When selecting someone to manage your financial future, the term "fiduciary" represents more than industry jargon. A fiduciary investment advisor operates under a legal and ethical obligation to place your interests above their own, a standard that distinguishes them from other financial professionals. Understanding this distinction becomes increasingly important as you navigate complex decisions around retirement planning, investment management, and wealth preservation. The choice between a fiduciary and a non-fiduciary advisor can significantly impact your portfolio's performance, fee structure, and overall financial trajectory.

Understanding the Fiduciary Standard

The fiduciary standard represents the highest standard of care in financial services. When an advisor operates as a fiduciary, they must act in your best interests at all times, disclosing any conflicts of interest and prioritizing your financial well-being over their compensation.

This standard contrasts sharply with the suitability standard, which only requires recommendations to be suitable for your situation, not necessarily optimal. A non-fiduciary advisor can recommend products that generate higher commissions, as long as they meet basic suitability criteria.

Legal Framework and Regulatory Oversight

The Investment Advisers Act of 1940 established the foundation for fiduciary duty in the United States. Registered Investment Advisors (RIAs) must adhere to this standard under Securities and Exchange Commission (SEC) oversight.

Key regulatory requirements include:

- Full disclosure of compensation structures and potential conflicts

- Written documentation of the fiduciary relationship

- Ongoing monitoring of investment recommendations

- Transparency in fee arrangements and service agreements

According to guidance on verifying fiduciary status, understanding the regulatory framework helps investors confirm an advisor's obligations. The distinction matters because some financial professionals only act as fiduciaries in certain capacities or for specific accounts.

How a Fiduciary Investment Advisor Differs from Other Financial Professionals

The financial services industry includes various professionals with different regulatory standards. Understanding these differences helps you identify the right partner for your needs.

Broker-Dealers and Registered Representatives

Broker-dealers operate under the suitability standard when making investment recommendations. They can receive commissions on products they sell, which may create incentive misalignment.

While some brokers provide valuable services, their compensation model differs fundamentally from the fiduciary approach. The comparison between advisers, brokers, and insurance agents highlights these structural differences in how professionals are compensated and regulated.

Dual-Registered Advisors

Some professionals maintain both RIA and broker-dealer registrations. This dual status means they act as fiduciaries for some services while operating under the suitability standard for others.

| Advisor Type | Standard | Regulatory Body | Compensation Model |

|---|---|---|---|

| Registered Investment Advisor | Fiduciary | SEC or State | Fees (AUM, hourly, flat) |

| Broker-Dealer | Suitability | FINRA | Commissions + Fees |

| Dual-Registered | Both | SEC/FINRA | Mixed |

| Insurance Agent | Suitability | State Insurance Dept. | Commissions |

This complexity makes verification essential. A fiduciary investment advisor operating exclusively as an RIA avoids these potential conflicts inherent in dual registration.

Benefits of Working with a Fiduciary Investment Advisor

Selecting a fiduciary advisor provides distinct advantages that extend beyond basic investment recommendations. The structural differences in how these professionals operate create tangible benefits for your financial planning.

Transparency in Fees and Compensation

Fee-only fiduciary advisors receive compensation directly from clients rather than product commissions. This structure eliminates incentives to recommend higher-commission products that may not align with your goals.

Common fee structures include:

- Assets under management (AUM) percentages

- Hourly consultation rates

- Fixed retainer fees

- Project-based pricing

Understanding what fiduciary truly means in practical terms helps you evaluate whether an advisor's compensation model creates alignment or conflict. Virtual-first advisory firms often provide detailed fee disclosures upfront, making cost comparison straightforward.

Conflict-Free Recommendations

A fiduciary investment advisor must navigate around conflicts that could compromise objectivity. This obligation extends to all aspects of financial planning, from investment selection to estate planning strategies.

When evaluating insurance products, retirement accounts, or investment vehicles, a fiduciary cannot favor options that generate personal compensation at your expense. This protection becomes particularly valuable in complex situations involving:

- Rollover decisions from employer-sponsored retirement plans

- Annuity selections with varying commission structures

- Tax-advantaged account allocations

- Estate planning product recommendations

- Alternative investment opportunities

Comprehensive Financial Planning

The fiduciary relationship typically encompasses broader planning beyond investment selection. A holistic approach considers how different financial elements interact to support your long-term objectives.

Fiduciary planning services often integrate retirement planning, tax strategies, estate planning, and investment management. This coordination ensures your financial plan operates as a cohesive system rather than disconnected parts.

Identifying and Verifying Fiduciary Status

Not all advisors who claim fiduciary status maintain this standard consistently. Verification requires specific steps and questions beyond accepting surface-level representations.

Essential Questions to Ask

The right questions reveal an advisor's true obligations. Asking whether an advisor acts in your best interests requires more specificity than a simple yes-or-no question about fiduciary status.

Critical verification questions:

- Will you provide written acknowledgment of your fiduciary duty?

- Do you receive any third-party compensation for product recommendations?

- Are you registered as an investment advisor with the SEC or state regulators?

- In what situations, if any, would you not act as a fiduciary?

- How do you handle conflicts of interest when they arise?

These questions create accountability and surface potential conflicts before they impact your financial decisions. Documentation matters-verbal assurances carry less weight than written commitments.

Checking Regulatory Databases

Public databases allow independent verification of an advisor's registration and disciplinary history. The SEC's Investment Adviser Public Disclosure (IAPD) system provides comprehensive information on registered advisors.

Key information to review:

- Form ADV Part 2 (the firm's brochure detailing services and fees)

- Disciplinary history and regulatory actions

- Assets under management and client counts

- Conflicts of interest disclosures

- Compensation arrangements

State securities regulators maintain similar databases for advisors managing assets below SEC registration thresholds. This verification process typically takes less than thirty minutes but provides substantial clarity about an advisor's background and obligations.

The Role of Fiduciary Investment Advisors in Retirement Planning

Retirement planning presents unique challenges where the fiduciary standard provides significant value. The complexity of coordinating income sources, tax strategies, and distribution planning benefits from conflict-free guidance.

Social Security Optimization

Claiming decisions for Social Security benefits create permanent consequences. A fiduciary investment advisor analyzes your specific situation-including health factors, other income sources, and longevity considerations-without bias toward products that generate commissions.

The analysis considers:

- Spousal benefit coordination for married couples

- Tax implications of different claiming ages

- Break-even analysis comparing claiming strategies

- Medicare premium impacts from additional income

- Continued employment effects on benefit calculations

These decisions interact with broader retirement planning considerations, making unbiased guidance particularly valuable.

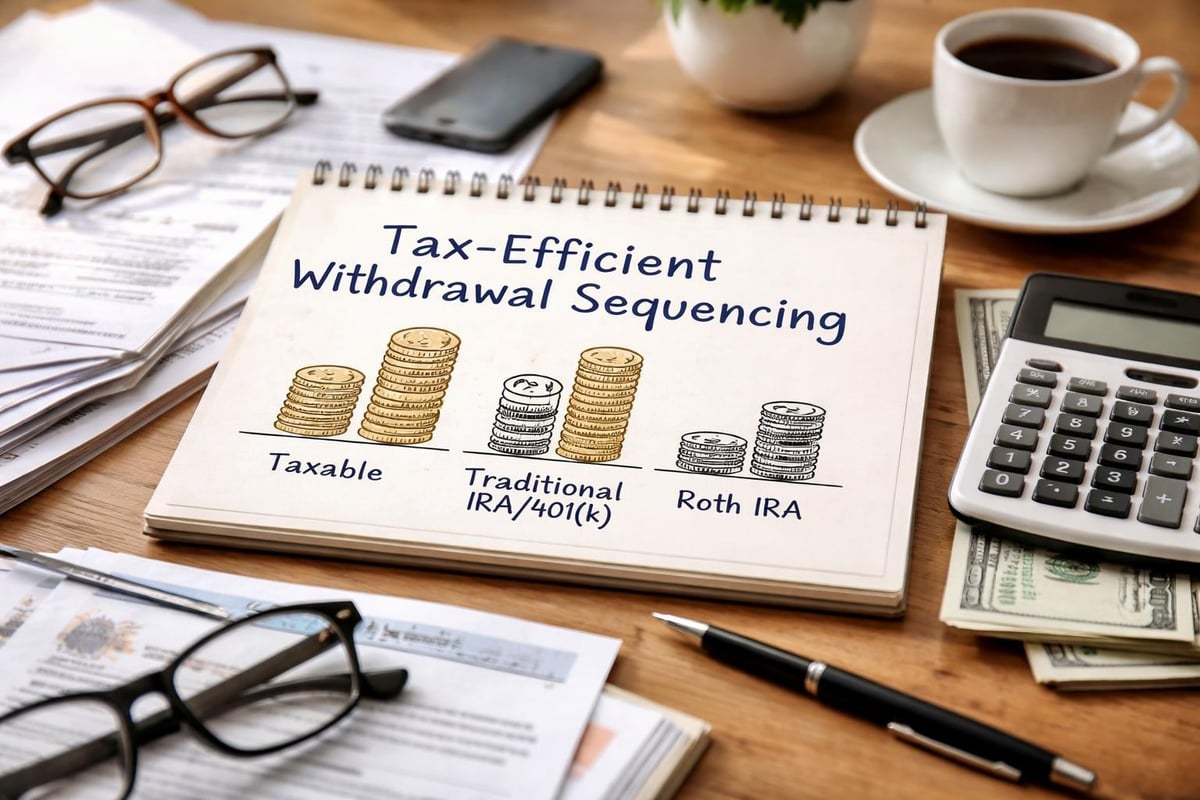

Distribution Strategy Development

How you withdraw funds during retirement affects tax liability, portfolio longevity, and estate outcomes. A fiduciary approach prioritizes tax efficiency and sustainability over product sales.

| Withdrawal Source | Tax Treatment | Strategic Considerations |

|---|---|---|

| Roth Accounts | Tax-free | Preserve for later years or heirs |

| Traditional IRA/401(k) | Ordinary income | Required minimum distributions after age 73 |

| Taxable Accounts | Capital gains rates | Tax-loss harvesting opportunities |

| Cash Value Life Insurance | Potentially tax-free | Loan vs. withdrawal implications |

Creating an optimal sequence considers your tax bracket trajectory, required minimum distribution timing, and potential legacy goals. Financial planning and investment management integration ensures these elements work together coherently.

Investment Management Under the Fiduciary Standard

The fiduciary obligation extends to ongoing portfolio management, not just initial recommendations. This continuous duty affects how advisors construct portfolios, manage risk, and rebalance holdings.

Portfolio Construction Principles

A fiduciary investment advisor builds portfolios based on your risk tolerance, time horizon, and financial goals rather than commission potential. This approach typically emphasizes low-cost, diversified investment vehicles.

Modern portfolio theory principles guide allocation decisions:

- Asset class diversification across domestic and international markets

- Cost minimization through index funds or ETFs when appropriate

- Tax efficiency in investment vehicle selection

- Rebalancing protocols that maintain target allocations

- Risk management aligned with your capacity for volatility

Investment management strategies under fiduciary oversight focus on factors within control-costs, taxes, and diversification-rather than attempting to time markets or select "hot" investments.

Avoiding High-Cost Products

The absence of commission incentives removes pressure to recommend expensive or complex products. Many actively managed mutual funds, variable annuities, and structured products carry costs that significantly impact long-term returns.

Fee comparison matters substantially over time. A 1% difference in annual fees on a $500,000 portfolio compounds to over $130,000 in additional costs over twenty years, assuming 7% gross returns.

Tax Strategy Coordination

Effective financial planning requires integration between investment decisions and tax implications. A fiduciary investment advisor considers tax efficiency as a core component of portfolio management and distribution planning.

Tax-Loss Harvesting

Systematically capturing investment losses to offset gains reduces annual tax liability. This strategy works particularly well in taxable accounts, where realized losses can offset gains or reduce ordinary income.

The process involves:

- Identifying positions trading below cost basis

- Selling to realize the loss

- Replacing with similar (but not substantially identical) investments

- Maintaining desired asset allocation throughout

- Tracking losses for current and future tax years

A fiduciary approach implements this strategy based on your tax situation rather than transaction-based compensation considerations.

Retirement Account Conversions

Roth conversions create current tax liability in exchange for future tax-free growth and withdrawals. A fiduciary investment advisor evaluates whether this strategy serves your interests based on current and projected tax rates, required minimum distribution impacts, and estate planning goals.

The analysis considers your complete financial picture, including:

- Current marginal tax bracket versus expected retirement rates

- State tax implications of conversion timing

- Medicare premium thresholds (IRMAA)

- Estate tax exposure for high-net-worth individuals

- Beneficiary tax situations for inherited accounts

Tax strategy planning requires personalization-generic advice rarely optimizes outcomes for individual situations.

Estate Planning Integration

A comprehensive fiduciary relationship addresses how assets transfer to beneficiaries. While fiduciary investment advisors don't replace estate attorneys, they coordinate investment and account structures with your estate plan objectives.

Beneficiary Designation Coordination

Retirement accounts, life insurance, and transfer-on-death registrations pass outside probate through beneficiary designations. These designations override will provisions, making coordination essential.

Common coordination issues include:

- Outdated beneficiaries after marriage, divorce, or deaths

- Minor children named without trust structures

- Tax inefficiency from beneficiary assignments

- Unequal inheritances conflicting with estate intentions

- Charitable giving opportunities through retirement accounts

Estate planning considerations integrate with investment management to ensure your wealth transfers according to your wishes while minimizing tax burden on heirs.

Trust Account Management

When trusts hold investment assets, fiduciary investment advisors manage these accounts consistent with trust provisions and beneficiary interests. This dual fiduciary relationship-both to you as grantor and to beneficiaries-requires careful navigation of potentially competing interests.

The Virtual-First Fiduciary Model

Technology has transformed how fiduciary advisors deliver services. Virtual-first firms provide comprehensive planning without geographic constraints, often with enhanced efficiency and accessibility.

Technology-Enhanced Service Delivery

Secure client portals, video conferencing, and digital document management enable comprehensive planning regardless of location. This model particularly benefits:

- Clients with demanding schedules who value flexible meeting times

- Those who relocate frequently or maintain multiple residences

- Individuals seeking specialized expertise unavailable locally

- People comfortable with digital communication platforms

The virtual approach doesn't diminish the fiduciary obligation. Fiduciary advisory services delivered remotely maintain the same legal and ethical standards as traditional in-person relationships.

Cost Efficiency and Accessibility

Virtual-first operations often carry lower overhead than traditional office-based models. These savings may translate to more competitive fee structures or investment minimums, making fiduciary advice accessible to a broader audience.

The model also enables more frequent communication. Rather than quarterly in-person meetings, virtual advisors can connect more regularly through video calls, addressing questions and adjustments as situations evolve.

Evaluating Fee Structures

Understanding how a fiduciary investment advisor charges for services enables informed comparisons and ensures alignment with your situation.

Assets Under Management (AUM) Fees

The most common fee structure charges a percentage of managed assets annually. Typical rates range from 0.50% to 1.50%, often decreasing at higher asset levels.

Advantages:

- Advisor compensation grows only as your portfolio grows

- No separate charges for planning services

- Predictable annual costs

- Alignment between client and advisor success

Considerations:

- Costs increase proportionally with account size

- May be expensive for high-net-worth clients

- Doesn't account for complexity of planning needs

- Potential bias toward keeping assets managed rather than debt payoff

Hourly and Retainer Models

Some fiduciary advisors charge hourly rates or annual retainers instead of AUM fees. This structure works well for clients who need planning guidance but prefer to implement recommendations independently.

Hourly rates typically range from $200 to $500, while retainers vary based on service scope. These models separate planning compensation from investment size, potentially benefiting clients with substantial assets or those who prefer unbundled services.

Project-Based Pricing

Specific financial planning projects-such as retirement analysis, Social Security optimization, or estate plan review-may carry flat fees. This approach provides cost certainty and works well for discrete planning needs.

Ongoing Monitoring and Relationship Management

The fiduciary duty extends beyond initial planning. Regular reviews ensure recommendations remain appropriate as markets change and your circumstances evolve.

Annual Review Components

Comprehensive annual reviews typically address:

- Performance analysis compared to benchmarks and objectives

- Allocation adjustments based on market changes or life events

- Tax planning for the upcoming year

- Estate plan updates reflecting legislative or family changes

- Goal progress toward retirement or other objectives

- Fee transparency showing all costs incurred

This structured approach keeps planning current and responsive to changing conditions. Customized planning requires regular updates rather than one-time recommendations.

Life Event Responsiveness

Significant life changes-retirement, inheritance, marriage, divorce, health issues-require planning adjustments. A fiduciary investment advisor adapts strategies to accommodate new circumstances without the bias of commission-generating product sales.

Quick response capability matters during time-sensitive situations. Virtual-first models often enable faster connection than scheduling in-person appointments, providing guidance when decisions can't wait.

Industry Trends Affecting Fiduciary Advisors

The financial services landscape continues evolving, with regulatory changes and market developments affecting how fiduciary advisors operate.

Regulatory Developments

The Department of Labor's fiduciary rule, SEC Regulation Best Interest, and state-level fiduciary initiatives have increased attention on advisor standards. While implementation varies, the general trend favors enhanced client protections.

These regulations attempt to close gaps between suitability and fiduciary standards, though significant differences remain. Understanding institutional investment advisor selection criteria shows how sophisticated investors prioritize fiduciary relationships.

Technology and Robo-Advisors

Automated investment platforms have entered the market with low-cost, algorithm-driven portfolio management. While these services operate as fiduciaries, they typically lack the comprehensive planning and customization that human advisors provide.

The most effective approaches often combine technology efficiency with personalized guidance. This hybrid model leverages automation for routine tasks while preserving advisor expertise for complex decisions requiring judgment and experience.

Making Your Selection Decision

Choosing a fiduciary investment advisor represents a significant decision affecting your financial future. A systematic evaluation process helps identify the right fit for your needs.

Evaluation Criteria

Beyond fiduciary status verification, consider these factors:

- Service scope: Does the advisor provide comprehensive planning or investment-only management?

- Expertise areas: What specializations or credentials does the advisor hold?

- Communication style: How frequently will you meet, and through what channels?

- Fee structure: Does the pricing model align with your asset level and needs?

- Technology platform: Can you easily access information and communicate?

- Minimum requirements: Do you meet asset or income thresholds?

Guidance on finding and vetting fiduciary advisors provides additional frameworks for evaluation. The goal is finding an advisor whose capabilities, approach, and personality fit your preferences.

Trial Period Considerations

Some relationships begin with limited engagements before committing to ongoing management. A financial plan project or hourly consultation allows you to evaluate the advisor's process, communication, and recommendations before transitioning full account management.

This approach reduces risk while providing immediate planning value. You can assess whether the advisor's recommendations demonstrate genuine fiduciary commitment or reflect conflicts of interest.

Selecting a fiduciary investment advisor ensures your financial professional operates under the highest standard of care, prioritizing your interests in every recommendation and decision. This choice fundamentally affects how your wealth is managed, the conflicts you avoid, and the peace of mind you experience throughout your financial journey. Brookwood Investment Group provides fiduciary advisory services through a virtual-first model, delivering personalized retirement planning, investment management, estate planning, and tax strategies tailored to your unique goals and lifestyle.