Inheriting an IRA can feel overwhelming, particularly when you're navigating the complexities of distribution rules, tax implications, and regulatory changes that have reshaped the retirement account landscape. Whether you've recently become a beneficiary or are planning your own estate strategy, understanding the nuances of an inherited IRA is essential for preserving wealth and minimizing tax burdens. The SECURE Act of 2019 fundamentally altered how most beneficiaries must handle these accounts, creating new timelines and considerations that require careful attention and strategic planning.

Understanding the Basics of Inherited IRAs

An inherited IRA represents a retirement account passed to a beneficiary after the original owner's death. These accounts maintain their tax-deferred or tax-free status, but the distribution requirements differ significantly from standard IRAs. The type of IRA you inherit (traditional or Roth), your relationship to the deceased, and the timing of their death all influence your options and obligations.

When someone names you as a beneficiary on their retirement account, you gain access to those funds, but you cannot treat the account as your own in most cases. The rules governing inherited IRAs have become increasingly complex, requiring beneficiaries to understand their specific circumstances before making distribution decisions.

Types of Beneficiaries and Their Different Rules

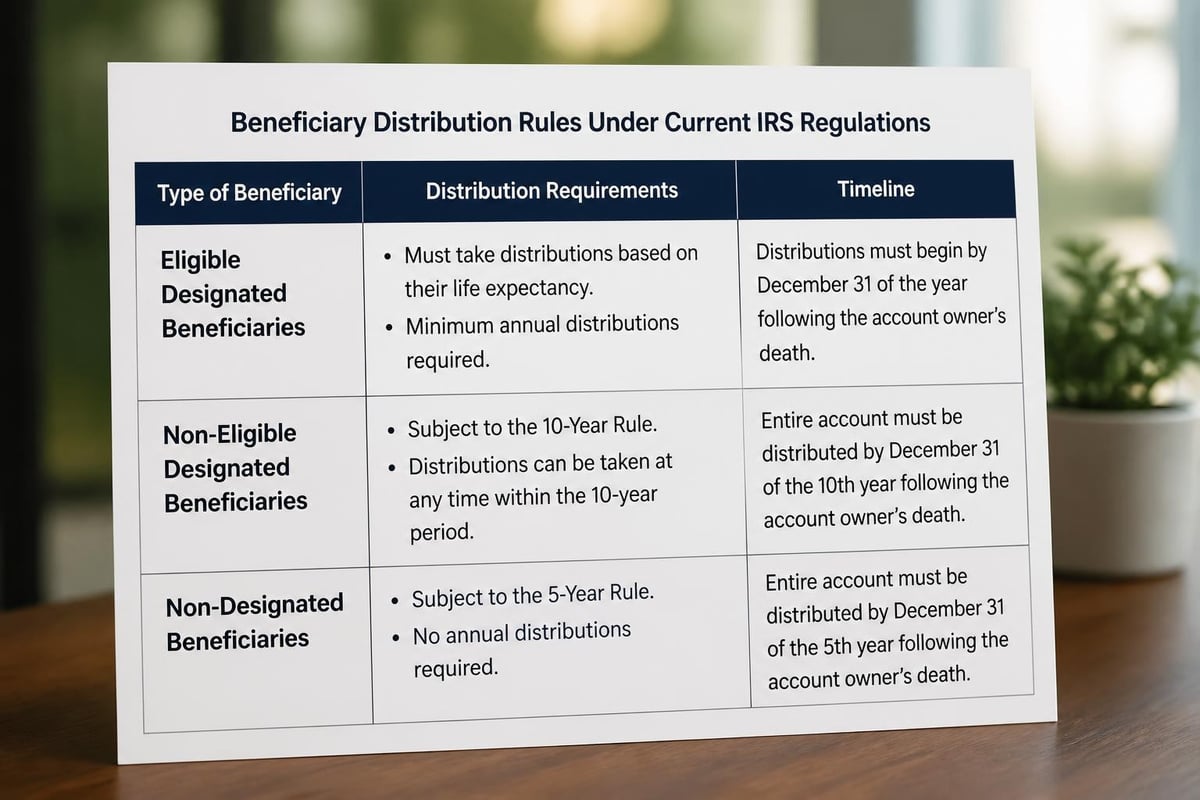

The IRS categorizes beneficiaries into distinct groups, each with unique distribution requirements. Understanding which category applies to your situation determines your available options and required actions.

Eligible Designated Beneficiaries include:

- Surviving spouses

- Minor children of the account owner (until reaching majority)

- Disabled or chronically ill individuals

- Persons not more than 10 years younger than the deceased

Non-eligible Designated Beneficiaries encompass all other individual beneficiaries who don't meet the criteria above. This category includes adult children, siblings, nieces, nephews, and friends.

Non-designated Beneficiaries refer to entities such as estates, charities, and most trusts. These beneficiaries face the most restrictive distribution rules.

The 10-Year Rule and Required Minimum Distributions

The SECURE Act introduced the 10-year rule, which fundamentally changed distribution requirements for most inherited IRA beneficiaries. This regulation requires non-eligible designated beneficiaries to withdraw all funds from the inherited account within 10 years of the original owner's death.

Initially, there was confusion about whether annual distributions were required during this period. The IRS clarified in 2022 that if the original account owner had already begun taking required minimum distributions (RMDs), the beneficiary must continue taking annual RMDs during the 10-year period. If the owner died before their required beginning date, the beneficiary can take distributions on any schedule, as long as the account is fully depleted by the end of year 10.

Spouse Beneficiary Options

Surviving spouses enjoy the most flexibility when inheriting an IRA. They can choose from several strategies depending on their age, financial needs, and tax situation:

- Treat the IRA as their own by rolling it into their existing IRA or designating themselves as the account owner

- Remain a beneficiary and take distributions based on their life expectancy

- Apply the 10-year rule if they prefer accelerated distributions

- Disclaim the inheritance to pass it to contingent beneficiaries

Rolling the account into their own IRA often provides the greatest flexibility, allowing the surviving spouse to delay RMDs until they reach age 73 (as of 2026). This strategy works particularly well for younger spouses who don't need immediate income.

Tax Implications of Inherited Traditional vs. Roth IRAs

The tax treatment of distributions from your inherited IRA depends critically on whether you've inherited a traditional or Roth account. Understanding these differences helps you make informed decisions about distribution timing and amounts.

Inherited Traditional IRA Taxation

Distributions from an inherited traditional IRA are taxed as ordinary income in the year you receive them. This creates a planning opportunity: you can potentially manage your tax bracket by controlling the timing and amount of distributions, particularly if the 10-year rule applies without annual RMD requirements.

Consider spreading distributions across multiple years if you're subject to the 10-year rule without annual RMDs. Taking the entire balance in year 10 could push you into a significantly higher tax bracket, whereas strategic annual distributions might keep you in a lower bracket throughout the period.

Inherited Roth IRA Considerations

Roth IRA distributions are generally tax-free, provided the account has been open for at least five years. Even if you must withdraw funds within 10 years, qualified distributions maintain their tax-free status. This characteristic makes inherited Roth IRAs particularly valuable, as the funds can continue growing tax-free during the distribution period.

Working with fiduciary financial advisors can help you develop a distribution strategy that maximizes the tax-free growth potential while meeting regulatory requirements.

Strategic Distribution Planning

Developing a thoughtful distribution strategy requires balancing multiple factors: your current income needs, tax situation, other retirement assets, and long-term financial goals. Rushing into distributions without proper planning can result in unnecessary tax liabilities and lost growth opportunities.

| Distribution Strategy | Best For | Key Consideration |

|---|---|---|

| Minimum required only | Those in high tax brackets | Maximizes tax-deferred growth |

| Equal annual distributions | Predictable income needs | Simplifies planning and budgeting |

| Tax-bracket management | Variable income situations | Requires annual analysis |

| Delayed distributions | Young beneficiaries | Maximizes compounding potential |

Coordinating With Other Income Sources

Your inherited IRA distributions don't exist in isolation. They interact with Social Security benefits, pension income, investment earnings, and other revenue streams. Large distributions can trigger:

- Higher Medicare Part B and Part D premiums through IRMAA surcharges

- Increased taxation of Social Security benefits

- Phase-outs of various tax deductions and credits

- Net investment income tax obligations

Comprehensive retirement planning accounts for these interactions, optimizing your overall tax situation rather than focusing solely on the inherited IRA.

Trust as Beneficiary Considerations

Naming a trust as an IRA beneficiary adds another layer of complexity but may serve important estate planning purposes. Trusts as beneficiaries face specific requirements and restrictions that demand careful structuring.

Reasons to name a trust as beneficiary:

- Control over distributions to spendthrift heirs

- Protection for beneficiaries with special needs

- Asset protection from creditors or divorce

- Management for minor children beyond age of majority

Challenges and requirements:

- Trust must be valid under state law

- Trust must be irrevocable or become irrevocable at death

- Beneficiaries must be identifiable

- Documentation must be provided to the IRA custodian

The type of trust matters significantly. See-through trusts that meet specific IRS requirements allow the IRA to be distributed based on the oldest trust beneficiary's life expectancy, while non-qualifying trusts face the most restrictive distribution rules.

Common Mistakes to Avoid

Navigating inherited IRA rules presents numerous pitfalls that can result in penalties, unnecessary taxes, or lost planning opportunities. Awareness of these common errors helps you avoid costly mistakes.

Missing Distribution Deadlines

Failing to take required distributions triggers a 25% excise tax on the amount that should have been withdrawn. This penalty can be reduced to 10% if corrected within two years, but avoiding the mistake altogether is clearly preferable. Understanding distribution requirements for your specific situation is essential.

Improper Titling

The inherited IRA must be properly titled to maintain its tax-advantaged status. The account should be registered in the deceased owner's name for the benefit of the beneficiary. Incorrect titling can result in immediate taxation of the entire balance.

Failing to Update Beneficiary Designations

If you inherit an IRA and fail to name your own beneficiaries, the account typically passes to your estate upon your death, potentially subjecting it to probate and unfavorable distribution rules. Update beneficiary designations promptly after inheriting the account.

Not Considering State Tax Implications

While federal tax rules apply uniformly, state tax treatment of inherited IRAs varies significantly. Some states exempt certain beneficiaries, while others impose inheritance taxes on top of income taxes. Understanding your state's specific rules is crucial for complete planning.

Multiple Beneficiary Situations

When an IRA has multiple beneficiaries, the situation becomes more complex. Each beneficiary's distribution requirements are typically determined by the oldest beneficiary's age unless the account is properly separated.

Key considerations with multiple beneficiaries:

- Separate accounts by December 31 of the year following the owner's death

- Each beneficiary can then use their own age for calculating distributions (if applicable)

- Different beneficiary categories can pursue their own strategies

- Communication and coordination prevent misunderstandings

For example, if three siblings inherit an IRA and one qualifies as disabled, splitting the account allows the disabled sibling to stretch distributions over their life expectancy while the other two follow the 10-year rule.

Year-of-Death RMDs

If the original IRA owner died after their required beginning date but before taking their RMD for that year, the beneficiary must withdraw the remaining RMD amount by December 31 of the death year. This often-overlooked requirement can result in penalties if missed.

The year-of-death RMD is calculated based on the deceased owner's age and account balance, not the beneficiary's situation. This distribution is in addition to any distributions the beneficiary must take under their own requirements starting the following year.

Conversion and Recharacterization Limitations

Unlike account owners, beneficiaries cannot convert an inherited traditional IRA to an inherited Roth IRA. This restriction eliminates one potential tax planning strategy available to original account owners. However, tax-efficient distribution planning can still optimize your tax situation through careful timing and amount management.

The inability to convert emphasizes the importance of Roth conversions during the original owner's lifetime as part of comprehensive estate planning strategies. Converting traditional IRA assets to Roth before death can provide beneficiaries with more favorable tax treatment.

Documentation and Record-Keeping

Maintaining thorough documentation of your inherited IRA is essential for tax compliance and future planning. Keep detailed records of:

- The original account owner's date of death

- Account valuations at death and each subsequent year-end

- All distribution amounts and dates

- Tax forms (1099-R) for each distribution

- Beneficiary designation forms

- Communication with the IRA custodian

These records prove invaluable during tax preparation, IRS inquiries, or estate planning updates. Digital copies stored securely provide backup protection against physical document loss.

Working With Financial Professionals

The complexity of inherited IRA rules makes professional guidance particularly valuable. A qualified advisor can help you:

- Determine your beneficiary classification and applicable rules

- Model different distribution scenarios and their tax impacts

- Integrate the inherited IRA into your overall financial plan

- Coordinate with tax professionals for optimal outcomes

- Navigate custodian requirements and paperwork

Investment management services that include inherited IRA expertise ensure your assets continue working effectively toward your financial goals while maintaining compliance with distribution requirements.

Looking Ahead: Potential Legislative Changes

Tax laws continue evolving, and inherited IRA rules may face future modifications. Staying informed about potential changes helps you adapt your strategy as needed. The SECURE 2.0 Act has already made additional adjustments to retirement account rules, and further refinements remain possible.

While you cannot control legislative changes, maintaining flexibility in your distribution strategy allows you to adjust as new rules emerge. Regular reviews with financial professionals help ensure your approach remains optimal under current regulations.

Navigating inherited IRA rules requires understanding complex regulations, tax implications, and strategic options specific to your beneficiary status and financial situation. The right distribution strategy balances immediate needs with long-term tax efficiency while maintaining full compliance with IRS requirements. Brookwood Investment Group LLC provides personalized guidance on inherited IRA management, retirement planning, and comprehensive wealth strategies designed to help you make informed decisions that align with your unique goals and circumstances.