Understanding what you'll invest in professional financial guidance represents a crucial step in building a successful relationship with an advisor. Financial advisor cost varies significantly based on the services you need, the complexity of your financial situation, and the compensation model your advisor uses. As you evaluate options for managing your wealth and planning your financial future, gaining clarity on how advisors charge for their expertise helps you make informed choices that align with your goals and budget.

Common Financial Advisory Fee Structures

The financial advisory industry employs several distinct compensation models, each with unique characteristics that affect your total investment in professional guidance. Understanding these fee structures enables you to compare options effectively and identify which approach best suits your financial circumstances.

Assets Under Management (AUM) Fees

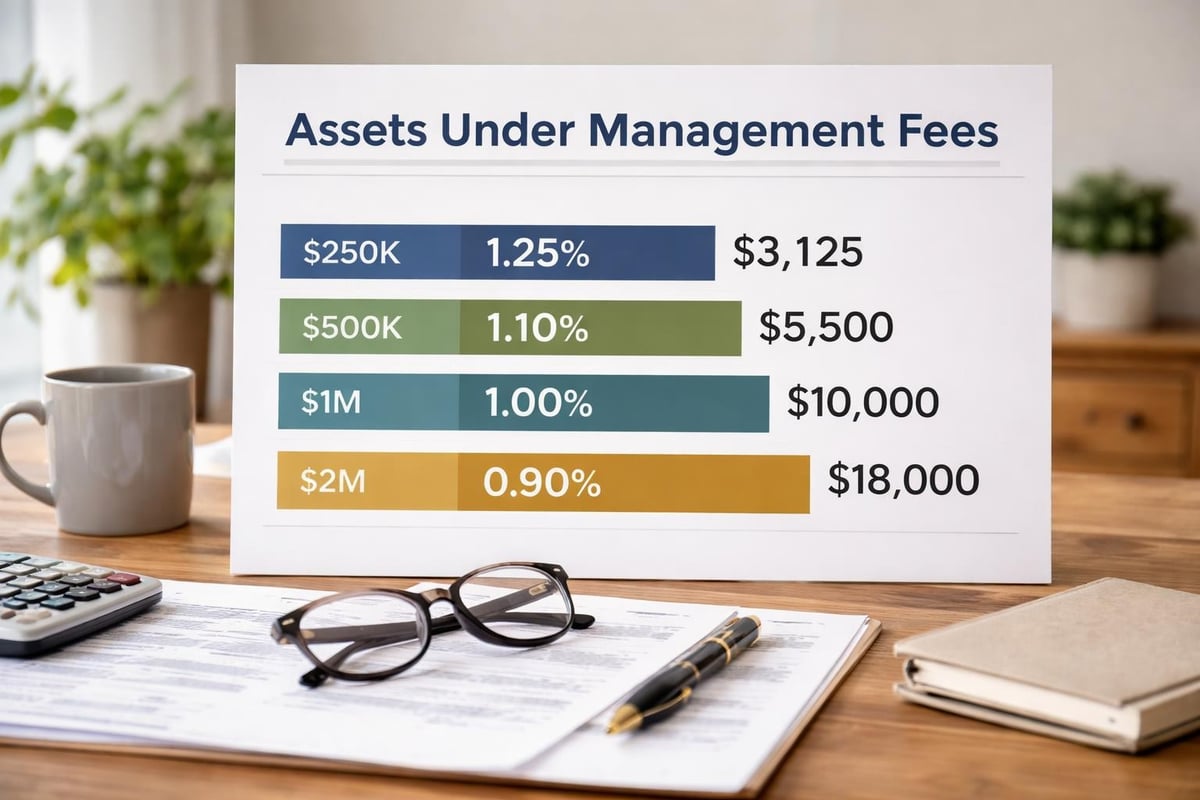

The most prevalent pricing model involves charging a percentage of the assets your advisor manages on your behalf. This structure typically ranges from 0.50% to 2.00% annually, with the percentage often decreasing as your portfolio value increases.

Key characteristics of AUM fees include:

- Percentage decreases at higher asset tiers (breakpoints)

- Charges calculated quarterly based on portfolio value

- Alignment between advisor success and client portfolio growth

- Comprehensive service coverage without separate billing

For example, a client with $500,000 in managed assets paying a 1.00% annual fee would invest $5,000 per year for ongoing portfolio management and financial planning services. This model has become popular among fiduciary advisory services because it creates natural alignment between the advisor's compensation and client outcomes.

Hourly Rate Arrangements

Some financial professionals charge for their time rather than basing fees on assets. Hourly rates for financial advisors generally range from $150 to $450 per hour, depending on the advisor's experience, credentials, and geographic location.

This model works particularly well for:

- One-time financial plan development

- Specific project consultations

- Second opinions on investment strategies

- Clients who prefer to implement recommendations independently

Financial advisor cost transparency reaches its peak with hourly billing since you pay only for the time you actually use. However, estimating total project costs can prove challenging until the work begins.

Flat Fee Packages

Flat fee structures provide predetermined pricing for specific services or comprehensive annual planning. A one-time financial plan might cost between $1,500 and $10,000, while annual retainer arrangements typically range from $2,000 to $7,500.

| Service Type | Typical Flat Fee Range | What's Included |

|---|---|---|

| Basic Financial Plan | $1,500 – $3,000 | Budget analysis, retirement projections, basic recommendations |

| Comprehensive Plan | $3,000 – $10,000 | Detailed analysis, tax strategies, estate planning, investment recommendations |

| Annual Retainer | $2,000 – $7,500 | Ongoing access, plan updates, quarterly reviews |

This transparent pricing model appeals to clients seeking predictable costs without surprises.

Factors Influencing Financial Advisor Cost

Multiple variables determine what you'll ultimately invest in professional financial guidance. Understanding these factors helps you evaluate whether the financial advisor cost aligns with the value you receive.

Complexity of Your Financial Situation

Straightforward financial circumstances generally warrant lower fees than complex situations involving multiple income streams, business ownership, or intricate estate planning needs. Financial advisors for business owners often command higher fees due to the specialized expertise required.

Factors that increase service complexity:

- Multiple business entities or partnerships

- Stock options and executive compensation packages

- Multi-generational wealth transfer planning

- International tax considerations

- Charitable giving strategies involving trusts or foundations

Advisor Credentials and Experience

Professional certifications like CFP® (Certified Financial Planner), CFA® (Chartered Financial Analyst), and CPA (Certified Public Accountant) typically correlate with higher fees. These designations require extensive education, rigorous examinations, and ongoing continuing education commitments.

Advisors with specialized expertise in areas like retirement planning and estate planning may charge premium rates reflecting their advanced knowledge and experience navigating complex scenarios.

Geographic Location and Service Delivery

Traditional in-person advisory relationships in high-cost metropolitan areas typically command higher fees than virtual arrangements. However, virtual-first firms have disrupted this pattern by offering access to experienced professionals regardless of client location.

The shift toward virtual advisory services has created opportunities for clients to access top-tier expertise without premium geographic pricing, particularly when working with independent financial advisors who operate with lower overhead than traditional brick-and-mortar practices.

Comparing Different Compensation Models

Various fee structures available to financial advisors each present distinct advantages and considerations. Evaluating these models against your specific needs helps identify the most suitable approach.

Fee-Only vs. Commission-Based Compensation

Fee-only advisors receive compensation exclusively from client fees, eliminating potential conflicts of interest associated with product sales commissions. This model has gained significant traction among clients seeking unbiased recommendations.

Commission-based advisors earn income through commissions on financial products they recommend, such as insurance policies or mutual funds. While this can reduce upfront costs, it may create incentive misalignment since compensation depends on specific product sales rather than overall client outcomes.

Fee-based advisors combine both models, charging planning fees while also earning commissions on certain products. Understanding which model your advisor uses proves essential for evaluating potential conflicts of interest.

Assessing Value Beyond Price

The lowest financial advisor cost doesn't necessarily represent the best value. Effective advisory relationships generate value through:

- Tax-efficient investment strategies that reduce annual tax liability

- Behavioral coaching that prevents costly emotional decisions during market volatility

- Estate planning that minimizes transfer taxes and administrative costs

- Retirement income strategies that maximize sustainable withdrawal rates

- Risk management that protects accumulated wealth

Research suggests that comprehensive financial planning can add significant value annually through tax optimization, strategic asset allocation, and behavioral guidance. When evaluating financial advisor cost, consider the potential financial impact of professional guidance across multiple planning dimensions.

Questions to Ask About Advisor Fees

Transparency regarding compensation helps establish trust and ensures you understand exactly what you're investing in professional guidance. Before engaging an advisor, ask these critical questions:

Fee Structure Questions:

- How do you charge for your services?

- What specific services are included in your fee?

- Are there any additional costs beyond your stated fee?

- How often do you bill, and when is payment due?

- Do you receive any compensation from third parties for recommendations?

Understanding Total Cost of Service

Evaluating the complete financial advisor cost requires looking beyond stated advisory fees to underlying investment expenses. Management fees for mutual funds, ETFs, and other investment vehicles add to your total annual cost.

A comprehensive cost analysis should include:

- Advisory fees (AUM, hourly, or flat fee)

- Underlying investment expense ratios

- Trading costs and transaction fees

- Custodian fees (if applicable)

- Tax preparation fees for complex returns

Request a clear breakdown showing all anticipated costs so you can make accurate comparisons between advisors and evaluate total investment in professional guidance.

Financial Advisory Costs for Different Life Stages

Your financial advisor cost often correlates with your life stage and the complexity of planning needs you face. Understanding typical costs at different stages helps you budget appropriately for professional guidance.

Early Career Professionals

Young professionals building wealth typically benefit from hourly consultations or flat-fee plans rather than AUM arrangements. Initial planning might cost $1,500 to $3,000 for comprehensive guidance on:

- Student loan repayment strategies

- Emergency fund establishment

- Retirement account selection and contribution optimization

- Basic insurance coverage assessment

- Career decision financial analysis

This approach provides valuable guidance while keeping financial advisor cost proportionate to current assets and income levels.

Mid-Career Wealth Accumulators

As wealth accumulates and financial situations grow more complex, many clients transition to AUM or retainer arrangements. At this stage, financial advisor cost might range from $3,000 to $15,000 annually, depending on portfolio size and service scope.

Planning typically expands to include:

- Advanced tax optimization strategies

- College funding plans

- Real estate investment analysis

- Business succession planning (for entrepreneurs)

- Comprehensive risk management

Working with fiduciary planning professionals ensures recommendations prioritize your interests throughout this critical wealth-building phase.

Pre-Retirement and Retirement Planning

Approaching retirement introduces complex decisions around Social Security claiming, pension elections, Medicare planning, and sustainable withdrawal strategies. Financial advisor cost during this phase often represents the highest value-add period.

| Planning Focus | Typical Cost Range | Key Services |

|---|---|---|

| Pre-Retirement (5-10 years out) | $5,000 – $20,000 annually | Retirement readiness analysis, income planning, tax-efficient distribution strategies |

| Transition Phase | $2,500 – $5,000 (one-time) | Social Security optimization, pension analysis, healthcare coverage planning |

| Retirement Income Management | 0.75% – 1.25% of AUM | Ongoing portfolio management, systematic withdrawals, tax coordination, estate updates |

The complexity of coordinating multiple income sources while managing longevity risk and healthcare costs justifies investment in experienced guidance during this critical transition.

Alternative Advisory Options and Their Costs

Traditional one-on-one advisory relationships aren't the only option for accessing professional financial guidance. Several alternatives offer varying service levels at different price points.

Robo-Advisors

Automated investment platforms typically charge 0.25% to 0.50% of assets under management for algorithm-driven portfolio management and basic planning tools. While significantly cheaper than human advisors, these platforms offer limited personalization and no behavioral coaching during market stress.

Understanding how robo-advisors compare to traditional advisory relationships helps determine whether the cost savings justify the reduced service level for your situation.

Hybrid Models

Some firms combine automated portfolio management with access to human advisors for specific questions or periodic reviews. These hybrid approaches typically charge 0.40% to 0.75% of AUM, offering a middle ground between pure robo-advisors and comprehensive human guidance.

Financial Planning Subscriptions

Monthly subscription services have emerged offering ongoing access to financial planners for flat monthly fees ranging from $100 to $500. These services work well for clients seeking regular guidance without asset-based fees, particularly those building wealth or preferring to manage investments independently while accessing planning expertise.

Evaluating Whether Advisory Costs Are Justified

Determining whether financial advisor cost represents worthwhile investment requires honest assessment of your financial knowledge, time availability, and the potential value professional guidance could generate.

DIY Financial Management Considerations

Managing your finances independently eliminates advisory fees but requires:

- Significant time investment in research and ongoing education

- Emotional discipline during market volatility

- Comprehensive understanding of tax laws and planning strategies

- Expertise across investment management, estate planning, and insurance

- Systematic approach to rebalancing and risk management

Many successful professionals find that the time required for effective financial management exceeds what they can realistically dedicate while maintaining career focus and work-life balance.

Measuring Advisory Value

Professional guidance generates value through multiple channels beyond investment returns. Consider whether an advisor might help you:

- Avoid costly mistakes in retirement account rollovers or withdrawal sequencing

- Implement tax-loss harvesting and asset location strategies

- Navigate complex estate planning decisions

- Optimize Social Security claiming strategies worth tens of thousands in lifetime benefits

- Maintain investment discipline during market downturns

When these benefits exceed the financial advisor cost, professional guidance represents a sound investment in your financial success.

Making the Decision About Advisory Services

Selecting the right advisor at the appropriate fee level requires careful evaluation of your needs, preferences, and financial circumstances. Start by clarifying what services you actually need versus what might be nice to have.

Decision framework for advisory engagement:

- Assess complexity: How complicated is your financial situation?

- Evaluate expertise gaps: Where do you lack knowledge or confidence?

- Calculate time investment: How many hours would DIY management require?

- Determine service preferences: Do you prefer ongoing relationships or project-based engagement?

- Compare total costs: What would comprehensive guidance cost across different models?

Understanding what financial advice should cost in your specific situation helps you evaluate proposals from prospective advisors and identify fair pricing for the services you need.

Negotiating Advisory Fees

While many advisory fees follow standard industry benchmarks, some flexibility exists, particularly for clients with larger portfolios or straightforward planning needs. Approach fee discussions professionally by:

- Requesting detailed service descriptions for proposed fees

- Asking about fee reductions at higher asset levels

- Inquiring whether services can be unbundled if you don't need comprehensive offerings

- Understanding whether annual reviews might identify opportunities to adjust service levels and fees

Remember that the goal isn't necessarily the lowest financial advisor cost, but rather optimal value for the services you receive.

Understanding financial advisor cost structures, typical fee ranges, and the factors that influence pricing enables you to make informed decisions about professional financial guidance that aligns with your goals and budget. When you're ready to explore personalized financial planning with transparent, client-focused guidance, Brookwood Investment Group offers fiduciary advisory services tailored to your unique situation through a virtual-first approach that combines accessibility with comprehensive expertise in retirement planning, investment management, and tax-efficient strategies.