Understanding how to generate tax-free income can be a transformative element of your financial strategy. While most Americans focus solely on earning more, sophisticated investors recognize that what you keep after taxes matters more than what you earn. Tax-free income represents dollars that never appear on your tax return as taxable earnings, allowing you to build wealth more efficiently over time. This comprehensive guide explores legitimate strategies to incorporate tax-advantaged income into your financial plan while maintaining full compliance with IRS regulations.

Understanding the Foundation of Tax-Free Income

The concept of tax-free income is often misunderstood. Many people confuse tax-deferred income with truly tax-free income, but these are fundamentally different strategies. Tax-deferred accounts like traditional IRAs postpone taxes until withdrawal, while tax-free income generates returns that the IRS never taxes.

According to the IRS guidelines on taxable income, specific income types receive special treatment under federal tax law. These provisions exist to encourage behaviors that benefit society, such as saving for retirement, paying for education, or investing in municipal infrastructure.

Key characteristics of legitimate tax-free income sources:

- Income that never appears as taxable on your return

- Compliance with specific IRS requirements and contribution limits

- Often involves strategic planning years in advance

- Typically requires proper account registration and documentation

- May have income limitations or phase-outs

The difference between earning $100,000 in taxable income versus tax-free income can represent $20,000 to $37,000 in federal taxes alone, depending on your bracket. For high-income professionals, this difference compounds dramatically over decades.

Roth Retirement Accounts: The Foundation of Tax-Free Retirement

Roth IRAs and Roth 401(k)s represent the cornerstone of most tax-free income strategies. These accounts accept after-tax contributions today in exchange for completely tax-free withdrawals in retirement, including all earnings and growth.

Standard Roth IRA Contributions

For 2026, individuals can contribute up to $7,000 annually to a Roth IRA, with an additional $1,000 catch-up contribution for those aged 50 and older. However, income limits apply: single filers with modified adjusted gross income above $161,000 face reduced contribution limits, with complete phase-out at $176,000.

The power of Roth accounts lies in decades of tax-free compounding. A 35-year-old contributing the maximum for 30 years with average market returns could accumulate over $600,000 in completely tax-free retirement funds.

Mega Backdoor Roth Strategy

High-income earners often exceed Roth IRA income limits, but the mega backdoor Roth strategy provides an alternative path. This approach allows after-tax 401(k) contributions beyond the standard $23,500 limit (2026), potentially reaching the total contribution limit of $70,000 through employer contributions and after-tax additions.

This strategy requires:

- An employer 401(k) plan that permits after-tax contributions

- In-service distributions or in-plan Roth conversions

- Careful coordination with your plan administrator

- Proper tax reporting on Form 8606

Not all employers offer this capability, making it essential to review your specific plan documents or consult with financial planning professionals who can evaluate your situation.

Municipal Bonds: Tax-Exempt Interest Income

Municipal bonds issued by state and local governments offer interest payments that are generally exempt from federal income tax. For residents of the issuing state, interest may also be exempt from state and local taxes, creating triple tax-free income.

| Bond Type | Federal Tax | State Tax | Best For |

|---|---|---|---|

| In-State Municipal | Exempt | Exempt | High state tax residents |

| Out-of-State Municipal | Exempt | Taxable | Lower tax states |

| Taxable Bond | Taxable | Taxable | Tax-advantaged accounts |

The true value of municipal bonds depends on your tax bracket. A municipal bond yielding 3.5% provides an equivalent taxable yield of 5.4% for someone in the 35% federal tax bracket. Tax-advantaged income strategies often incorporate municipal bonds as core holdings for generating steady, tax-free cash flow.

Evaluating Municipal Bond Opportunities

Before investing in municipal bonds, consider these factors:

- Credit quality: Not all municipalities have equal financial strength

- Duration risk: Longer-term bonds face greater interest rate sensitivity

- Call provisions: Many municipal bonds can be redeemed early

- Tax-equivalent yield: Calculate the true after-tax benefit for your bracket

Individual bonds provide predictable income and return of principal at maturity, while municipal bond funds offer diversification but introduce price volatility.

Health Savings Accounts: The Triple Tax Advantage

Health Savings Accounts (HSAs) offer perhaps the most powerful tax-free income opportunity available. These accounts provide three distinct tax benefits that no other account can match: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For 2026, contribution limits are $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution for those 55 and older. Forbes financial strategies frequently highlight HSAs as underutilized tools for retirement planning.

Advanced HSA strategy:

- Pay current medical expenses out-of-pocket

- Save receipts for future reimbursement

- Invest HSA funds for long-term growth

- Reimburse yourself years later, tax-free

- After age 65, use for any purpose (taxed like traditional IRA if not medical)

Many people treat HSAs as mere spending accounts, but sophisticated investors recognize them as retirement savings vehicles. A 40-year-old maximizing family HSA contributions for 25 years could accumulate over $400,000 in tax-free medical expense coverage.

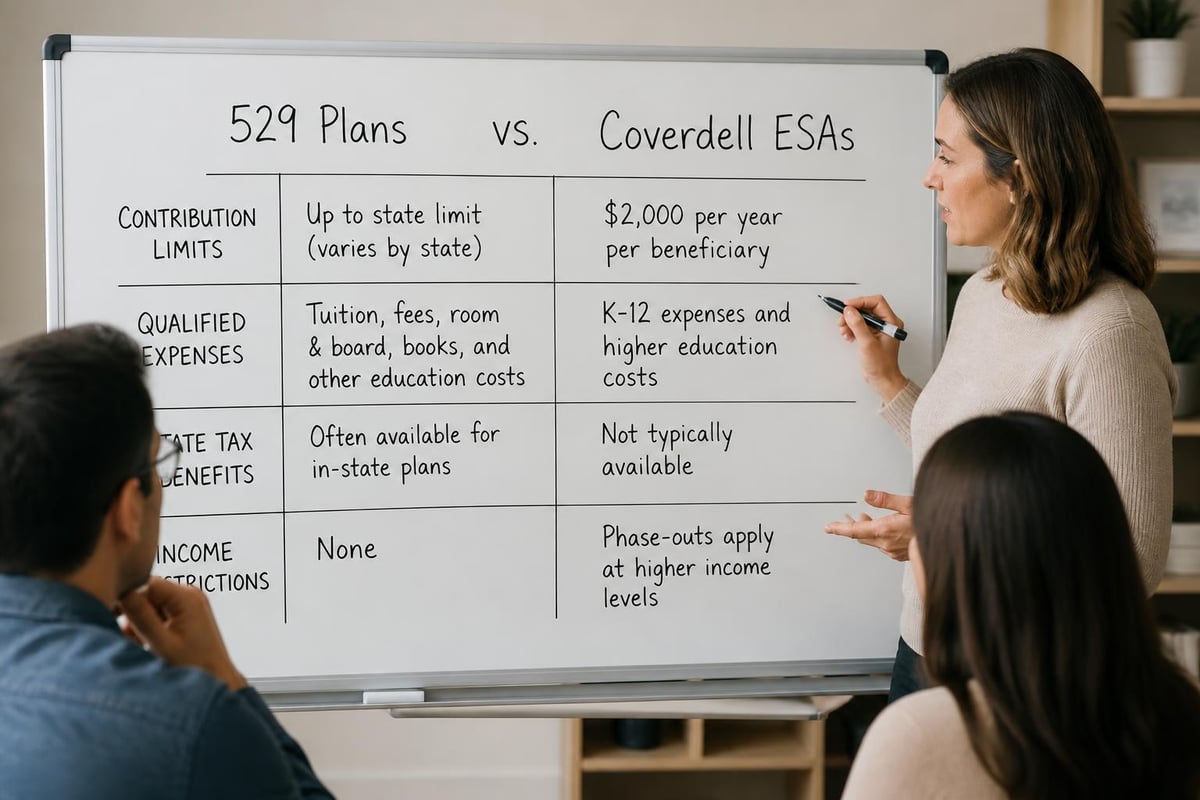

Qualified Education Savings: 529 Plans and Coverdell ESAs

Education savings accounts provide tax-free growth and withdrawals when used for qualified education expenses. These accounts won't generate retirement income, but they free up other assets by covering education costs without tax consequences.

529 College Savings Plans

State-sponsored 529 plans accept after-tax contributions that grow tax-free and distribute tax-free for qualified education expenses. Many states offer additional state tax deductions for contributions, enhancing the tax benefit.

Recent legislative changes expanded 529 plan flexibility:

- K-12 private school tuition ($10,000 annually)

- Apprenticeship programs

- Student loan repayment (up to $10,000 lifetime)

- Roth IRA rollovers (starting in 2024, subject to specific requirements)

Coverdell Education Savings Accounts

Coverdell ESAs allow $2,000 annual contributions per beneficiary with tax-free growth and distributions for qualified education expenses from elementary school through college. Income phase-outs begin at $95,000 for single filers in 2026.

Life Insurance as a Tax-Free Income Vehicle

Permanent life insurance policies can generate tax-free income through policy loans and withdrawals, though this strategy requires careful structuring and comes with important limitations.

Cash value life insurance mechanics:

- Pay premiums into permanent life insurance policy

- Cash value grows tax-deferred within the policy

- Borrow against cash value without creating taxable events

- Death benefit repays loans and passes tax-free to beneficiaries

This approach works best for high-income individuals who have maximized other tax-advantaged accounts. The strategy requires substantial, sustained premium payments and typically makes sense only for those maintaining coverage for decades.

Critical considerations include:

- High internal costs reduce net returns compared to other investments

- Policy lapses with outstanding loans create taxable income

- Requires death benefit to remain in force for optimal results

- Complex products requiring thorough understanding before purchase

Life insurance can play a role in comprehensive estate planning strategies, but it should complement rather than replace traditional retirement accounts.

Real Estate Investment Opportunities

Real estate offers multiple paths to tax-advantaged income, though few provide completely tax-free returns. The primary residence exclusion and Qualified Opportunity Zones represent the clearest tax-free real estate strategies.

Primary Residence Capital Gains Exclusion

Single homeowners can exclude up to $250,000 in capital gains ($500,000 for married couples) when selling their primary residence, provided they've owned and lived in the home for at least two of the past five years. This exclusion can be used repeatedly throughout your lifetime.

Strategic homeowners have used this provision to generate significant tax-free income by:

- Purchasing homes in appreciating markets

- Living in the property while improving it

- Selling after meeting the residency requirement

- Repeating the process with another property

Qualified Opportunity Zones

Qualified Opportunity Zones allow investors to defer and potentially eliminate capital gains taxes by investing in designated economically distressed communities. Gains from any source can be reinvested into Qualified Opportunity Funds within 180 days.

The tax benefits include:

- Temporary deferral of original capital gains until 2026

- Permanent exclusion of Opportunity Zone appreciation if held 10+ years

- No contribution limits like Roth accounts

- Potential for significant tax-free appreciation

This strategy suits investors with substantial capital gains seeking long-term growth opportunities while supporting community development.

Additional Sources of Tax-Free Income

Beyond the major strategies outlined above, several types of nontaxable income exist that may apply to your situation:

| Income Source | Tax Treatment | Considerations |

|---|---|---|

| Child support payments | Tax-free to recipient | Not deductible by payer |

| Life insurance death benefits | Generally tax-free | Exceptions for transferred policies |

| Gifts and inheritances | No income tax | May face estate/gift tax |

| Qualified scholarships | Tax-free for tuition/fees | Room and board is taxable |

| Accident and disability insurance | Often tax-free | Depends on premium payment source |

Understanding which income sources escape taxation can help you make informed decisions about compensation structures, insurance coverage, and financial planning approaches.

Implementing a Tax-Free Income Strategy

Creating an effective tax-free income plan requires coordinating multiple strategies based on your specific circumstances. The most successful approaches typically combine several methods rather than relying on a single tactic.

Step-by-step implementation framework:

- Assess current tax situation: Determine your effective tax rate and identify opportunities

- Maximize employer-sponsored accounts: Contribute to Roth 401(k) options if available

- Fund Health Savings Accounts: Treat HSA as a retirement vehicle, not just medical spending

- Evaluate Roth conversions: Consider converting traditional IRA funds during lower-income years

- Incorporate municipal bonds: Add tax-exempt fixed income appropriate to your risk tolerance

- Plan education funding: Establish 529 plans early to maximize tax-free compounding

- Review annually: Tax laws change, requiring periodic strategy adjustments

The tax planning services offered by fiduciary advisors can help you navigate the complexity of coordinating these strategies while ensuring compliance with current regulations.

Common Mistakes to Avoid

Even sophisticated investors make errors when pursuing tax-free income. Understanding these pitfalls can help you avoid costly mistakes.

Frequent planning errors:

- Focusing exclusively on tax minimization while ignoring overall returns

- Failing to account for required minimum distributions in traditional accounts

- Not coordinating tax-free strategies with Social Security timing

- Overlooking state tax implications of various strategies

- Implementing life insurance policies without understanding costs and complexity

- Missing income limits and contribution deadlines for Roth accounts

NerdWallet’s comprehensive guide to tax-free income sources provides additional context on avoiding common misconceptions about what qualifies as truly tax-free.

Tax Law Changes and Future Considerations

Tax legislation constantly evolves, affecting the viability of various tax-free income strategies. The Tax Cuts and Jobs Act provisions that reduced individual tax rates are scheduled to sunset after 2025, potentially increasing the value of tax-free income sources.

Proposed legislative changes to monitor include:

- Potential modifications to Roth conversion rules

- Changes to estate tax exemptions affecting inherited Roth accounts

- State-level tax law modifications impacting municipal bond benefits

- Adjustments to HSA contribution limits and qualified expenses

Staying informed about tax law developments helps you adapt your strategy before changes take effect. Working with professionals who specialize in retirement and tax planning ensures your approach remains optimized as regulations evolve.

Coordination with Overall Financial Planning

Tax-free income strategies should integrate seamlessly with your broader financial objectives rather than existing in isolation. The most effective plans balance tax efficiency with liquidity needs, risk management, and long-term goals.

Consider how tax-free income sources fit within:

- Retirement income planning: Coordinating taxable, tax-deferred, and tax-free withdrawals

- Legacy objectives: Maximizing after-tax wealth transfer to beneficiaries

- Charitable giving: Balancing tax-free growth with philanthropic goals

- Business succession: Structuring exits to minimize tax impact

The complexity of coordinating these elements highlights the value of comprehensive financial planning services that address your complete financial picture rather than isolated strategies.

Tax-free income strategies offer powerful opportunities to build wealth more efficiently, but they require careful planning, proper execution, and ongoing management to maximize benefits. The most effective approaches coordinate multiple strategies tailored to your specific tax situation, income level, and long-term objectives. Brookwood Investment Group provides personalized guidance on implementing tax-efficient strategies as part of comprehensive financial planning, helping you navigate the complexity of tax-advantaged investing while ensuring your approach aligns with your unique goals and circumstances.