Retirement planning involves navigating complex regulations, and understanding your 401k minimum distribution requirements is essential for maintaining compliance while optimizing your financial strategy. As you approach retirement age, the IRS mandates that you begin withdrawing specific amounts from your tax-advantaged retirement accounts, creating both tax implications and planning opportunities. These required minimum distributions (RMDs) affect millions of Americans with substantial retirement savings, and proper planning can help you manage your tax burden while preserving wealth for future needs.

Understanding 401k Minimum Distribution Requirements

The 401k minimum distribution represents the smallest amount the IRS requires you to withdraw annually from your retirement accounts once you reach a specific age. This requirement applies to traditional 401(k) plans, traditional IRAs, SEP IRAs, SIMPLE IRAs, and other tax-deferred retirement vehicles.

The age when you must begin taking distributions has changed recently due to legislative updates. Under the SECURE 2.0 Act, individuals who turn 73 in 2026 must start their RMDs by April 1 of the year following the year they reach age 73. This deadline represents your "required beginning date."

Key Age Thresholds and Timeline

The RMD starting age depends on your birth year:

- Born before 1951: RMDs began at age 70½

- Born 1951-1959: RMDs begin at age 73

- Born 1960 or later: RMDs begin at age 75

For individuals still working at age 73, the IRS allows an exception if you don't own more than 5% of the company sponsoring your 401(k) plan. This "still-working exception" permits you to delay RMDs from that specific employer's plan until you retire.

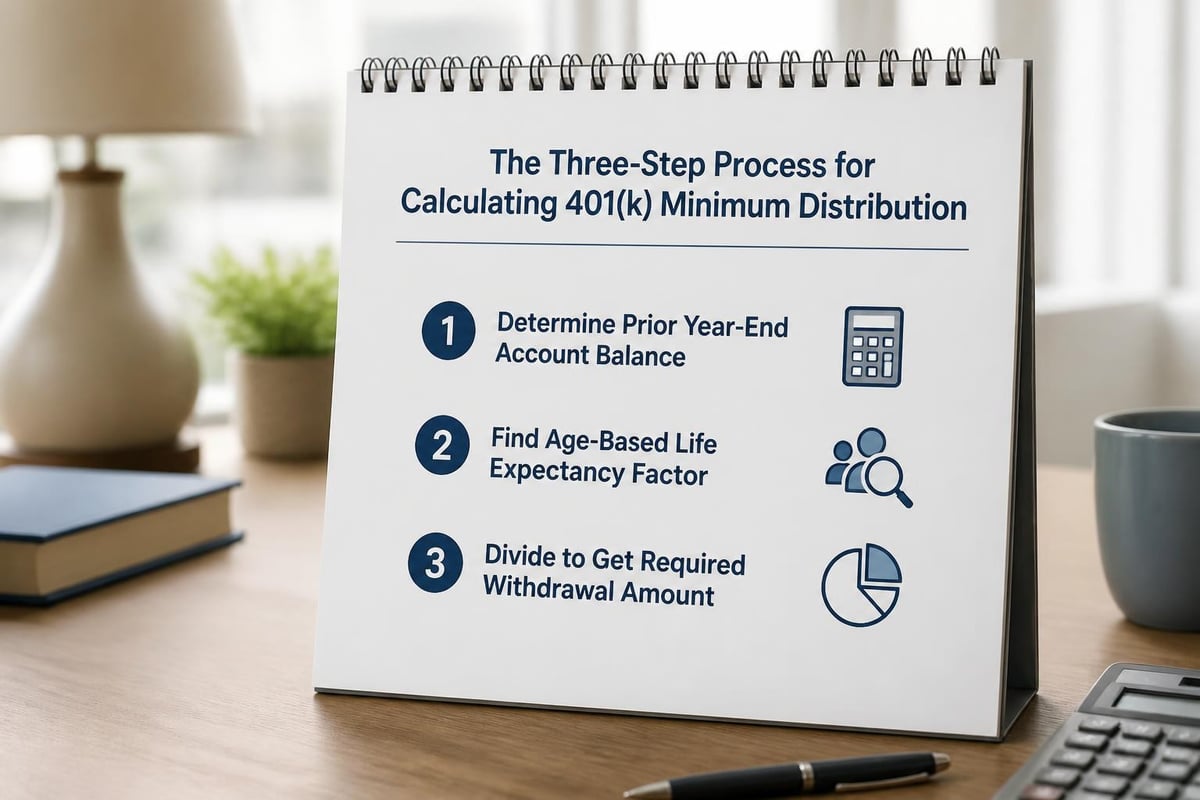

Calculating Your 401k Minimum Distribution

Understanding how to calculate your required withdrawal ensures compliance and helps with tax planning. The calculation involves two primary components: your account balance and your life expectancy factor.

The Basic Formula

| Component | Description |

|---|---|

| Prior Year-End Balance | Total account value as of December 31 of the previous year |

| Life Expectancy Factor | IRS-published number from Uniform Lifetime Table |

| Calculation Method | Divide balance by life expectancy factor |

To calculate your 401k minimum distribution, divide your account balance from December 31 of the previous year by the distribution period from the IRS Uniform Lifetime Table. For example, if you're 75 years old in 2026 with a December 31, 2025 balance of $500,000, and your distribution period is 24.6, your RMD would be approximately $20,325.

Multiple Account Considerations

Many individuals hold retirement savings across several accounts. Here's how aggregation works:

- Traditional IRAs: Calculate RMDs separately for each IRA, but you may withdraw the total from one or more IRAs

- 401(k) accounts: Calculate and withdraw separately from each 401(k) plan

- 403(b) accounts: Generally must calculate and withdraw separately, though some aggregation is permitted

The calculation methods for RMDs can become complex when you have inherited accounts or multiple retirement vehicles, making professional guidance valuable.

Tax Implications of Required Minimum Distributions

Your 401k minimum distribution counts as ordinary income for federal tax purposes. This classification can significantly impact your overall tax situation, potentially pushing you into higher tax brackets and affecting Medicare premiums.

Understanding the Tax Impact

Every dollar you withdraw from your traditional 401(k) as an RMD faces taxation at your marginal income tax rate. Unlike capital gains from investment accounts, these distributions don't receive preferential tax treatment.

Consider these tax-related consequences:

- Increased adjusted gross income (AGI)

- Higher Medicare Part B and Part D premiums through Income-Related Monthly Adjustment Amount (IRMAA)

- Potential taxation of Social Security benefits

- Reduced eligibility for certain tax deductions and credits

Working with advisors who specialize in retirement planning and estate planning can help you develop strategies to minimize these impacts through coordinated withdrawal planning.

Penalty for Missing RMDs

The consequences of failing to take your required distribution are severe. The IRS imposes a 25% excise tax on the amount you should have withdrawn but didn't. If you correct the error promptly (within two years), the penalty may be reduced to 10%.

This substantial penalty underscores the importance of tracking RMD deadlines and tax mistakes to avoid throughout your retirement years.

Strategic Planning for 401k Minimum Distributions

Proactive planning allows you to manage your 401k minimum distribution requirements while optimizing your overall financial situation. Several strategies can help reduce tax burdens and preserve wealth.

QCD Strategy: Qualified Charitable Distributions

If you're charitably inclined and at least 70½ years old, qualified charitable distributions (QCDs) offer significant advantages. You can donate up to $105,000 annually (for 2026, adjusted for inflation) directly from your IRA to qualified charities.

Benefits of QCDs include:

- Satisfying your RMD requirement

- Excluding the distribution from taxable income

- Avoiding the increase in AGI that affects other tax calculations

- Supporting causes you care about efficiently

Note that QCDs only apply to IRAs, not 401(k) plans. However, you can roll over 401(k) funds to an IRA to take advantage of this strategy.

Roth Conversion Considerations

Converting traditional 401(k) or IRA assets to Roth accounts before reaching RMD age can provide long-term benefits. While you'll pay taxes on the converted amount, Roth IRAs don't have RMD requirements during the original owner's lifetime.

| Strategy Aspect | Traditional 401(k)/IRA | Roth IRA |

|---|---|---|

| RMD Requirement | Yes, starting at 73-75 | No, during owner's lifetime |

| Tax on Withdrawals | Ordinary income | Tax-free if qualified |

| Tax on Conversion | N/A | Ordinary income in conversion year |

| Estate Planning | RMDs required for heirs | More favorable for beneficiaries |

This approach works particularly well during lower-income years or when you anticipate being in higher tax brackets during retirement. Understanding how taxes could affect your retirement accounts helps inform these decisions.

Asset Location and Withdrawal Sequencing

Strategic withdrawal sequencing involves determining which accounts to tap first based on tax efficiency and your overall financial plan. Generally, this means:

- Required minimum distributions (you have no choice)

- Taxable investment accounts (flexibility and potentially lower tax rates)

- Tax-deferred accounts beyond RMDs (managing bracket exposure)

- Roth accounts (preserving tax-free growth)

The optimal sequence depends on your specific situation, including income sources, tax bracket, legacy goals, and spending needs. Professional advisors offering personalized retirement planning services can develop customized withdrawal strategies aligned with your objectives.

Special Situations and Exceptions

Certain circumstances create unique considerations for your 401k minimum distribution requirements. Understanding these exceptions helps you navigate complex scenarios.

Still-Working Exception

If you continue working past age 73 and participate in your current employer's 401(k) plan, you may defer RMDs from that specific plan. However, this exception only applies if you own 5% or less of the company.

Key points about the still-working exception:

- Only applies to your current employer's plan

- Must still take RMDs from other retirement accounts

- Doesn't extend to previous employers' 401(k) plans

- Ends when you retire

Inherited Retirement Accounts

Beneficiaries of inherited 401(k) plans face different rules depending on their relationship to the deceased and when the account owner died. The SECURE Act substantially changed these rules for accounts inherited after December 31, 2019.

Non-spouse beneficiaries generally must:

- Deplete the account within 10 years (with some exceptions)

- Take annual RMDs if the original owner had already begun distributions

- Follow special rules if you're a minor child, disabled, chronically ill, or not more than 10 years younger than the deceased

Spouse beneficiaries have more options, including treating the account as their own or taking distributions based on their life expectancy.

First-Year RMD Grace Period

For your first RMD only, you have until April 1 of the year following the year you turn 73. However, this delay means taking two distributions in one year (the first-year RMD by April 1 and the current year's RMD by December 31), potentially creating a larger tax burden.

Most tax professionals recommend taking your first distribution in the year you turn 73 to avoid this double-taxation year.

Integrating RMD Planning Into Your Overall Strategy

Your 401k minimum distribution shouldn't exist in isolation from your comprehensive financial plan. Effective integration considers multiple interconnected factors that impact your retirement security.

Coordination With Social Security

The timing of Social Security benefits affects your overall tax picture when combined with RMDs. For some individuals, delaying Social Security until age 70 while managing RMDs strategically can optimize lifetime benefits.

Consider how your customized retirement plan addresses the interaction between these income sources, including provisional income calculations that determine Social Security taxation.

Estate Planning Considerations

RMDs impact your estate planning by reducing account balances available to heirs. However, strategic planning can help preserve wealth across generations.

Estate planning approaches include:

- Life insurance funding using RMD proceeds

- Charitable remainder trusts for tax-efficient giving

- Roth conversions to provide tax-free inheritance

- Gifting strategies using RMD income

Understanding estate planning advantages helps you make informed decisions about legacy goals while meeting distribution requirements.

Healthcare and Medicare Planning

Your 401k minimum distribution increases your modified adjusted gross income (MAGI), which determines Medicare premium surcharges. In 2026, IRMAA thresholds create substantial premium increases at specific income levels.

Strategic management of RMDs, combined with other income sources, can help you avoid crossing IRMAA thresholds or minimize time spent in higher premium brackets. This requires forward-looking planning that considers tax strategies alongside retirement income.

Investment Management During RMD Years

Once you begin taking your 401k minimum distribution, your investment strategy should evolve to support systematic withdrawals while managing longevity risk and market volatility.

Portfolio Positioning

Your asset allocation should reflect several factors:

- Time horizon (potentially 20-30+ years in retirement)

- Risk tolerance and capacity

- Income needs beyond RMDs

- Legacy objectives

- Market conditions and valuations

Many retirees maintain equity exposure to support long-term purchasing power, while positioning fixed-income and cash equivalents to fund near-term distributions without forced selling during market downturns.

Withdrawal Timing and Market Volatility

Taking your required distribution during market downturns forces you to sell more shares to meet dollar requirements, potentially depleting your portfolio faster. Strategies to manage this sequence-of-returns risk include:

- Maintaining adequate cash reserves (12-24 months of distributions)

- Creating a "bucket" strategy with different time horizons

- Rebalancing to fund withdrawals from appreciated assets

- Adjusting discretionary spending during severe downturns

Tax-Loss Harvesting Opportunities

While you can't avoid the RMD itself, tax-loss harvesting in taxable accounts can offset other capital gains and reduce your overall tax burden. This coordinated approach across account types demonstrates the value of comprehensive investment management during retirement.

Common Mistakes and How to Avoid Them

Understanding frequent errors related to 401k minimum distribution requirements helps you maintain compliance and optimize your strategy.

Calculation Errors

Using incorrect account balances or outdated life expectancy tables leads to under-withdrawals that trigger penalties. Always use the December 31 balance from the previous year and consult current IRS tables. For 2026, ensure you're using the updated tables that reflect recent regulatory changes.

Missing Aggregation Rules

Failing to understand which accounts can be aggregated for RMD purposes creates confusion. Remember that 401(k) plans require separate calculations and withdrawals from each plan, while IRAs allow aggregation.

Ignoring Beneficiary Designations

Outdated or missing beneficiary designations complicate estate settlement and may create unintended tax consequences for heirs. Review designations regularly, especially after major life events.

Waiting Until December

Last-minute RMD withdrawals in December create processing delays and potential missed deadlines. Establish a systematic approach, whether taking monthly distributions or scheduling withdrawals earlier in the year.

Resources like this overview of common tax mistakes highlight additional pitfalls to avoid as you navigate distribution requirements.

Planning for Large Account Balances

Individuals with substantial retirement savings face unique challenges with their 401k minimum distribution. When you've saved significant amounts, the RMDs can be substantial, creating considerable tax burdens.

High-Income Strategies

For accounts exceeding $1 million, annual RMDs can push you into the highest tax brackets and trigger maximum IRMAA surcharges. Advanced strategies may include:

- Multi-year Roth conversion planning before RMDs begin

- Charitable remainder trusts for tax-deferred giving

- Donor-advised funds to manage charitable deductions

- Strategic gifting to family members in lower brackets

Professional Guidance Value

The complexity of managing large distributions, coordinating multiple income sources, and optimizing tax efficiency across decades of retirement makes professional advice particularly valuable. Working with fiduciary advisors ensures recommendations align with your best interests rather than product sales.

Technology and RMD Tracking

Modern tools help you monitor your 401k minimum distribution obligations across multiple accounts. Many custodians provide automatic RMD calculations and can establish systematic distributions to ensure compliance.

Technology advantages include:

- Automatic calculation updates reflecting regulatory changes

- Reminder systems for distribution deadlines

- Tax reporting integration for year-end documentation

- Portfolio modeling showing long-term RMD projections

However, technology complements rather than replaces comprehensive planning that considers your unique circumstances, goals, and values.

Regulatory Changes and Future Considerations

The rules governing 401k minimum distribution continue evolving through legislation. The SECURE Act of 2019 and SECURE 2.0 Act of 2022 substantially modified RMD requirements, and future changes remain possible.

Staying informed about regulatory updates ensures your strategy remains compliant and optimized. Professional advisors monitor these changes and help you adapt your plan accordingly, whether through virtual advisory services or traditional relationships.

Understanding current requirements while maintaining flexibility for future adjustments positions you to navigate an evolving regulatory landscape confidently.

Managing your 401k minimum distribution effectively requires understanding complex rules, coordinating multiple financial elements, and adapting strategies as regulations and personal circumstances change. Whether you're approaching your first RMD or optimizing distributions from substantial retirement savings, professional guidance helps you navigate tax implications while preserving wealth for your goals. Brookwood Investment Group offers personalized, fiduciary guidance tailored to your unique retirement situation, helping you develop tax-efficient strategies that align with your lifestyle and legacy objectives.