGI). The IRS uses a phase-out range system, where your contribution allowance gradually decreases as your income approaches the upper threshold.

For single filers and heads of household in 2026, the phase-out range begins at $150,000 and ends at $165,000. This means if your MAGI falls below $150,000, you can make the full contribution. Between $150,000 and $165,000, your contribution limit reduces proportionally. Once your income exceeds $165,000, you cannot contribute directly to a Roth IRA.

Income Thresholds by Filing Status

Different filing statuses face different income restrictions. The Roth IRA contribution and income limits have been updated to reflect 2026 adjustments.

Single Filers and Heads of Household:

- Full contribution: MAGI below $150,000

- Partial contribution: MAGI between $150,000 and $165,000

- No contribution: MAGI above $165,000

Married Filing Jointly:

- Full contribution: MAGI below $236,000

- Partial contribution: MAGI between $236,000 and $246,000

- No contribution: MAGI above $246,000

Married Filing Separately (if you lived with your spouse at any time during the year):

- Full contribution: Not applicable

- Partial contribution: MAGI below $10,000

- No contribution: MAGI above $10,000

The married filing separately category presents unique challenges. If you lived with your spouse during the year, the maximum income for Roth IRA eligibility drops significantly to just $10,000, making direct contributions nearly impossible for most earners in this category.

Contribution Limits Beyond Income Restrictions

Even when you qualify based on income, contribution limits still apply. For 2026, the maximum contribution is $7,000 for individuals under age 50, with an additional $1,000 catch-up contribution allowed for those aged 50 and older.

These limits represent the combined total you can contribute to all traditional and Roth IRAs. You cannot exceed these amounts even if you have multiple accounts. Working with a fiduciary advisory firm can help ensure you optimize contributions across all retirement vehicles.

| Age Group | Maximum Contribution | Catch-Up Contribution | Total Allowed |

|---|---|---|---|

| Under 50 | $7,000 | $0 | $7,000 |

| 50 and Over | $7,000 | $1,000 | $8,000 |

Your contribution cannot exceed your earned income for the year. If you earned $5,000 in 2026, your maximum contribution is $5,000, regardless of the standard limits.

Calculating Your Modified Adjusted Gross Income

Determining whether you fall within the maximum income for Roth IRA eligibility requires calculating your MAGI. This figure differs from your adjusted gross income (AGI) and taxable income.

To calculate MAGI for Roth IRA purposes, start with your AGI from your tax return. Then add back certain deductions:

- Traditional IRA deductions

- Student loan interest deduction

- Tuition and fees deduction

- Foreign earned income exclusion

- Foreign housing exclusion or deduction

- Excluded savings bond interest

- Excluded employer adoption benefits

Most taxpayers find their MAGI equals or closely approximates their AGI, since many of these add-backs don't apply. However, those with foreign income or specific deductions should calculate carefully to determine eligibility.

Strategies for High Earners

If your income approaches or exceeds the maximum income for Roth IRA thresholds, several strategies can help you continue building tax-free retirement savings.

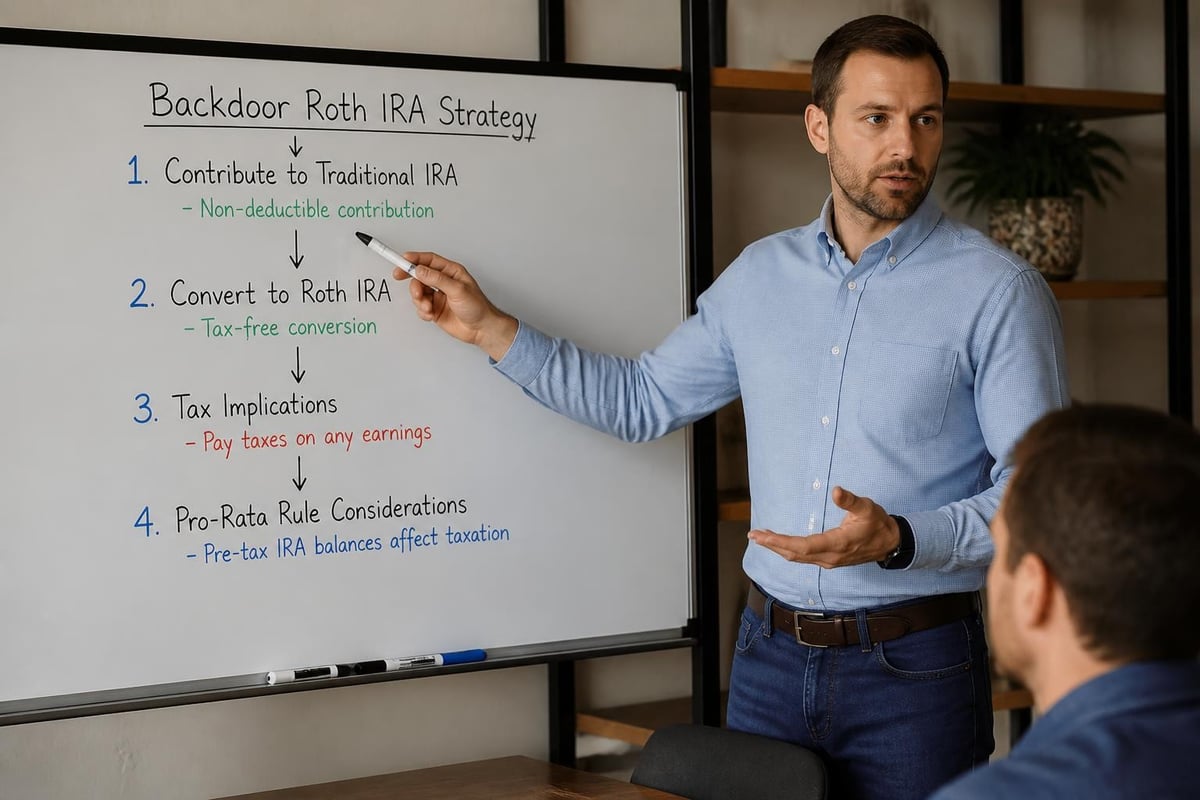

Backdoor Roth IRA Conversions remain a popular option. This involves contributing to a traditional IRA (which has no income limits) and then converting those funds to a Roth IRA. The conversion triggers taxable income on any pre-tax contributions and earnings, but future growth remains tax-free.

Key considerations for backdoor conversions include:

- Pro-rata rule implications if you have existing traditional IRA balances

- Timing of contributions and conversions within the tax year

- State tax implications of conversion income

- Five-year rule for withdrawal of converted amounts

Working with retirement planning specialists ensures you execute these strategies correctly and avoid unnecessary tax consequences.

Spousal Roth IRAs provide another avenue for married couples. Even if one spouse has no earned income, they can contribute to their own Roth IRA based on the working spouse's income, provided the couple files jointly and meets the income requirements. This effectively doubles the household's Roth contribution capacity.

Mega Backdoor Roth strategies through employer 401(k) plans allow significantly larger contributions for those whose employers offer after-tax 401(k) contributions and in-plan Roth conversions. These strategies can move tens of thousands of dollars into Roth accounts annually, far exceeding standard IRA limits.

Phase-Out Range Calculations

Understanding how partial contribution amounts are calculated within the phase-out range helps you maximize allowable contributions when your income falls in this zone.

The formula requires several steps. First, subtract the lower phase-out threshold from your MAGI. Next, divide this amount by the total phase-out range ($15,000 for most filers). Multiply this percentage by the maximum contribution amount, then subtract the result from the maximum contribution to determine your allowed amount.

For example, a single filer with MAGI of $157,500 in 2026:

- $157,500 – $150,000 = $7,500

- $7,500 ÷ $15,000 = 0.5 (50% through phase-out)

- $7,000 × 0.5 = $3,500

- $7,000 – $3,500 = $3,500 allowed contribution

The income limits and phase-out calculations can become complex, particularly when income fluctuates throughout the year or includes variable compensation.

Tax Year Contributions and Deadlines

You can contribute to a Roth IRA for the 2026 tax year from January 1, 2026, through the tax filing deadline in April 2027 (typically April 15). This extended window provides flexibility for year-end income planning.

If you discover in early 2027 that your 2026 income fell below the maximum income for Roth IRA eligibility, you still have time to make contributions for that tax year. Conversely, if your income exceeded expectations, you must remove excess contributions to avoid penalties.

Excess Contribution Consequences

Contributing beyond allowable limits based on income or dollar amounts creates tax complications. The IRS imposes a 6% excise tax on excess contributions for each year they remain in the account.

You can correct excess contributions by:

- Withdrawing the excess plus any earnings before the tax filing deadline

- Recharacterizing contributions to a traditional IRA

- Carrying forward excess as next year's contribution (if eligible)

The earnings portion of withdrawn excess contributions is taxable and may be subject to a 10% early withdrawal penalty if you're under age 59½. For guidance on retirement account strategies and tax implications, consulting experienced advisors helps navigate these situations.

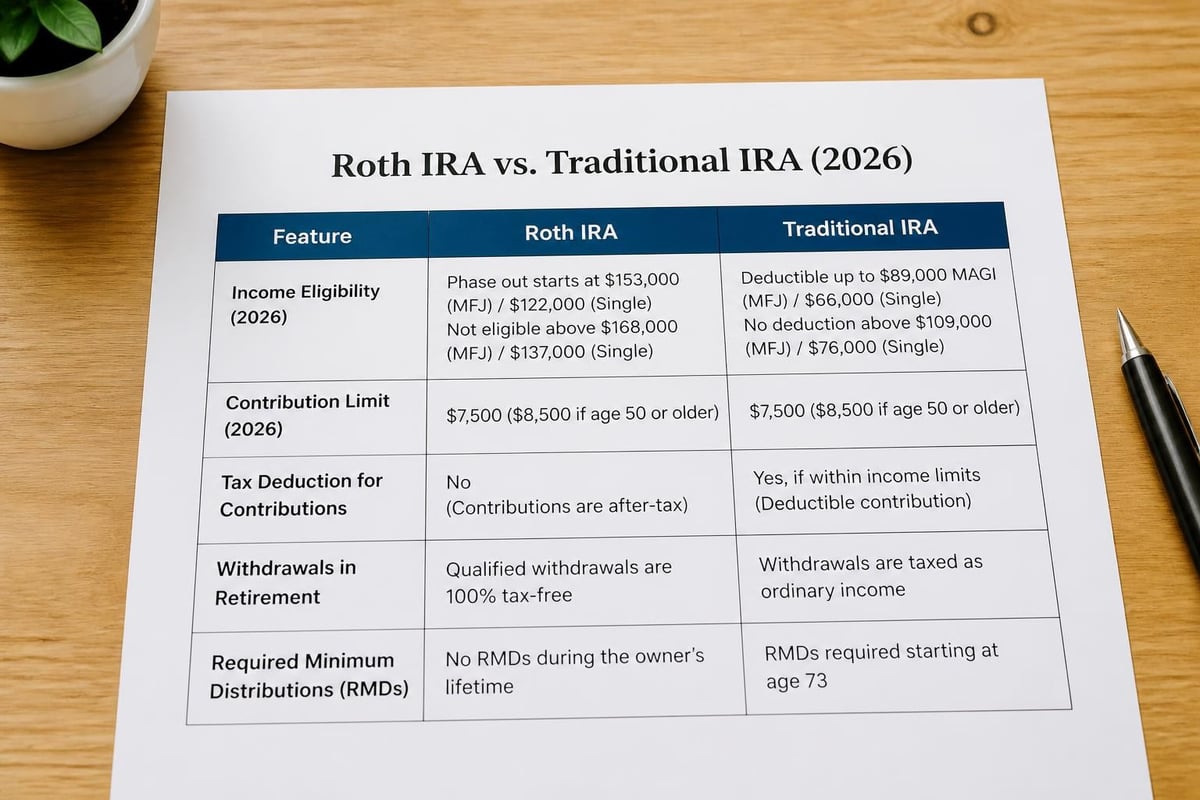

Comparing Roth and Traditional IRA Income Limits

A critical distinction: traditional IRAs have no income limits for contributions. Anyone with earned income can contribute to a traditional IRA regardless of how much they earn. However, the ability to deduct those contributions phases out at certain income levels if you or your spouse participates in an employer retirement plan.

This difference creates strategic opportunities. High earners above the maximum income for Roth IRA eligibility can still benefit from traditional IRA contributions, particularly for backdoor Roth conversion strategies. Understanding traditional IRA basics and contribution rules helps inform comprehensive retirement planning.

| Account Type | Contribution Income Limits | Deduction Income Limits | Tax Treatment |

|---|---|---|---|

| Roth IRA | Yes (phase-out ranges) | N/A | Tax-free growth and withdrawals |

| Traditional IRA | No | Yes (if covered by employer plan) | Tax-deferred growth, taxed at withdrawal |

Estate Planning and Roth IRA Benefits

Beyond the maximum income for Roth IRA considerations, these accounts offer significant estate planning advantages. Roth IRAs are not subject to required minimum distributions during the owner's lifetime, allowing funds to grow tax-free indefinitely.

Beneficiaries inheriting Roth IRAs can enjoy tax-free distributions, making these accounts powerful wealth transfer vehicles. While the SECURE Act changed distribution rules for most non-spouse beneficiaries, requiring accounts to be emptied within ten years, the tax-free nature of distributions remains valuable.

For comprehensive estate planning strategies that incorporate Roth IRAs, professional guidance ensures your legacy planning aligns with current regulations and your family's needs.

Income Projections and Contribution Timing

Your income can fluctuate throughout the year due to bonuses, commissions, self-employment variations, or investment gains. This variability complicates determining whether you'll remain below the maximum income for Roth IRA thresholds.

Conservative strategies include:

- Monitoring year-to-date income quarterly

- Waiting until late in the year to contribute if income is uncertain

- Making smaller monthly contributions that can be adjusted

- Using the extended deadline to contribute after year-end when income is known

Self-employed individuals face additional complexity with variable income and the ability to make deductible retirement plan contributions that affect MAGI. Working with advisors who understand business owner financial planning helps optimize retirement strategies across all available vehicles.

Roth 401(k) Alternatives for High Earners

Employer-sponsored Roth 401(k) plans provide an alternative for those exceeding Roth IRA income limits. These plans have no income restrictions, allowing unlimited earners to make Roth contributions up to the 401(k) limit of $23,000 in 2026 (plus $7,500 catch-up for those 50+).

Roth 401(k) contributions offer similar tax benefits to Roth IRAs, with tax-free growth and qualified distributions. However, they differ in several ways:

- Higher contribution limits

- No income restrictions

- Employer matching (goes into pre-tax account)

- Required minimum distributions during owner's lifetime (though this can be avoided by rolling to a Roth IRA)

- Different creditor protection provisions

Understanding how various retirement account types work together enables comprehensive tax diversification strategies across your retirement portfolio.

Market Volatility and Roth Conversions

Market downturns present strategic opportunities for Roth conversions. When investment values decline, converting traditional retirement accounts to Roth accounts while values are depressed minimizes the tax impact of conversion while capturing future recovery in tax-free accounts.

This timing strategy works independently of the maximum income for Roth IRA contribution limits, since conversions face no income restrictions. Even high earners can convert unlimited amounts, though they must pay taxes on the converted value.

The decision to convert involves analyzing:

- Current versus projected future tax rates

- Available cash to pay conversion taxes

- Time horizon until withdrawal

- Overall tax planning across multiple years

- State tax implications

These complex decisions benefit from personalized financial guidance that considers your complete financial picture.

Young Professionals and Long-Term Roth Benefits

For professionals early in their careers, maximizing Roth IRA contributions before reaching the maximum income for Roth IRA thresholds creates substantial long-term value. Decades of tax-free compounding can generate significant retirement wealth.

A 30-year-old contributing $7,000 annually until age 65, assuming 7% average returns, would accumulate over $930,000 in tax-free savings. The same contributions in a traditional IRA would face ordinary income tax on all distributions.

Young, high-earning professionals in fields like technology, medicine, or law should prioritize Roth contributions while eligible, as their income growth may soon exceed limits. This window of opportunity may not last long.

Income Limit Adjustments and Future Planning

The IRS adjusts the maximum income for Roth IRA eligibility annually based on inflation indices. These increases typically range from $1,000 to $3,000 every few years, though high inflation periods may see larger jumps, as evidenced by the increases between 2024 and 2026.

Staying informed about annual limit changes ensures you don't miss contribution opportunities. If your income has previously exceeded limits but has since decreased, or if limit increases bring you back into eligibility, reviewing your situation each year maintains optimal contribution strategies.

Planning for gradual income increases throughout your career helps anticipate when you might phase out of Roth IRA eligibility, allowing time to implement alternative strategies like backdoor conversions or increased Roth 401(k) contributions.

Documentation and Record Keeping

Maintaining thorough records of Roth IRA contributions, conversions, and basis becomes increasingly important as accounts grow and you approach retirement. The IRS requires Form 8606 for nondeductible traditional IRA contributions and Roth conversions.

Proper documentation prevents double taxation when you eventually take distributions. Since Roth IRA contributions can be withdrawn tax-free and penalty-free at any time (earnings face restrictions), tracking your contribution basis versus earnings ensures accurate tax treatment.

Keep records of:

- Annual contribution amounts and dates

- Tax forms showing income calculations

- Conversion documentation

- Recharacterization forms

- Basis calculations

These records become essential during retirement when you begin taking distributions or if you need to demonstrate compliance during IRS inquiries.

Navigating the maximum income for Roth IRA eligibility and optimizing your retirement savings strategy requires ongoing attention to income changes, tax law updates, and strategic planning opportunities. Understanding these limits enables proactive decision-making that maximizes your tax-advantaged savings potential. Whether you're beginning your career, experiencing income growth, or approaching retirement, Brookwood Investment Group offers personalized guidance to help you navigate Roth IRA strategies, retirement planning, and comprehensive wealth management tailored to your unique financial situation and goals.