Transitioning from accumulation to distribution represents one of the most significant financial shifts you'll experience. When paychecks stop, your investment portfolio must work differently. Rather than focusing solely on growth, your assets need to generate reliable cash flow while preserving capital for decades ahead. Understanding how to structure income-generating investments becomes essential for maintaining your lifestyle without depleting your nest egg prematurely.

Understanding the Income Retirement Landscape

Investing for income in retirement requires a fundamental shift in strategy compared to your working years. During accumulation, you could weather market volatility with time on your side. Now, sequence-of-returns risk becomes a critical concern-poor market performance early in retirement can significantly impact your long-term financial security.

The challenge lies in balancing several competing objectives simultaneously. You need current income to cover living expenses, growth to combat inflation over potentially 30+ years, and principal preservation to avoid running out of money. This three-dimensional puzzle requires careful planning and ongoing adjustment.

The Modern Retirement Income Framework

Traditional retirement wisdom suggested a simple bond-heavy allocation, but today's environment demands more sophistication. With interest rates fluctuating and life expectancies extending, a multi-source income approach typically serves retirees better than any single strategy.

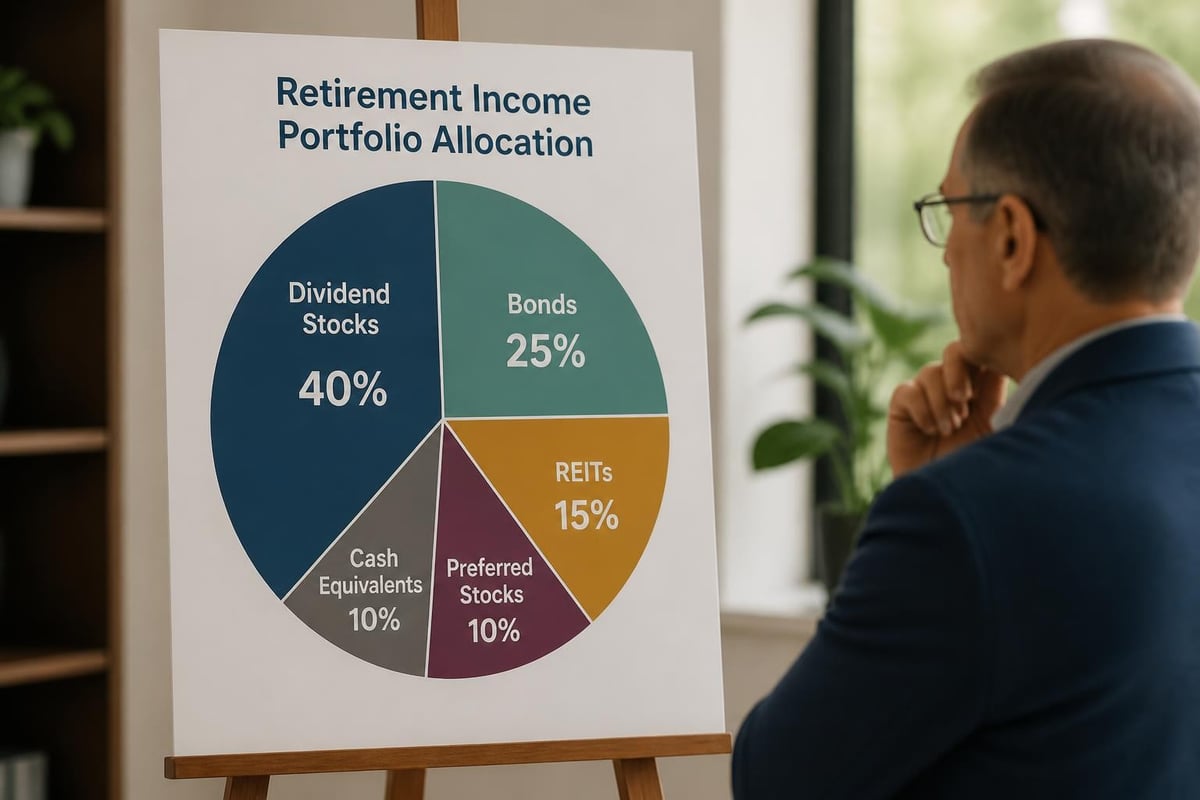

Consider these core income sources:

- Dividend-paying stocks from established companies with consistent payout histories

- Fixed income securities including individual bonds, bond funds, and bond ladders

- Real estate investment trusts (REITs) offering exposure to property income

- Preferred stocks combining equity upside with fixed payment characteristics

- Systematic withdrawal strategies from diversified portfolios

When planning your retirement planning and estate planning strategy, understanding how these elements work together becomes paramount. Each income source carries different tax implications, volatility profiles, and growth potential.

Building Your Income-Generating Portfolio

Constructing a portfolio specifically for retirement income differs significantly from building wealth during your career. The focus shifts from total return to sustainable distributions that won't erode your principal faster than necessary.

Dividend Stock Strategies

Dividend-paying equities form a cornerstone of many income portfolios. Companies that regularly distribute profits to shareholders provide both income and potential appreciation. However, not all dividend stocks deserve equal consideration.

Quality dividend stocks typically demonstrate:

- Consistent payment history spanning multiple market cycles

- Reasonable payout ratios leaving room for dividend growth

- Strong fundamentals supporting sustainable business models

- Diversification across sectors reducing company-specific risks

Many investors overlook dividend growth as a powerful inflation hedge. Companies that increase dividends annually can help your purchasing power keep pace with rising costs. Research from iShares demonstrates how dividend-focused strategies can provide both current income and long-term growth potential.

Fixed Income Allocation Strategies

Bonds and other fixed income securities traditionally anchor retirement portfolios, providing predictable payments and stability during equity market downturns. However, investing for income in retirement through bonds requires understanding various fixed income instruments.

| Fixed Income Type | Primary Benefit | Key Consideration |

|---|---|---|

| Treasury Bonds | Government backing, safety | Lower yields, inflation risk |

| Corporate Bonds | Higher yields than Treasuries | Credit risk varies by issuer |

| Municipal Bonds | Tax-exempt income | State-specific tax implications |

| Bond Funds | Instant diversification | No maturity date, NAV fluctuates |

| Bond Ladders | Predictable maturities | Requires larger capital commitment |

The bond allocation within your portfolio depends heavily on your risk tolerance, income needs, and time horizon. Younger retirees might maintain more equity exposure, while those in their eighties may prioritize principal protection.

Tax-Efficient Income Distribution

Where you hold different income-generating assets matters tremendously for your after-tax returns. Strategic asset location can enhance your spendable income by thousands of dollars annually without changing your investment strategy.

Optimizing Account Placement

Tax-inefficient investments belong in tax-deferred accounts, while tax-advantaged investments work better in taxable accounts. This seemingly simple concept requires careful implementation.

Tax-deferred accounts (Traditional IRA, 401(k)) work best for:

- High-yield bonds generating ordinary income

- REITs with non-qualified dividend distributions

- Actively managed funds with frequent trading

Roth accounts provide ideal homes for:

- Growth stocks with high appreciation potential

- Investments expected to generate significant long-term gains

- Assets you want to pass to heirs tax-free

Taxable brokerage accounts should typically hold:

- Qualified dividend-paying stocks benefiting from preferential rates

- Municipal bonds if you're in high tax brackets

- Tax-managed funds designed for taxable accounts

Understanding tax strategies becomes increasingly important as you coordinate multiple account types. Required minimum distributions (RMDs) from traditional retirement accounts can push you into higher brackets, making Roth conversions and qualified dividend income more valuable.

Withdrawal Strategies and Sustainability

How much can you safely withdraw without running out of money? This question has challenged financial planners and retirees for decades. Investing for income in retirement intersects directly with withdrawal rate decisions.

Beyond the Four Percent Rule

The traditional four percent rule provided a starting point, but it doesn't fit every situation. Vanguard’s research suggests that withdrawal rates should adjust based on market conditions, portfolio composition, and personal circumstances.

Dynamic withdrawal strategies offer more flexibility:

- Percentage-of-portfolio approaches adjust spending based on current portfolio values

- Guardrail strategies allow increases during good markets and cuts during downturns

- Floor-and-upside methods combine guaranteed income sources with variable withdrawals

- Income-only approaches spend only dividends and interest, never touching principal

Each strategy carries different trade-offs between spending stability and portfolio longevity. Working with a fiduciary advisor can help you select and adjust withdrawal strategies appropriate for your specific situation.

Managing Risk in Retirement Income Portfolios

Risk management takes on new dimensions when your portfolio must generate income rather than simply grow. Volatility that was merely annoying during accumulation can become devastating when you're selling assets to fund withdrawals.

Sequence-of-Returns Protection

Selling stocks during market downturns locks in losses and reduces your portfolio's recovery potential. Several strategies help manage this risk:

- Cash reserves covering 1-2 years of expenses prevent forced selling

- Bond tents gradually reducing equity exposure approaching and entering retirement

- Dividend-focused equity providing income without requiring sales

- Bucket strategies segmenting assets by time horizon and purpose

The bucket approach deserves particular attention. By dividing your portfolio into short-term (cash/bonds), medium-term (balanced), and long-term (growth) segments, you can draw from appropriate sources regardless of market conditions.

Diversification Across Income Sources

Concentrating too heavily in any single income-generating investment creates unnecessary vulnerability. Bank of America Private Bank emphasizes how diversification across asset classes and income types provides more stable cash flow.

Consider diversifying across:

- Geographic regions to capture global opportunities

- Sectors and industries avoiding overconcentration

- Company sizes from large-cap stability to mid-cap growth

- Income types mixing dividends, interest, and distributions

This diversification helps ensure that poor performance in one area doesn't devastate your entire income stream. When one sector cuts dividends, others may maintain or increase payouts.

Alternative Income-Generating Investments

Beyond traditional stocks and bonds, several investment vehicles can enhance retirement income. Understanding these options helps you construct a more robust portfolio aligned with your specific goals.

Real Estate Investment Trusts (REITs)

REITs offer exposure to real estate income without the headaches of property management. By law, REITs must distribute at least 90 percent of taxable income to shareholders, often resulting in attractive yields.

Different REIT categories serve different purposes:

| REIT Type | Focus Area | Income Characteristics |

|---|---|---|

| Equity REITs | Own properties, collect rent | Higher yields, property appreciation |

| Mortgage REITs | Finance real estate debt | Very high yields, interest rate sensitive |

| Hybrid REITs | Both ownership and financing | Balanced approach to income and risk |

REITs add diversification beyond stocks and bonds while providing inflation protection through rising rents and property values.

Preferred Stocks and Convertibles

Preferred stocks sit between common stocks and bonds in the capital structure. They typically pay fixed dividends with priority over common stockholders but offer less growth potential.

Advantages of preferreds include:

- Higher yields than common stocks

- More stable prices than common stocks

- Potential tax advantages on qualified dividends

Disadvantages to consider:

- Interest rate sensitivity similar to bonds

- Limited upside participation

- Lower priority than bonds in bankruptcy

Convertible bonds offer another hybrid option, providing bond-like income with equity upside potential if the underlying stock appreciates significantly.

Annuities and Guaranteed Income

While not technically investments, annuities deserve consideration in any comprehensive discussion about investing for income in retirement. These insurance products can provide guaranteed lifetime income, addressing longevity risk directly.

Types of Income Annuities

Guaranteed income options range from immediate annuities starting payments quickly to deferred income annuities beginning later. Each serves different purposes within a retirement income plan.

Single Premium Immediate Annuities (SPIAs) convert a lump sum into lifetime income immediately. They work well for covering essential expenses with predictable payments.

Deferred Income Annuities (DIAs) start payments at a future date, providing higher income rates due to the deferral period. These can serve as "longevity insurance" protecting against outliving other assets.

Variable Annuities with Living Benefits combine investment features with income guarantees, though fees can significantly reduce returns.

Annuities complement rather than replace investment portfolios. By covering fixed expenses with guaranteed income, you gain flexibility to take more calculated risks with remaining assets.

Healthcare Costs and Income Planning

Medical expenses represent one of the largest and most unpredictable retirement costs. Investing for income in retirement must account for healthcare inflation significantly exceeding general inflation.

Planning for Medical Expenses

Medicare covers many but not all healthcare costs. Premiums, deductibles, copayments, and uncovered services can consume substantial portions of retirement income.

Planning considerations include:

- Medicare Part B and Part D premiums tied to income levels through IRMAA

- Supplemental insurance covering Medicare gaps

- Long-term care expenses potentially requiring separate insurance or dedicated assets

- Prescription costs varying widely based on specific needs

Maintaining some growth-oriented investments helps ensure your portfolio can fund healthcare expenses that may accelerate significantly in your later years. Financial planning services often include healthcare cost projections customized to your specific health situation and family history.

Adapting Your Strategy Over Time

Your retirement income strategy shouldn't remain static for 30+ years. Market conditions change, personal circumstances evolve, and tax laws shift. Regular reviews ensure your portfolio continues meeting your needs.

Life-Stage Adjustments

Early retirement typically allows for more aggressive positioning, while advanced age suggests greater conservatism. However, these aren't rigid rules.

Years 60-70 often emphasize:

- Transitioning from accumulation to income orientation

- Building cash reserves for sequence-of-returns protection

- Optimizing Social Security claiming strategies

- Converting traditional IRAs to Roth accounts during lower-income years

Years 70-80 frequently focus on:

- Managing required minimum distributions efficiently

- Adjusting withdrawal rates based on portfolio performance

- Rebalancing to maintain appropriate risk levels

- Updating estate plans and beneficiary designations

Beyond age 80 priorities often shift toward:

- Simplifying investment holdings for easier management

- Increasing liquid assets for potential care needs

- Finalizing legacy and charitable giving plans

- Ensuring heirs understand financial arrangements

Behavioral Considerations for Income Investors

Emotional discipline often determines success more than investment selection. When markets decline or dividends get cut, maintaining your strategic course becomes challenging.

Common Psychological Traps

Chasing yield ranks among the most dangerous behavioral mistakes. Unusually high yields typically signal elevated risk. Companies paying unsustainably high dividends often cut them during downturns, leaving investors with both income loss and capital depreciation.

Panic selling during market volatility crystallizes losses and disrupts long-term income plans. Remember that short-term market movements rarely justify major portfolio changes.

Recency bias leads investors to overweight recent performance. Just because growth stocks outperformed doesn't mean they will continue doing so, and vice versa.

Working with advisors who understand these behavioral tendencies can help you maintain discipline when emotions run high. The personalized guidance provided by fiduciary advisors includes behavioral coaching alongside investment management.

Coordinating Income Sources

Most retirees receive income from multiple sources beyond their investment portfolios. Social Security, pensions, rental properties, and part-time work all contribute to your total cash flow picture.

Optimizing the Income Mix

Charles Schwab’s guidance emphasizes coordinating various income streams to minimize taxes and maximize sustainability. For example, delaying Social Security while living on portfolio withdrawals can increase lifetime benefits while reducing required portfolio size.

Strategic coordination involves:

- Timing Social Security to maximize survivor benefits and cost-of-living adjustments

- Managing pension elections between lump sums and annuitized payments

- Coordinating spousal benefits across different income sources

- Sequencing account withdrawals to optimize tax efficiency across decades

This coordination becomes increasingly complex when multiple income sources interact with progressive tax brackets, Medicare premium calculations, and state tax considerations.

Environmental Factors Affecting Income Strategies

External factors beyond your control significantly impact retirement income success. Understanding these forces helps you adapt appropriately.

Interest Rate Environments

Low interest rates compress bond yields and push investors toward riskier alternatives. Rising rates increase bond income but decrease bond prices, creating losses for those needing to sell before maturity.

Strategies for different rate environments include:

Low-rate periods:

- Emphasizing dividend growth over current yield

- Shortening bond duration to reduce interest rate risk

- Considering alternative income sources like REITs

- Maintaining flexibility for opportunities when rates rise

Rising-rate periods:

- Building bond ladders locking in higher rates progressively

- Accepting temporary bond portfolio declines as the price of higher future income

- Avoiding long-duration bonds vulnerable to price decreases

- Reassessing high-dividend stocks that may underperform

Inflation's Impact on Income

Inflation steadily erodes purchasing power. An income stream that seems adequate today may fall short in 15 years if it doesn't grow. U.S. Bank research highlights how different income investments respond to inflation pressures.

Some investments naturally provide inflation protection:

- Dividend growth stocks from companies that raise payouts

- Treasury Inflation-Protected Securities (TIPS) adjusting principal with CPI

- Real estate providing rental income growth

- Commodities and natural resource investments

Balancing current income needs against inflation protection requires ongoing attention and periodic rebalancing.

Investing for income in retirement demands a comprehensive approach balancing current cash flow needs, long-term sustainability, tax efficiency, and risk management. Your strategy should evolve as markets change and your personal circumstances shift over potentially three decades or more. Brookwood Investment Group LLC provides personalized, fiduciary guidance to help you navigate these complexities, designing income strategies tailored to your unique goals and circumstances. Schedule a consultation to explore how a customized retirement income plan can support your financial security and lifestyle objectives.