Changing jobs or retiring often brings important decisions about your retirement savings. If you have accumulated funds in an employer-sponsored 401(k), you may be considering your options for managing those assets. One of the most popular choices involves executing a direct rollover 401k to ira, a strategy that allows you to maintain tax-deferred status while potentially gaining access to broader investment opportunities and more personalized financial management. Understanding the mechanics, benefits, and considerations of this process can help you make informed decisions that align with your long-term financial goals.

Understanding the Direct Rollover Process

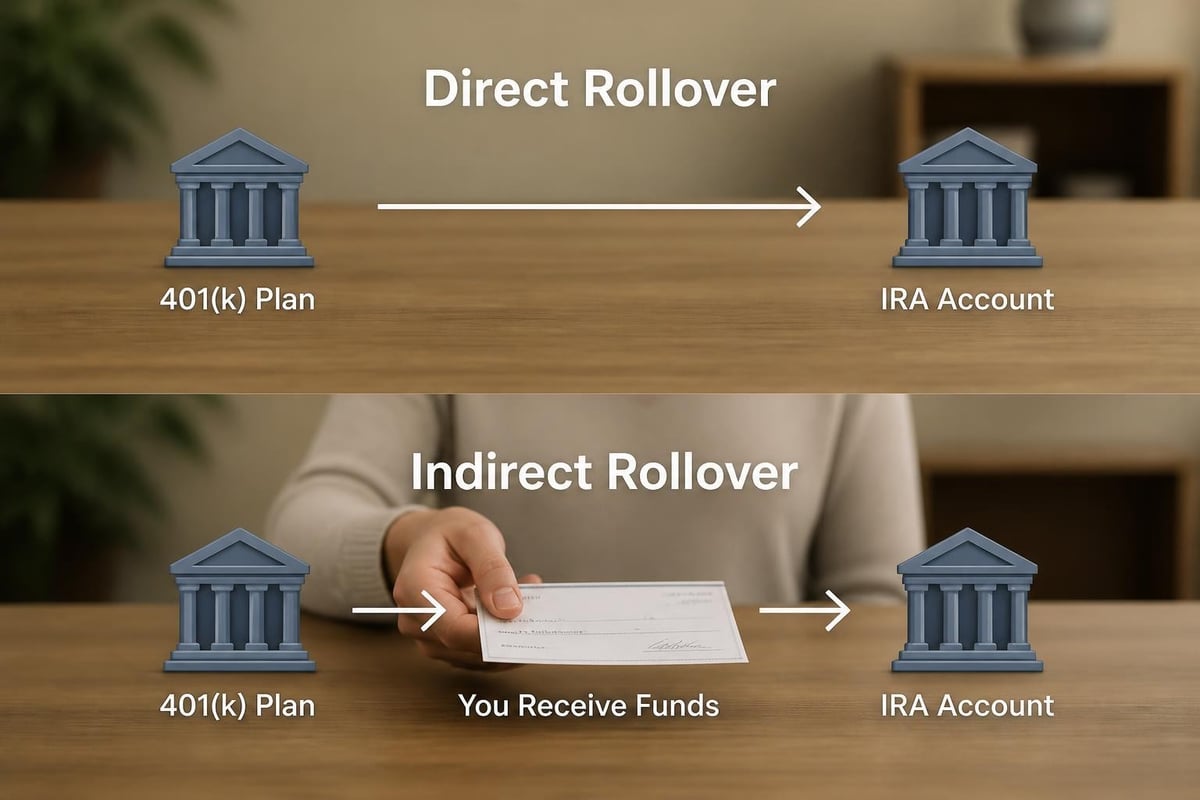

A direct rollover 401k to ira represents a specific method of transferring retirement funds from your employer-sponsored plan to an individual retirement account. This approach differs significantly from indirect rollovers in both execution and tax implications.

What Makes It "Direct"

In a direct rollover, the funds move directly from your 401(k) plan administrator to your IRA custodian without you ever taking possession of the money. The check is typically made payable to the receiving financial institution for your benefit, or the transfer occurs electronically between institutions.

This distinction matters tremendously for tax purposes. When you execute a direct rollover 401k to ira, the IRS does not consider the transaction a taxable distribution. You avoid mandatory withholding, maintain the tax-deferred status of your retirement savings, and eliminate the risk of penalties that can arise with indirect rollovers.

Key advantages of the direct method include:

- No 20% mandatory withholding requirement

- No 60-day deadline to complete the transfer

- Reduced paperwork and administrative burden

- Lower risk of tax complications or penalties

Indirect Rollover Risks

By contrast, an indirect rollover involves the funds being distributed to you personally. Understanding IRA rollover rules becomes critical in these situations because you face a 60-day window to deposit the funds into your IRA. Miss that deadline, and the distribution becomes taxable income, potentially subject to early withdrawal penalties if you are under age 59½.

Step-by-Step Guide to Execute Your Rollover

Completing a direct rollover 401k to ira requires coordination between multiple parties, but the process follows a predictable sequence when properly managed.

Phase One: Preparation and Decision-Making

Before initiating any transfer, you need to determine which type of IRA best suits your circumstances. Traditional IRAs accept pre-tax 401(k) funds without triggering immediate taxation, maintaining the same tax treatment you enjoyed in your employer plan. Roth IRAs offer tax-free growth and distributions but require paying taxes on the converted amount upfront.

Evaluate these factors when choosing:

- Your current tax bracket versus expected retirement tax bracket

- Your timeline to retirement and expected income needs

- Estate planning considerations for your beneficiaries

- Required minimum distribution (RMD) preferences

Working with fiduciary advisory services can provide personalized guidance based on your complete financial picture, including tax strategies and long-term planning objectives.

Phase Two: Account Opening

Select an IRA provider that aligns with your investment preferences, fee structure, and service expectations. Different custodians offer varying levels of investment options, from basic mutual fund platforms to full-service brokerages with stocks, bonds, ETFs, and alternative investments.

Once you choose your provider, complete the IRA application process. Most financial institutions now offer streamlined online applications that take 15-30 minutes to complete. You will need personal information, beneficiary designations, and your 401(k) account details.

Phase Three: Initiating the Rollover

Contact your 401(k) plan administrator to request rollover paperwork. Many employers provide online portals where you can initiate this request electronically, while others require physical forms. The administrator needs specific information about your receiving IRA, including the financial institution name, your account number, and the account registration.

Specify that you want a direct rollover on all documentation. This language matters. Some forms may ask whether you want a "trustee-to-trustee transfer" or "direct rollover," which are essentially the same thing for these purposes.

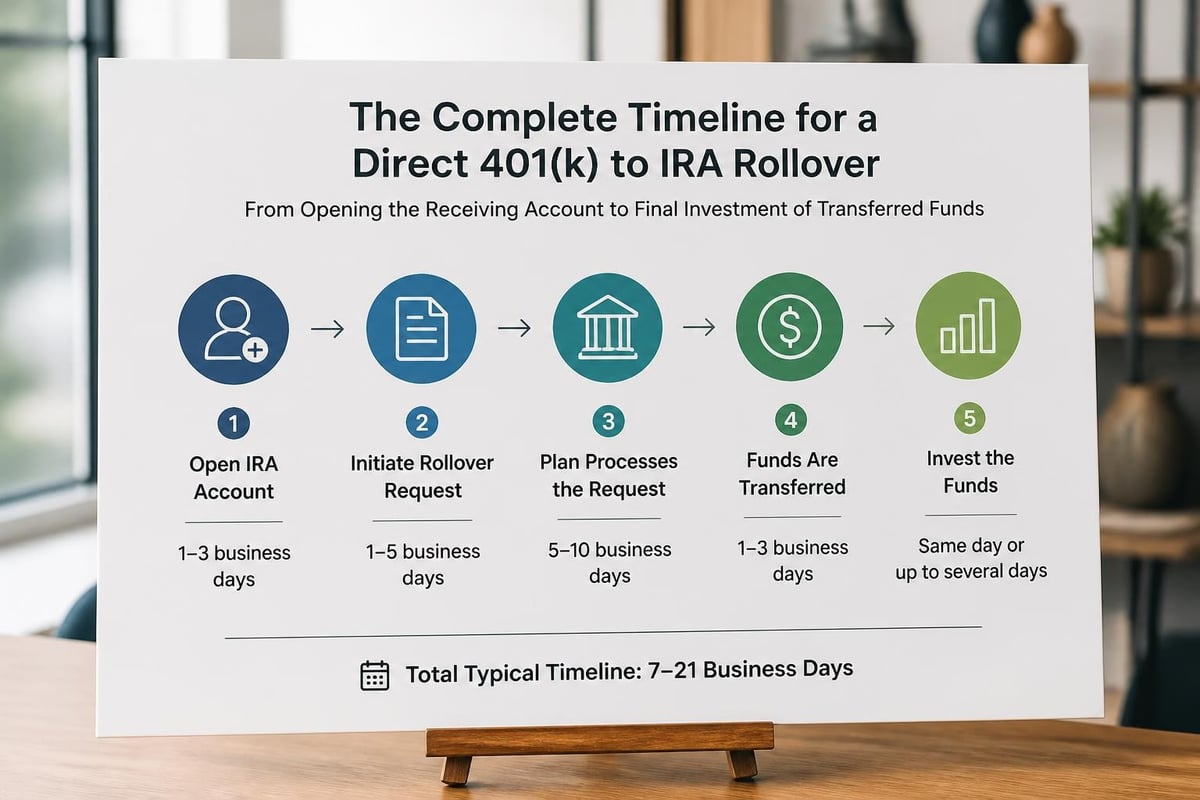

| Rollover Step | Timeline | Key Action |

|---|---|---|

| Open IRA | 1-3 days | Complete application with chosen custodian |

| Request rollover | Same day | Contact 401(k) administrator |

| Processing | 2-6 weeks | Plan administrator processes request |

| Fund transfer | 3-10 days | Money moves between institutions |

| Investment | Immediate | Deploy funds according to strategy |

Phase Four: Following Through

After submitting your request, the 401(k) plan administrator reviews the paperwork and processes the distribution. Processing times vary by administrator, ranging from a few days to several weeks. During this period, your funds remain invested in your 401(k) unless you specifically request liquidation.

Once the funds arrive in your IRA, they typically sit in a money market or settlement account until you provide investment instructions. Guidance on how to roll over a 401(k emphasizes the importance of having an investment strategy ready before the transfer completes to avoid prolonged periods in cash positions.

Comparing Investment Options and Flexibility

One primary motivation for executing a direct rollover 401k to ira involves the expanded investment universe available in individual retirement accounts compared to employer-sponsored plans.

401(k) Plan Limitations

Employer-sponsored retirement plans typically offer 15-30 investment options, primarily consisting of mutual funds selected by the plan administrator or third-party consultant. While these options often include target-date funds, index funds, and actively managed mutual funds across various asset classes, you remain limited to the specific menu your employer provides.

Some 401(k) plans also restrict certain investment strategies, such as frequent trading or holding concentrated positions in individual securities. These limitations exist partly to reduce fiduciary liability for plan sponsors and partly to simplify administration.

IRA Advantages

Individual retirement accounts remove most of these restrictions. Within an IRA, you can typically access:

- Individual stocks and bonds

- Exchange-traded funds (ETFs) across all asset classes

- Mutual funds from hundreds of fund families

- Real estate investment trusts (REITs)

- Certificates of deposit (CDs)

- Precious metals (in certain IRA types)

- Alternative investments through self-directed IRAs

This flexibility allows for more sophisticated portfolio construction aligned with your specific risk tolerance, time horizon, and financial objectives. Understanding the benefits of rolling over a 401(k) helps illustrate how investment flexibility can translate into potential cost savings and improved portfolio customization.

Tax Considerations and Strategic Planning

Tax implications represent a critical consideration when planning a direct rollover 401k to ira, particularly when deciding between traditional and Roth IRA destinations.

Traditional IRA Rollovers

Rolling pre-tax 401(k) funds into a traditional IRA maintains tax-deferred status. You pay no taxes at the time of transfer, and the money continues growing tax-deferred until you take distributions in retirement. Required minimum distributions begin at age 73 for individuals born in 1960 or later, following recent legislative changes.

This approach makes sense when you expect to be in a similar or lower tax bracket during retirement compared to your current working years. It preserves your tax deferral and avoids triggering a large tax bill during your working years.

Roth Conversion Considerations

Converting 401(k) funds to a Roth IRA during your rollover creates a taxable event. The entire converted amount adds to your ordinary income for that tax year, potentially pushing you into higher tax brackets.

However, factors to consider before rolling into a Roth IRA include the long-term benefits of tax-free growth and distributions. Roth IRAs also avoid required minimum distributions during the original owner's lifetime, providing more flexibility in retirement income planning.

Strategic Roth conversion scenarios include:

- Years with lower-than-normal income (job transitions, sabbaticals)

- Early retirement before Social Security or pension income begins

- Deliberate multi-year conversion strategies to manage tax brackets

- Estate planning to leave tax-free assets to beneficiaries

Working with professionals who understand retirement planning and estate planning helps optimize the timing and amount of conversions to minimize lifetime tax burden.

Cost Analysis and Fee Structures

Executing a direct rollover 401k to ira may reduce your ongoing investment expenses, though results vary based on your specific situation.

401(k) Fee Layers

Employer-sponsored retirement plans often include multiple fee layers that reduce your returns over time. Administrative fees cover recordkeeping, compliance, and communication costs. Investment fees compensate fund managers. Some plans also charge individual service fees for loans, distributions, or special services.

Large employers often negotiate favorable pricing due to their plan size, potentially offering lower-cost institutional share classes unavailable to individual investors. Small and mid-sized company plans may face higher per-participant costs due to limited negotiating power.

IRA Cost Considerations

Individual retirement accounts eliminate administrative fees charged at the plan level but introduce account-level fees from your chosen custodian. Many modern IRA providers now offer commission-free trading on stocks and ETFs, with no annual account maintenance fees for accounts above minimum balances.

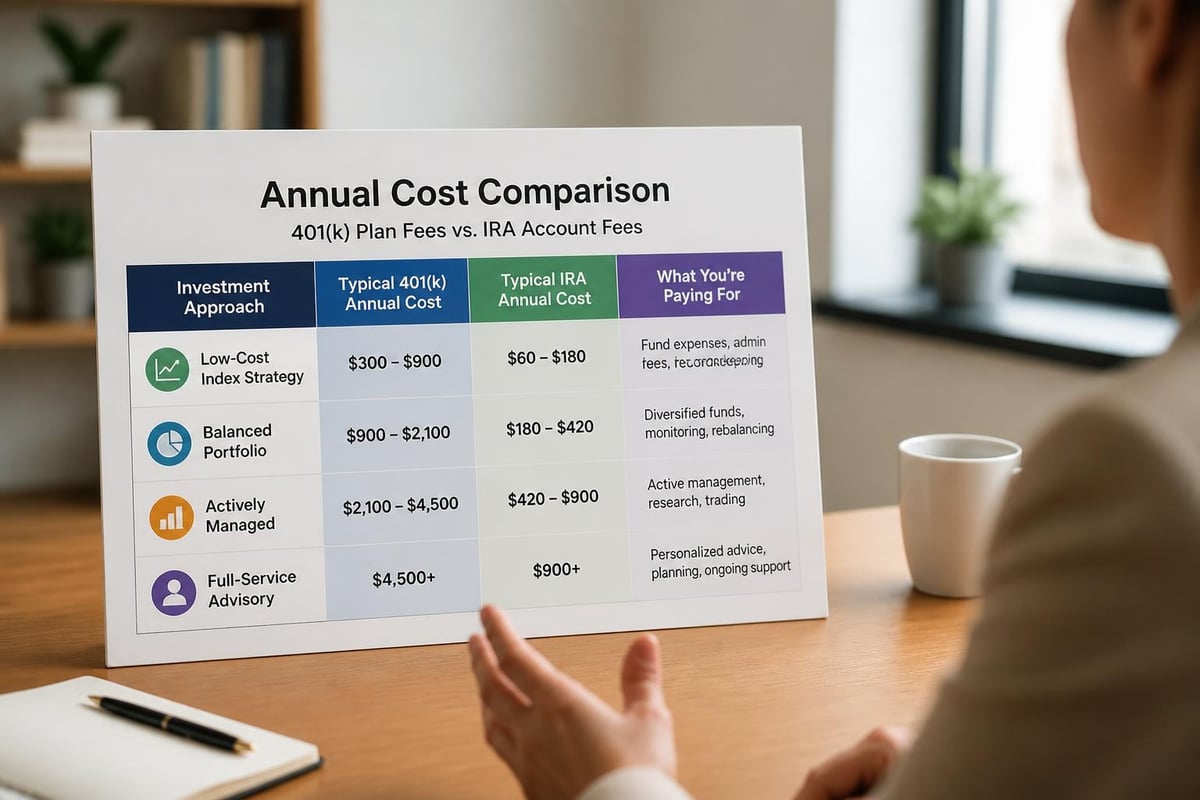

| Cost Category | 401(k) Plans | IRAs |

|---|---|---|

| Administrative fees | $50-$150/year typical | Often $0 with minimum balance |

| Investment expense ratios | 0.50%-1.50% average | 0.03%-1.50% depending on choices |

| Trading commissions | Usually $0 for plan options | Often $0 for stocks/ETFs |

| Advisory fees | Rarely available | 0.25%-1.50% if using advisor |

The key difference lies in control. With an IRA following a direct rollover 401k to ira, you choose your investments and can select low-cost index funds or ETFs if cost minimization is a priority. You also have the option to work with investment management professionals who provide personalized portfolio management and planning services.

Protection and Creditor Considerations

An often-overlooked aspect of the direct rollover 401k to ira decision involves legal protections afforded to retirement accounts under federal and state law.

Federal ERISA Protection

Funds held in 401(k) plans enjoy unlimited protection from creditors under the Employee Retirement Income Security Act (ERISA). This federal law shields employer-sponsored retirement plan assets from bankruptcy proceedings, lawsuits, and creditor claims with very few exceptions.

IRA Protection Levels

Individual retirement accounts receive more limited protection. Federal bankruptcy law protects up to $1,512,350 in traditional and Roth IRA assets (adjusted for inflation in 2026) from creditors in bankruptcy proceedings. Amounts exceeding this threshold may be vulnerable depending on the circumstances.

State law governs IRA creditor protection outside bankruptcy proceedings, creating a patchwork of protection levels across the country. Some states provide unlimited protection for IRA assets, while others offer limited or no protection beyond the federal bankruptcy exemption.

Rollover IRAs containing funds from qualified employer plans receive somewhat stronger protection than contributory IRAs in bankruptcy, maintaining unlimited protection similar to 401(k)s. However, potential risks associated with moving funds to IRAs warrant consideration if you work in a profession with high liability exposure or face significant creditor risks.

Common Mistakes to Avoid

Even straightforward direct rollover 401k to ira transactions can encounter problems when individuals overlook critical details or make preventable errors.

Failing to Specify "Direct"

The most consequential mistake involves not clearly specifying a direct rollover on your distribution request. If the 401(k) administrator sends the check to you personally instead of directly to your IRA custodian, the transaction becomes an indirect rollover with a 60-day deadline and 20% withholding requirement.

Missing Required Documentation

Incomplete paperwork delays the process and sometimes results in abandoned rollovers. Ensure you provide all required documentation to both your 401(k) administrator and your IRA custodian, including:

- Completed distribution request forms with original signatures

- IRA account documentation showing your account number

- Receiving institution's wire or delivery instructions

- Medallion signature guarantees if required for large balances

Rolling Over Company Stock

Employer stock held in your 401(k) may qualify for special tax treatment called net unrealized appreciation (NUA). This strategy allows you to pay long-term capital gains rates on the appreciation rather than ordinary income tax rates, potentially saving substantial taxes on highly appreciated company stock.

Executing a direct rollover 401k to ira eliminates the ability to use this strategy. Consult with tax professionals before rolling over any employer stock to evaluate whether NUA treatment makes sense for your situation.

Forgetting About Outstanding Loans

If you have an outstanding 401(k) loan when you separate from service, the unpaid balance typically becomes due. Failing to repay the loan before executing your rollover results in the outstanding balance being treated as a taxable distribution, potentially with early withdrawal penalties.

Timing Considerations for Your Rollover

When you execute a direct rollover 401k to ira can influence both the complexity of the transaction and the financial outcomes you experience.

During Employment

Most employer plans prohibit in-service distributions before age 59½, meaning you cannot roll over funds while still employed unless you meet specific age or service requirements. Some plans allow in-service rollovers for employees over age 59½ or for funds that have been in the plan for a minimum period.

After Separation from Service

Leaving your employer through retirement, resignation, or termination triggers immediate eligibility for rollover. You face no deadline for completing a direct rollover 401k to ira, allowing you to take time to research options and make thoughtful decisions.

However, maintaining funds in a former employer's plan exposes you to risks including plan termination, changing investment options, or difficulty accessing information after you have moved on to other opportunities.

Optimal timing considerations include:

- Market conditions and whether you want to remain invested during the transfer

- Tax planning opportunities in the current versus future tax years

- Time needed to research and select appropriate IRA investments

- Coordination with other financial planning initiatives

Professional guidance on managing old 401(k) accounts can help you evaluate these factors based on your specific circumstances.

Alternative Options to Consider

While a direct rollover 401k to ira serves many individuals well, other options deserve consideration based on your unique situation.

Leaving Funds in Your Former Employer Plan

If your 401(k) balance exceeds $7,000, most employers allow you to leave funds in their plan indefinitely. This option makes sense when your former employer's plan offers exceptional investment options at institutional pricing, provides valuable features like stable value funds unavailable in IRAs, or when you work in a high-liability profession and value the enhanced creditor protection.

Rolling to a New Employer's Plan

If you have started a new job with an employer offering a 401(k) plan, you can often roll your old 401(k) directly into the new plan. This consolidation simplifies your retirement savings, maintains ERISA creditor protection, and may provide access to institutional investment options or unique plan features.

Combining Multiple Strategies

You are not limited to a single approach. You might roll part of your 401(k) to a traditional IRA, convert another portion to a Roth IRA to manage the tax impact, and leave highly appreciated company stock in the plan for potential NUA treatment. This customized approach requires more coordination but can optimize tax efficiency and investment flexibility.

Documentation and Record Keeping

Proper documentation protects you from potential tax complications and provides clarity when reviewing your financial situation with advisors or preparing tax returns.

Essential Records to Maintain

After completing a direct rollover 401k to ira, retain copies of all documentation for at least seven years. Critical records include the final 401(k) statement before the rollover, documentation showing the direct nature of the transfer, confirmation from your IRA custodian showing the deposit, and Form 1099-R from your 401(k) administrator.

Form 1099-R reports the distribution to the IRS. For a proper direct rollover, box 2a (taxable amount) should show $0, and the distribution code should indicate a direct rollover. Report this on your tax return along with Form 5498 showing the IRA contribution to demonstrate the complete rollover chain.

Coordination with Tax Preparation

Your tax preparer needs specific information about your rollover to properly complete your return. Provide both the 1099-R from the distributing plan and the 5498 from the receiving IRA (though 5498s arrive later and may not be available until after you file). Proper reporting ensures the IRS does not treat the transaction as a taxable distribution.

Working with Financial Professionals

The complexity of retirement account rollovers, combined with the long-term implications of these decisions, often warrants professional guidance tailored to your complete financial picture.

Fiduciary Advisory Value

Fiduciary advisors operate under a legal obligation to act in your best interest, providing advice free from conflicts of interest that might arise from commission-based compensation or proprietary product requirements. This approach aligns particularly well with rollover decisions that can significantly impact your retirement security.

Comprehensive planning considers not just the mechanics of executing a direct rollover 401k to ira, but how this decision integrates with your broader financial strategy, including tax planning, estate considerations, and investment management.

Ongoing Investment Management

After completing your rollover, you face decisions about how to invest the transferred funds. Professional investment management services provide ongoing portfolio oversight, rebalancing, tax-loss harvesting, and adjustments based on changing market conditions or life circumstances.

Virtual-first advisory models now make professional guidance accessible regardless of your location, offering the convenience of digital communication combined with personalized service tailored to your unique goals and lifestyle.

A direct rollover 401k to ira provides tax-efficient access to expanded investment options while maintaining the tax-deferred status of your retirement savings. The process requires attention to detail, but the potential benefits of lower costs, greater investment flexibility, and personalized management can significantly impact your long-term financial security. Whether you are navigating a job transition, approaching retirement, or simply looking to optimize your retirement savings strategy, Brookwood Investment Group LLC offers fiduciary guidance tailored to your unique circumstances, helping you make informed decisions that support your long-term financial goals.