Navigating the complexities of accessing your retirement savings requires careful consideration of rules, regulations, and long-term financial implications. A 401(k) withdrawal represents a significant financial decision that can impact your retirement security, tax liability, and overall wealth accumulation strategy. Whether you're facing an unexpected expense, approaching retirement age, or simply exploring your options, understanding the various withdrawal methods, penalties, and strategic considerations becomes essential for maintaining financial stability while preserving your retirement nest egg.

Understanding 401(k) Withdrawal Fundamentals

The basic framework governing 401(k) withdrawals centers on age-based regulations established by the Internal Revenue Service. When you contribute to a traditional 401(k), you receive tax-deferred growth benefits, but the government expects to collect taxes when you eventually access these funds.

Standard withdrawal rules include:

- Penalty-free withdrawals beginning at age 59½

- Required minimum distributions starting at age 73 (as of 2026)

- Early withdrawal penalties of 10% plus ordinary income tax before age 59½

- Specific exceptions for hardship situations and qualifying events

The distinction between traditional and Roth 401(k) accounts significantly affects withdrawal taxation. Traditional accounts face ordinary income tax on the entire withdrawal amount, while Roth accounts allow tax-free withdrawals of contributions and earnings after age 59½, provided the account has been open for at least five years.

Early Withdrawal Penalties and Exceptions

Accessing your 401(k) before reaching age 59½ typically triggers substantial financial consequences. The early withdrawal penalties combine federal income tax with an additional 10% penalty tax, potentially reducing your distribution by 30% to 40% depending on your tax bracket.

However, specific circumstances permit penalty-free early withdrawals:

- Separation from service after age 55 (age 50 for public safety employees)

- Disability as defined by IRS guidelines

- Substantially equal periodic payments under IRS Rule 72(t)

- Qualified domestic relations orders in divorce proceedings

- Medical expenses exceeding 7.5% of adjusted gross income

- IRS levy on the retirement account

Understanding these exceptions helps individuals evaluate whether their situation justifies early access. Financial planning services can provide personalized guidance on navigating these complex regulations while minimizing tax consequences.

Tax Implications of Different Withdrawal Strategies

The tax treatment of your 401(k) withdrawal depends on multiple factors including account type, withdrawal timing, and your overall income picture. Traditional 401(k) distributions count as ordinary income in the year you receive them, potentially pushing you into higher tax brackets and affecting other income-based benefits.

Calculating Your Tax Burden

| Withdrawal Amount | Tax Bracket (Single) | Federal Tax | Penalty (if under 59½) | Net Distribution |

|---|---|---|---|---|

| $20,000 | 22% | $4,400 | $2,000 | $13,600 |

| $50,000 | 24% | $12,000 | $5,000 | $33,000 |

| $100,000 | 32% | $32,000 | $10,000 | $58,000 |

These calculations demonstrate the significant erosion of retirement savings through premature withdrawals. Understanding how 401(k) withdrawals are taxed becomes crucial for making informed decisions about accessing retirement funds.

State income taxes add another layer of complexity. Most states tax 401(k) withdrawals as ordinary income, though some offer preferential treatment for retirement distributions or exempt them entirely. Coordinating federal and state tax planning requires careful analysis of your complete financial situation.

Withholding Considerations

When initiating a 401(k) withdrawal, you'll face mandatory withholding requirements. Plan administrators typically withhold 20% for federal taxes on eligible rollover distributions, though you can adjust withholding for periodic payments. This upfront withholding creates immediate cash flow implications that require planning.

You might owe additional taxes when filing your return if withholding proves insufficient. Alternatively, excessive withholding creates an interest-free loan to the government. Strategic withholding management balances these competing considerations while ensuring compliance with tax obligations.

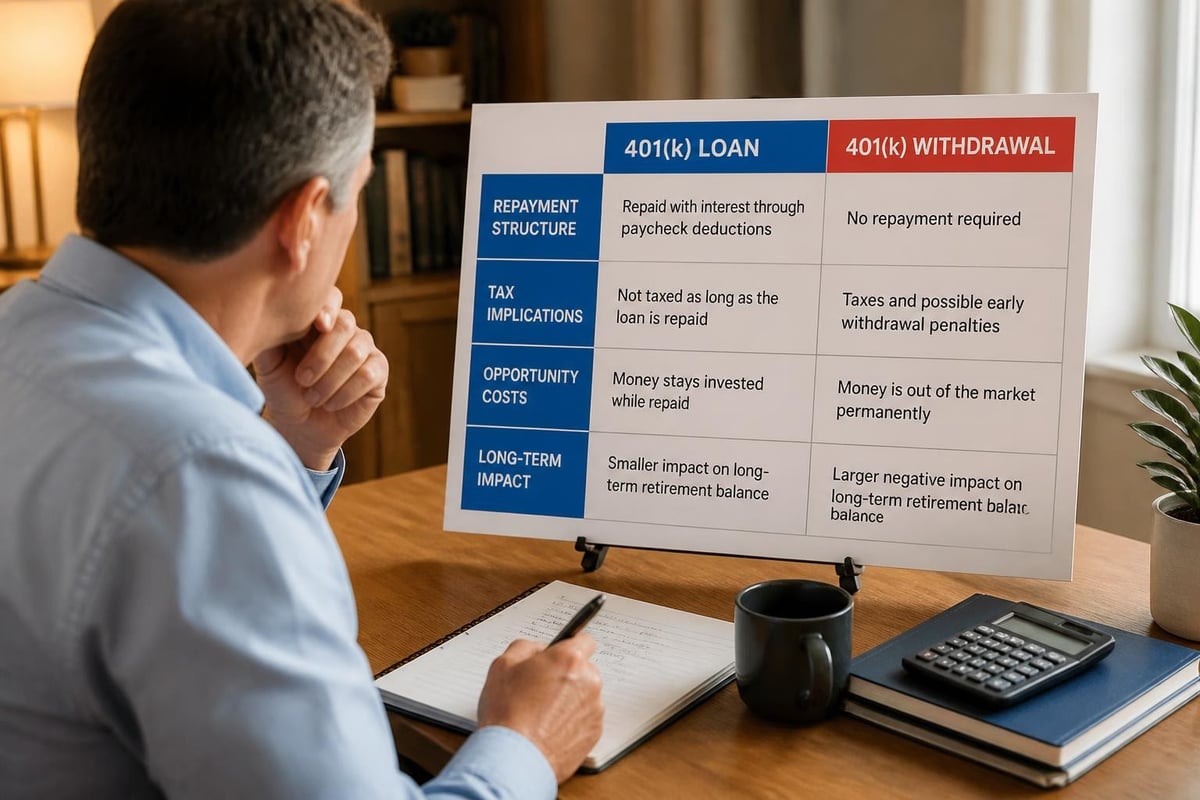

Hardship Withdrawals and Loans

Not all 401(k) access requires permanent withdrawals. Many plans offer hardship withdrawal provisions and loan options that provide temporary access to funds while preserving long-term retirement savings potential.

Qualifying hardship reasons include:

- Medical expenses for you, your spouse, or dependents

- Costs related to purchasing a primary residence

- Tuition and educational expenses

- Prevention of eviction or foreclosure

- Funeral expenses

- Repair of casualty damage to primary residence

Hardship withdrawals require demonstrating immediate and heavy financial need, plus exhausting other available resources. You can only withdraw the amount necessary to satisfy the need, including taxes and penalties. These distributions remain subject to ordinary income tax and the 10% early withdrawal penalty unless an exception applies.

401(k) Loan Alternative

Borrowing from your 401(k) offers advantages over hardship withdrawals in many situations. You can typically borrow up to 50% of your vested balance or $50,000, whichever is less. Loan repayments go back into your account with interest, essentially paying yourself rather than losing the funds permanently.

However, loans carry significant risks. If you separate from your employer, the outstanding balance typically becomes due within 60 to 90 days. Failure to repay triggers taxation and penalties as if you took a direct withdrawal. Additionally, you lose investment growth potential on borrowed funds during the repayment period.

Strategic Withdrawal Planning for Retirement

Approaching retirement age transforms 401(k) withdrawal planning from crisis management to strategic income optimization. The sequence and timing of withdrawals significantly impact your tax liability, investment longevity, and overall retirement security.

Required minimum distributions begin at age 73 for individuals born in 1951 or later. The RMD amount calculates based on your account balance and IRS life expectancy tables. Failing to take required distributions triggers penalties equal to 25% of the amount you should have withdrawn.

Withdrawal Sequencing Strategies

Tax-efficient withdrawal sequencing considers multiple account types and their distinct tax treatments:

- Taxable investment accounts first to allow tax-advantaged accounts continued growth

- Tax-deferred accounts (traditional 401(k), traditional IRA) to manage taxable income

- Tax-free accounts (Roth 401(k), Roth IRA) last to maximize tax-free growth

This general framework requires customization based on individual circumstances. Someone with substantial traditional 401(k) balances might prioritize earlier distributions to avoid massive RMDs pushing them into higher tax brackets. Retirement planning strategies should align withdrawal timing with Social Security claiming decisions, healthcare costs, and legacy planning objectives.

| Age Range | Primary Consideration | Strategic Approach |

|---|---|---|

| 59½-65 | Bridge to Medicare | Manage health insurance costs |

| 65-70 | Social Security timing | Balance distributions with benefits |

| 70-73 | Pre-RMD positioning | Reduce future RMD burden |

| 73+ | RMD compliance | Tax-efficient distribution management |

Roth Conversion Opportunities

Strategic 401(k) withdrawals can facilitate Roth conversions during low-income years. Converting traditional 401(k) funds to Roth accounts triggers immediate taxation but creates tax-free growth and withdrawal opportunities for the future. This strategy works particularly well during early retirement years before RMDs and Social Security begin.

The analysis requires projecting future tax rates, income needs, and legacy objectives. Converting too aggressively increases current tax liability unnecessarily, while converting too conservatively leaves you vulnerable to higher future tax rates and substantial RMDs.

Impact on Long-Term Retirement Security

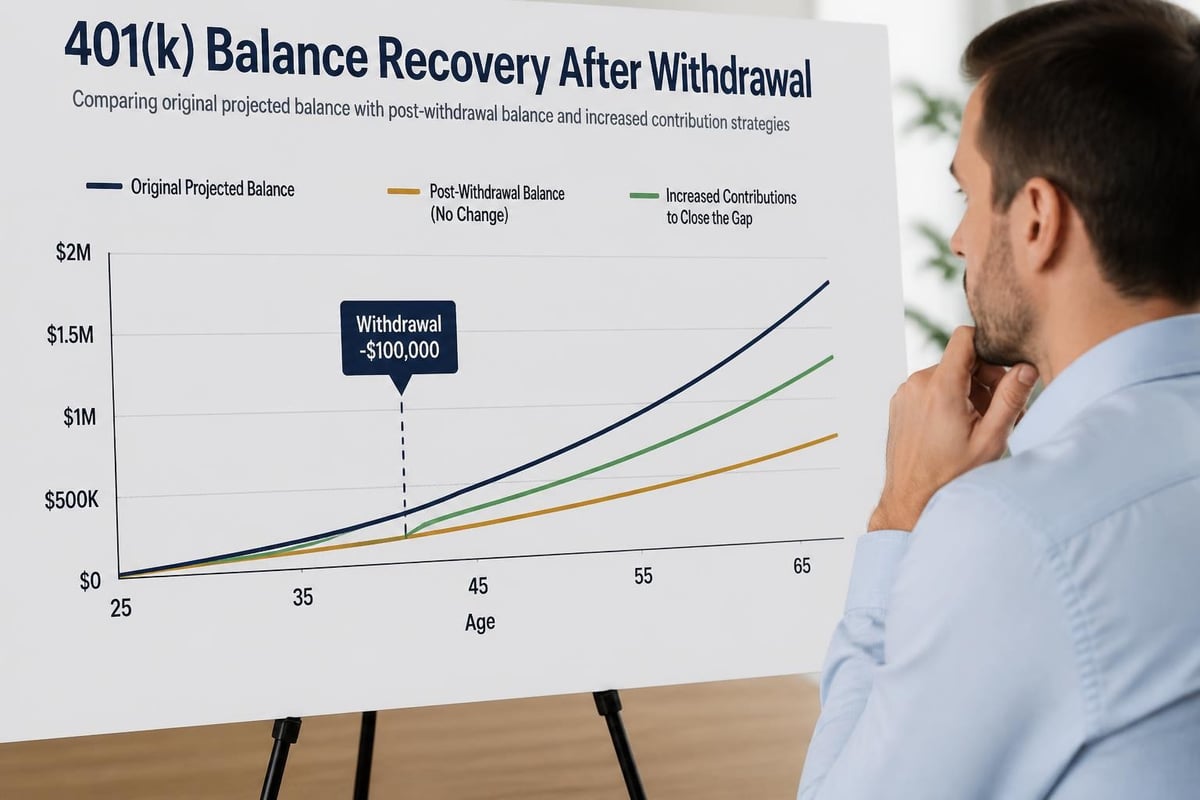

Every dollar withdrawn from your 401(k) represents not just the immediate distribution but also the future growth potential lost. The long-term impacts of early 401(k) withdrawals compound over time, potentially derailing retirement readiness.

Consider a 35-year-old withdrawing $25,000 from their 401(k). After taxes and penalties, they receive approximately $16,250. However, the true cost extends far beyond this immediate reduction. Assuming 7% annual returns, that $25,000 would grow to approximately $190,000 by age 65. The opportunity cost dwarfs the short-term benefit.

Rebuilding After Withdrawal

If circumstances necessitate a 401(k) withdrawal, developing a recovery plan becomes essential. This includes:

- Maximizing future contributions to catch up on lost savings

- Capturing employer matches to accelerate rebuilding

- Adjusting retirement timeline if necessary to compensate for reduced balances

- Increasing savings rate in other accounts to diversify retirement resources

Recovery feasibility depends on age, income, and time until retirement. Someone in their 30s or 40s has more opportunity to recover from a withdrawal setback than someone in their 50s approaching retirement.

Coordinating With Overall Financial Planning

401(k) withdrawal decisions exist within a broader financial context requiring comprehensive analysis. Your withdrawal strategy should integrate with estate planning, tax planning, healthcare planning, and overall wealth management objectives.

Emergency funds provide crucial protection against the need for retirement account withdrawals. Maintaining three to six months of expenses in accessible savings creates a buffer for unexpected costs without jeopardizing retirement security. This fundamental financial planning principle prevents short-term crises from creating long-term consequences.

Professional Guidance Value

The complexity of 401(k) withdrawal regulations, tax implications, and strategic considerations makes professional guidance valuable for most individuals. Financial advisors can model different withdrawal scenarios, project tax consequences, and identify opportunities you might otherwise miss.

Fiduciary advisors prioritize your interests when developing withdrawal recommendations. They consider your complete financial picture, including other retirement accounts, Social Security benefits, pension income, and legacy objectives. This holistic approach optimizes decisions across your entire financial life rather than focusing narrowly on a single account or transaction.

Key planning areas requiring coordination:

- Social Security claiming strategies and timing

- Medicare enrollment and healthcare cost management

- Estate planning and beneficiary designations

- Tax bracket management and deduction optimization

- Investment allocation across account types

Alternative Strategies Before Withdrawing

Before proceeding with a 401(k) withdrawal, exhausting alternative funding sources helps preserve retirement security. Several options may provide needed funds without triggering the tax consequences and long-term impacts of retirement account distributions.

Home equity lines of credit offer access to funds secured by your property. Interest rates typically remain lower than credit cards, and interest may be tax-deductible if used for home improvements. However, this strategy creates debt obligations and puts your home at risk if you cannot make payments.

Personal loans from banks or credit unions provide another option, particularly for those with strong credit profiles. While interest rates vary based on creditworthiness, personal loans avoid the opportunity cost of lost investment growth and maintain retirement account balances for their intended purpose.

Family loans or gifts represent another possibility in some situations. Structuring these arrangements properly with clear terms and documentation protects relationships while providing needed funds. However, this approach requires careful consideration of family dynamics and potential tax implications for large transfers.

Selling Investments in Taxable Accounts

Liquidating investments in regular brokerage accounts often provides a more tax-efficient funding source than 401(k) withdrawals. Long-term capital gains rates typically fall below ordinary income tax rates, and you avoid the additional 10% early withdrawal penalty.

This strategy works particularly well when you have appreciated securities held for more than one year. The lower tax treatment preserves more of your assets while leaving retirement accounts intact for continued tax-advantaged growth.

Regulatory Compliance and Documentation

Proper documentation and compliance with IRS regulations protects you from unexpected tax consequences or penalties. Your plan administrator provides required forms for withdrawal requests, but understanding the process helps ensure smooth execution.

Form 1099-R documents all distributions from retirement accounts. You'll receive this form following any withdrawal, detailing the distribution amount and any taxes withheld. This information transfers to your tax return, where the distribution appears as taxable income unless an exception applies.

Maintaining records of hardship withdrawals, including documentation supporting your qualifying need, provides protection if the IRS questions your distribution. Similarly, tracking the basis in Roth accounts ensures accurate tax reporting when you eventually take distributions.

Required documentation typically includes:

- Withdrawal request forms specifying amount and timing

- Direct deposit or payment delivery instructions

- Tax withholding elections and calculations

- Supporting evidence for hardship withdrawals

- Rollover certifications if moving funds between accounts

Understanding these administrative requirements prevents delays and ensures your withdrawal processes correctly. Tax strategy planning should account for documentation requirements and timing considerations that affect tax year reporting.

A 401(k) withdrawal represents a significant financial decision with immediate tax consequences and lasting retirement security implications that require careful analysis and strategic planning. The rules, exceptions, and optimal strategies vary based on your age, financial situation, and long-term objectives, making personalized guidance essential for navigating these complex decisions effectively. Working with Brookwood Investment Group provides access to fiduciary advisors who offer comprehensive retirement planning, tax strategy development, and investment management services tailored to your unique circumstances. Consider scheduling a consultation to discuss your specific situation and develop a strategic approach to managing your retirement assets.