Setting ambitious financial objectives represents only the first step in a much larger journey. The real challenge emerges when you need to consistently work towards your goals amid competing priorities, market uncertainties, and life's inevitable changes. Whether you're preparing for retirement, building wealth for the next generation, or seeking financial independence, the path from aspiration to achievement requires structured planning, disciplined execution, and often professional guidance. Understanding the fundamental principles that drive goal attainment can transform abstract desires into concrete financial realities.

Understanding the Psychology Behind Goal Achievement

The science of goal pursuit reveals important insights about how individuals successfully work towards their goals. Research demonstrates that goal-setting effectiveness depends significantly on alignment between personal values and chosen objectives. Studies on self-concordance and implementation intentions show that individuals who pursue goals consistent with their intrinsic interests and values achieve higher success rates than those driven primarily by external pressures.

This psychological foundation proves particularly relevant in financial planning. When clients articulate retirement goals that genuinely reflect their desired lifestyle rather than arbitrary benchmarks, they demonstrate greater commitment to necessary actions. The distinction matters because financial objectives often require sustained effort over decades, not months.

Motivation Systems That Drive Progress

Understanding what fuels long-term commitment helps explain why some individuals successfully work towards your goals while others abandon their plans. Self-Determination Theory identifies three psychological needs that support sustained motivation:

- Autonomy: The need to feel in control of your financial decisions and direction

- Competence: The confidence that comes from understanding your financial situation and options

- Relatedness: The connection to advisors, family, or community who support your objectives

When financial planning addresses these fundamental needs, clients maintain engagement even during challenging market conditions or when sacrifices feel difficult. Professional advisors who recognize these motivational drivers can structure guidance that sustains commitment throughout multi-decade planning horizons.

Creating Actionable Implementation Strategies

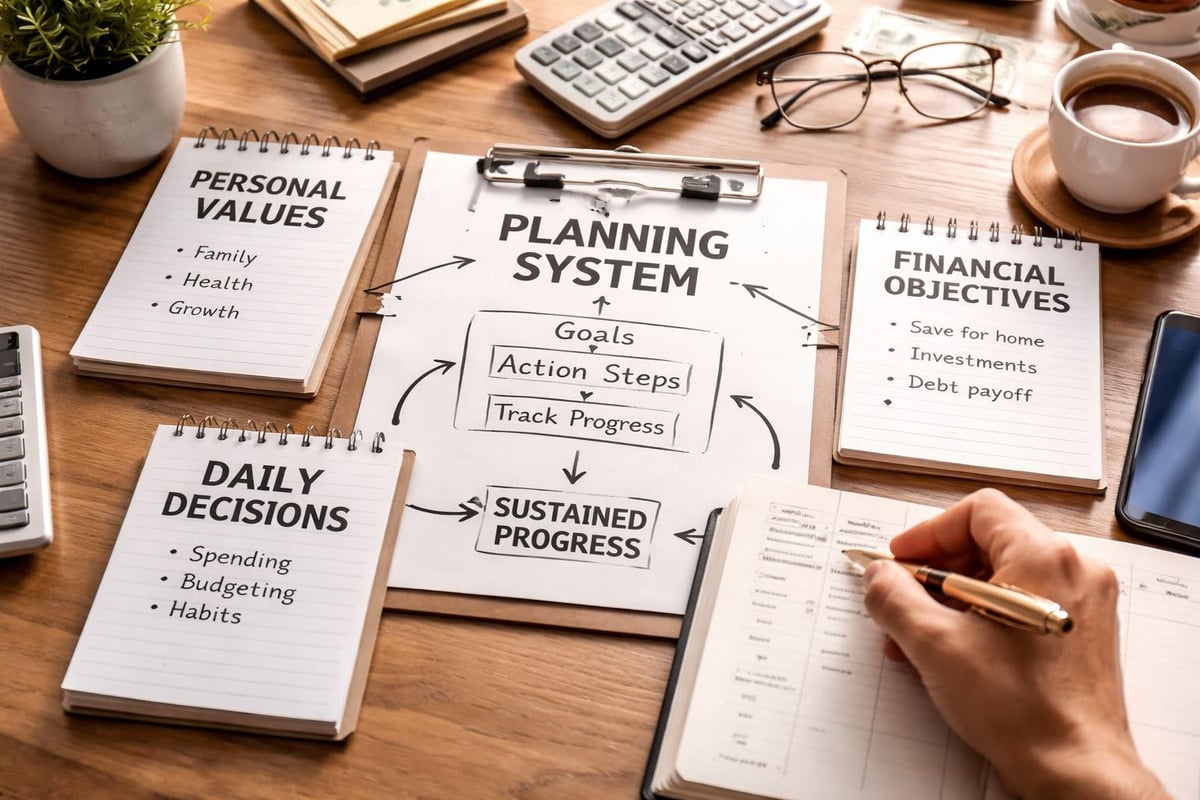

Vague intentions rarely translate into concrete results. The gap between wanting financial security and achieving it narrows considerably when you develop specific implementation intentions that define exactly when, where, and how you'll take necessary actions. This approach transforms abstract goals into executable tasks.

Consider the difference between "I want to save more for retirement" and "I will automatically transfer $1,500 to my retirement account on the first business day of each month." The second statement removes decision fatigue and creates a clear trigger for action. When you work towards your goals with this level of specificity, you bypass the motivational obstacles that derail less structured approaches.

Building Your Financial Action Framework

Evidence-based approaches to goal achievement emphasize the importance of written plans and accountability systems. Michigan State University Extension research highlights several critical components that increase success rates:

Documentation Requirements:

- Written goal statements with specific numerical targets

- Defined timelines with intermediate milestones

- Action steps broken into manageable increments

- Regular review schedules built into calendar systems

Accountability Structures:

- Scheduled check-ins with financial advisors or accountability partners

- Progress tracking mechanisms that provide visibility

- Adjustment protocols for when circumstances change

- Celebration systems for milestone achievements

This structured approach proves especially valuable for complex financial objectives like retirement planning that involve multiple variables, long time horizons, and evolving circumstances. The framework provides both direction and flexibility, allowing you to work towards your goals while adapting to life changes.

Navigating Goal Achievement Across Life Stages

The strategies that help you work towards your goals evolve as your life circumstances change. Research examining motivations and barriers at retirement age reveals that goal-setting approaches must adapt to different life phases. What works for wealth accumulation in your 30s may not align with asset preservation strategies in your 60s.

| Life Stage | Primary Focus | Key Strategies | Common Obstacles |

|---|---|---|---|

| Early Career (20s-30s) | Wealth Building | Maximize growth investments, establish emergency funds | Limited income, competing priorities |

| Mid-Career (40s-50s) | Acceleration | Increase contribution rates, diversify holdings | Family expenses, lifestyle inflation |

| Pre-Retirement (55-65) | Transition Planning | Risk adjustment, income strategy development | Market volatility concerns, healthcare costs |

| Retirement (65+) | Preservation & Distribution | Tax-efficient withdrawals, estate considerations | Longevity risk, legacy planning |

Understanding these phase-specific considerations allows you to set realistic expectations and choose appropriate strategies. Professional financial advisors help clients navigate these transitions by adjusting plans as circumstances evolve while maintaining focus on ultimate objectives.

Addressing Psychological Barriers

Even well-designed plans encounter psychological resistance. When individuals work towards your goals, they often face internal obstacles that have little to do with financial resources. Fear of market downturns, anxiety about making wrong decisions, or concerns about outliving assets can paralyze action.

Research on goal-setting for individuals experiencing anxiety emphasizes the importance of supportive relationships in overcoming these barriers. In financial contexts, this translates to the value of working with trusted advisors who provide both technical expertise and emotional support during uncertain times.

Leveraging Technology and Tracking Systems

Modern tools provide unprecedented capability to monitor progress and adjust strategies. When you work towards your goals using technology-enhanced systems, you gain real-time visibility into your financial position and can make data-informed decisions. However, research on self-tracking technologies suggests that effective implementation requires personalization and inclusive design.

Digital Tools That Support Goal Progress

Financial technology platforms offer various capabilities that support goal achievement:

- Automated contribution systems that remove friction from saving and investing

- Portfolio tracking dashboards that provide transparency into asset allocation and performance

- Scenario modeling tools that illustrate potential outcomes under different conditions

- Alert systems that notify you of important milestones or required actions

- Communication platforms that facilitate regular contact with advisory teams

The key lies in selecting tools that match your preferences and circumstances. Some individuals thrive with detailed daily tracking, while others prefer quarterly reviews. Fiduciary planning emphasizes personalization, ensuring that tracking systems support rather than overwhelm clients.

Balancing Automation and Engagement

Technology should enhance rather than replace human judgment. While automated investment platforms and robo-advisors offer efficiency, they may not address the nuanced decisions that arise during major life transitions. The most effective approach often combines technological efficiency for routine tasks with professional guidance for complex decisions.

When you work towards your goals using hybrid systems, you benefit from both consistency and adaptability. Automated contributions ensure regular progress, while periodic advisor consultations provide strategic adjustments based on changing circumstances or new opportunities.

Developing Long-Term Persistence and Grit

Short-term motivation proves relatively easy to generate. The greater challenge involves maintaining commitment across years or decades. The personality trait researchers call grit encompasses both perseverance and sustained passion for long-term objectives. This quality proves particularly relevant for financial goals that unfold over extended time horizons.

Individuals who successfully work towards your goals over long periods share certain characteristics. They view setbacks as temporary obstacles rather than permanent failures. They maintain focus on ultimate objectives even when immediate progress seems slow. They demonstrate willingness to adjust tactics while remaining committed to core goals.

Cultivating Resilience Through Market Cycles

Financial markets present both opportunities and challenges. Bull markets create wealth but may encourage complacency. Bear markets test commitment but offer accumulation opportunities. The ability to maintain steady progress regardless of market conditions separates successful wealth builders from those who abandon plans during volatility.

Strategies for maintaining commitment during market downturns:

- Focus on controllable factors like contribution rates and asset allocation

- Review historical data showing recovery patterns after previous downturns

- Reframe volatility as opportunity for dollar-cost averaging benefits

- Maintain regular communication with advisors who provide perspective

- Avoid excessive portfolio monitoring that amplifies emotional responses

These practices help you work towards your goals with consistency, reducing the tendency toward reactive decisions that undermine long-term plans. Estate planning and other long-horizon objectives particularly benefit from this steady approach.

Integrating Professional Guidance Into Your Strategy

While self-directed planning works for some individuals, most benefit from professional expertise. Financial advisors bring technical knowledge, experience across diverse client situations, and objective perspective that proves difficult to maintain independently. When you work towards your goals with professional support, you gain access to sophisticated strategies and avoid common pitfalls.

The Fiduciary Advantage

Working with fiduciary advisors ensures that recommendations prioritize your interests above all other considerations. This legal and ethical standard eliminates conflicts that arise when advisors benefit from selling particular products. The fiduciary relationship creates alignment between your success and your advisor's professional obligations.

Professional guidance provides several distinct advantages:

| Benefit Category | Specific Value | Impact on Goal Achievement |

|---|---|---|

| Technical Expertise | Tax strategy optimization, complex investment vehicles | Improved after-tax returns, efficient wealth transfer |

| Behavioral Coaching | Emotional support during volatility, accountability systems | Reduced reactive decisions, sustained commitment |

| Comprehensive Planning | Integration across retirement, estate, tax domains | Coordinated strategies, fewer conflicts between objectives |

| Time Efficiency | Delegation of research, monitoring, administrative tasks | Increased focus on personal priorities and career |

These advantages compound over time. Small improvements in tax efficiency or risk management accumulate into significant differences over multi-decade time horizons. The guidance you receive helps you work towards your goals more efficiently than purely self-directed approaches.

Adjusting Goals and Strategies as Circumstances Change

Rigid adherence to outdated plans creates unnecessary stress and suboptimal outcomes. Life presents unexpected opportunities and challenges that may require goal modification. Job changes, health issues, inheritance, divorce, or other significant events often necessitate strategy adjustments. The ability to adapt while maintaining core objectives distinguishes effective planning from inflexible systems.

Regular review cycles built into your planning process create natural opportunities for adjustment. Annual or semi-annual meetings with financial advisors provide structured forums for reassessing assumptions, updating projections, and modifying tactics. These reviews ensure that you continue to work towards your goals even as the specific path forward evolves.

When to Revise Versus When to Persist

Distinguishing between necessary adjustments and counterproductive abandonment requires judgment. Some modifications represent prudent responses to changed circumstances. Others reflect temporary frustration or market noise that passes quickly. Consider these factors when evaluating potential changes:

Signals that suggest revision:

- Fundamental changes in income, expenses, or family structure

- Major shifts in tax law or regulatory environment

- Significant changes in health status affecting longevity projections

- Achievement or abandonment of prerequisites for current strategy

Situations requiring persistence:

- Temporary market volatility without fundamental changes

- Short-term emotional responses to news or events

- Impatience with normal timeline for wealth accumulation

- Comparison anxiety triggered by others' apparent success

Professional advisors help clients distinguish between these scenarios, providing perspective that proves difficult to maintain independently. Their experience with diverse client situations creates pattern recognition that informs better decision-making about when to adjust and when to stay the course.

Measuring Progress and Celebrating Milestones

Tracking advancement toward objectives provides both motivation and early warning of potential problems. When you work towards your goals with measurement systems in place, you gain visibility that supports timely adjustments. Effective tracking balances detail with simplicity, providing sufficient information without creating overwhelming complexity.

Defining Meaningful Metrics

Not all measurements prove equally valuable. Focus on indicators that directly reflect progress toward ultimate objectives rather than vanity metrics that provide little actionable insight. For retirement planning, net worth growth matters more than individual account balances. For estate planning, comprehensive documentation completion indicates more than asset values alone.

High-value tracking metrics:

- Net worth trajectory relative to retirement income needs

- Savings rate as percentage of income

- Asset allocation alignment with risk tolerance and timeline

- Tax efficiency of investment and withdrawal strategies

- Estate planning document currency and completeness

These metrics connect directly to goal achievement and highlight areas requiring attention. Regular monitoring helps you work towards your goals with confidence, knowing whether current trajectory aligns with desired outcomes.

The Importance of Milestone Recognition

Long-term objectives can feel abstract and distant. Breaking them into intermediate milestones creates more frequent success experiences that sustain motivation. Reaching your first $100,000 in retirement savings, achieving target savings rate, or completing estate planning documents represents meaningful progress worthy of acknowledgment.

Recognition doesn't require elaborate celebration, but conscious acknowledgment of progress reinforces positive behaviors. Research on goal achievement demonstrates that people who recognize milestones maintain higher motivation levels than those who focus exclusively on distant end goals.

Building Accountability Systems That Work

External accountability significantly increases goal achievement rates. When you commit to specific actions and report progress to others, you create social pressure that reinforces commitment. This principle applies equally to fitness goals, professional objectives, and financial planning.

Accountability takes various forms in financial contexts. Regular meetings with advisors create structured check-in points. Automated reporting systems provide transparency. Some clients benefit from sharing goals with spouses or family members who provide support and gentle pressure. The specific mechanism matters less than consistent implementation.

Structuring Effective Review Cycles

Frequency and format of accountability check-ins should match goal characteristics and personal preferences. Retirement planning typically benefits from quarterly or semi-annual reviews. Tax strategy may require annual adjustments aligned with filing deadlines. Estate planning often involves less frequent reviews unless major life changes occur.

When you work towards your goals with structured accountability, you benefit from external momentum during periods when internal motivation wanes. This system proves particularly valuable during challenging market conditions or when competing priorities threaten to derail financial plans.

Professional advisory relationships through firms like Brookwood Investment Group formalize accountability through regular communication schedules, progress reports, and structured planning reviews. This professional framework ensures that accountability systems remain active even during busy life periods when self-directed discipline might falter.

Successfully achieving financial objectives requires more than good intentions. The combination of clear goal definition, structured implementation planning, appropriate technology tools, professional guidance, and consistent accountability creates conditions for long-term success. Whether you're planning for retirement, managing complex estates, or building generational wealth, these principles provide the foundation for sustained progress. Brookwood Investment Group specializes in helping clients develop and maintain personalized strategies aligned with their unique objectives and circumstances. Connect with our team to explore how fiduciary guidance can support your journey toward financial independence and security.