An IRA charitable distribution represents one of the most tax-efficient ways for retirees to support charitable organizations while managing their required minimum distributions. Also known as a qualified charitable distribution (QCD), this strategy allows individuals aged 70½ or older to transfer funds directly from their traditional IRA to a qualified charity, potentially reducing their taxable income while fulfilling their philanthropic goals. As tax regulations continue to evolve and more Americans reach retirement age, understanding the mechanics and benefits of this giving strategy has become increasingly important for comprehensive financial planning.

Understanding the IRA Charitable Distribution Basics

An ira charitable distribution allows IRA owners to make direct transfers from their retirement accounts to eligible charitable organizations. This transaction bypasses the account holder entirely, with funds moving directly from the IRA custodian to the charity. The distribution counts toward the owner's required minimum distribution for the year but doesn't increase adjusted gross income.

Key eligibility requirements include:

- You must be at least 70½ years old when the distribution occurs

- The distribution must come from a traditional IRA (not SEP or SIMPLE IRAs in most cases)

- The receiving organization must be a qualified 501(c)(3) charity

- The maximum annual QCD amount is $105,000 per individual as of 2026

- Funds must transfer directly from the IRA to the charity

The age threshold represents a critical detail that many overlook. Unlike required minimum distributions that now begin at age 73 for most individuals, the qualified charitable distribution option from Fidelity becomes available at the earlier age of 70½. This three-year window creates unique planning opportunities.

Why the Direct Transfer Matters

The direct transfer requirement isn't just administrative paperwork. When you receive an IRA distribution personally and then donate it to charity, you must report the full distribution as income first. You might claim a charitable deduction afterward, but this approach increases your adjusted gross income, potentially triggering higher Medicare premiums or affecting other income-based thresholds.

With an ira charitable distribution, the funds never touch your hands, and the amount doesn't appear as income on your tax return. This distinction makes QCDs particularly valuable for retirees who take the standard deduction rather than itemizing, as they receive tax benefits without needing to itemize charitable contributions.

Tax Benefits and Strategic Advantages

The tax advantages of an ira charitable distribution extend beyond simple income reduction. When properly executed, this strategy can influence multiple aspects of your financial picture, from Medicare costs to state tax obligations.

Income Tax Implications

| Traditional Donation | IRA Charitable Distribution |

|---|---|

| Counts as income first | Never counted as income |

| Requires itemizing to deduct | No itemization needed |

| Subject to AGI limitations | No AGI limitations apply |

| Increases MAGI | Does not increase MAGI |

The modified adjusted gross income (MAGI) impact deserves special attention. Many tax provisions and surcharges use MAGI as their calculation basis. By keeping this number lower through QCDs rather than traditional distributions, you may avoid or reduce several additional costs.

Planning strategies to manage Medicare IRMAA surcharges often incorporate qualified charitable distributions as a key component. Medicare Income-Related Monthly Adjustment Amounts (IRMAA) increase Part B and Part D premiums for individuals whose MAGI exceeds certain thresholds. Because an ira charitable distribution doesn't increase MAGI, it can help you stay below these thresholds.

Satisfying Required Minimum Distributions

Once you reach age 73, the IRS requires you to withdraw a specific amount from your traditional IRA annually. These required minimum distributions (RMDs) are calculated based on your account balance and life expectancy. For those who must take an RMD but don’t need the funds, an ira charitable distribution offers an elegant solution.

The QCD satisfies your RMD requirement without creating taxable income. If your RMD is $20,000 but you only need $12,000 for living expenses, you could take $12,000 as a regular distribution and direct $8,000 to charity as a QCD. This approach meets the IRS requirement while minimizing your tax burden.

Important RMD considerations:

- QCDs can satisfy all or part of your RMD

- You cannot use QCDs to satisfy RMDs from employer plans like 401(k)s

- The QCD must occur by December 31st to count for that tax year

- You cannot carry forward excess QCD amounts to future years

Working with retirement planning professionals can help you determine the optimal balance between regular distributions and charitable transfers based on your income needs and philanthropic objectives.

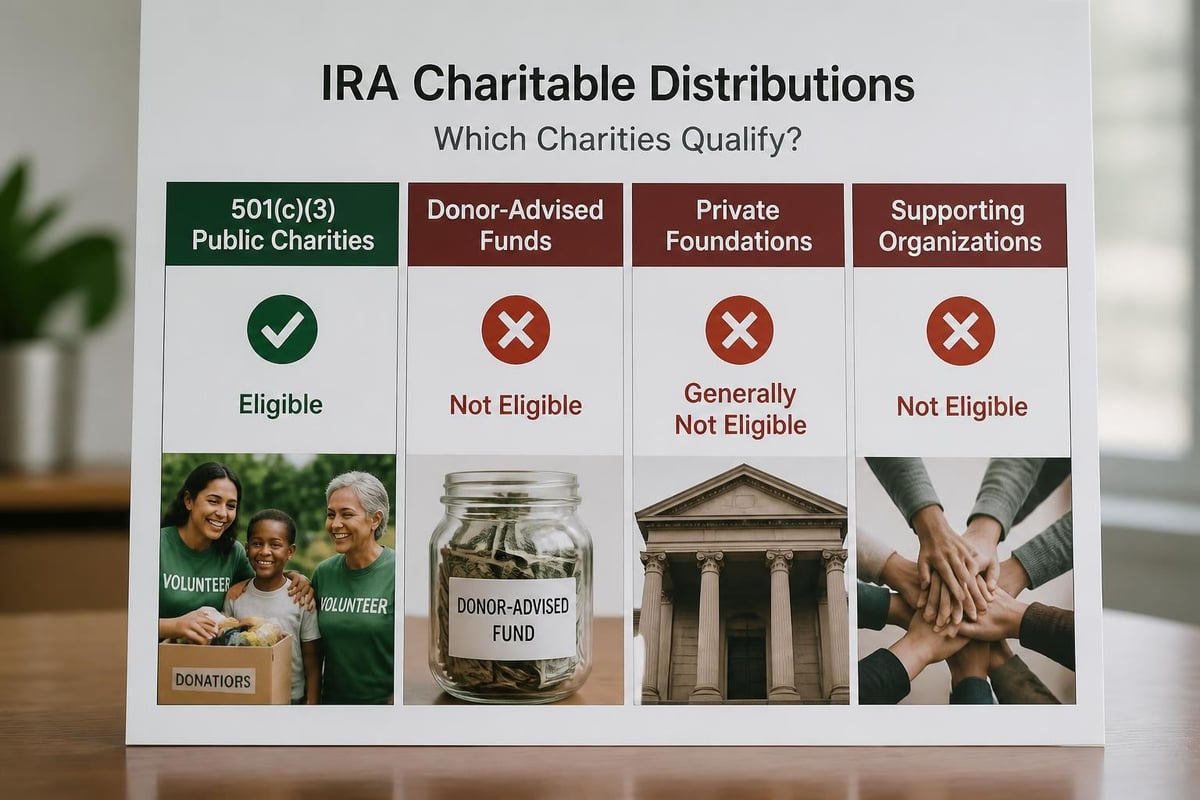

Eligible Charities and Distribution Methods

Not every charitable organization qualifies to receive an ira charitable distribution. The IRS maintains specific requirements that both the charity and the distribution method must meet.

Qualified Organizations

The receiving charity must be a 501(c)(3) organization eligible to receive tax-deductible contributions. However, several types of organizations that normally qualify for charitable deductions don't work for QCDs:

- Donor-advised funds cannot receive QCDs

- Private foundations are generally ineligible

- Supporting organizations don't qualify

- Charitable gift annuities weren't eligible until recent legislative changes

Organizations like the American Heart Association and American Red Cross actively promote their QCD programs, providing streamlined processes for donors who wish to make qualified charitable distributions. These established charities often have dedicated departments to facilitate IRA transfers.

Executing the Distribution

The mechanics of completing an ira charitable distribution require coordination between you, your IRA custodian, and the charity. Most major custodians have established procedures, but the process varies by institution.

Step-by-step distribution process:

- Contact your IRA custodian and request a QCD distribution form

- Provide the charity's legal name, address, and tax identification number

- Specify the exact amount you wish to transfer

- Submit the completed form according to your custodian's requirements

- Request written confirmation from both the custodian and the charity

- Maintain detailed records for tax reporting purposes

Timing matters significantly. IRA custodians may need several weeks to process QCD requests, particularly during the busy year-end period when many people make distributions. Starting the process in early December for a current-year QCD protects against processing delays.

Documentation and Tax Reporting Requirements

Proper documentation transforms an ira charitable distribution from a potential audit risk into a well-supported tax strategy. The IRS requires specific reporting, and maintaining thorough records protects you if questions arise.

What You Need to Keep

Your documentation file should include several key items. The IRA custodian will send you a Form 1099-R showing the total distribution amount. This form won't distinguish between regular distributions and QCDs, reporting the full amount as a distribution from your IRA.

The charity must provide a contemporaneous written acknowledgment for any gift of $250 or more. This acknowledgment should confirm that you received no goods or services in exchange for the contribution. Without this documentation, the IRS could disallow the QCD treatment.

| Document Type | Purpose | Retention Period |

|---|---|---|

| Form 1099-R | Shows total IRA distributions | Permanent |

| Charity acknowledgment letter | Proves gift and amount | Permanent |

| QCD request form | Documents your intent | 7 years minimum |

| Custodian confirmation | Verifies direct transfer | 7 years minimum |

| Tax return with QCD notation | Shows proper reporting | Permanent |

Reporting on Your Tax Return

When you file your tax return, you'll report the ira charitable distribution on the IRA distribution lines of Form 1040. The process requires attention to detail:

Enter the total distribution amount from Form 1099-R on line 4a. On line 4b (taxable amount), enter the total minus your QCD amount. Next to line 4b, write "QCD" to alert the IRS that you're claiming qualified charitable distribution treatment.

Detailed guidance on qualified charitable distribution reporting addresses common questions about this process. Many taxpayers benefit from professional assistance the first year they implement this strategy to ensure proper reporting.

Strategic Planning Considerations

Maximizing the benefits of an ira charitable distribution requires integration with your broader financial strategy. Several planning considerations can enhance the effectiveness of this approach.

Coordinating With Other Charitable Giving

If you regularly support charitable causes, timing and method matter. Consider making your QCDs early in the year to satisfy your RMD requirement, then using other assets for additional giving later. This sequencing allows the QCD to reduce your income immediately while preserving flexibility for responsive giving as opportunities arise.

Some donors maintain a charitable giving budget that combines QCDs with other methods. You might direct $15,000 annually through qualified charitable distributions to your core supported organizations, then donate appreciated securities or cash to address special appeals or new initiatives.

Optimization strategies include:

- Using QCDs for organizations that don't accept securities

- Saving appreciated stock donations for charities with brokerage accounts

- Directing QCDs to smaller organizations that prefer cash

- Maintaining donor recognition through separate cash gifts if desired

Multi-Year Planning Approaches

Looking beyond the current tax year, an ira charitable distribution strategy can evolve as your circumstances change. In years when you have high income from other sources, maximizing your QCD amount (up to $105,000) provides greater tax benefits. In lower-income years, you might reduce QCDs and take more regular distributions if you're in a lower tax bracket.

Some retirees adopt a "QCD-first" approach, automatically directing their first distributions each year to charity until they reach either their desired charitable giving amount or the RMD threshold. This systematic method simplifies decision-making and ensures philanthropic commitments are met before discretionary spending.

Comprehensive estate planning strategies often incorporate QCD planning, particularly when IRA assets represent a significant portion of the estate. Since traditional IRAs create income tax obligations for most non-spouse beneficiaries, using these assets for charitable giving during your lifetime can be more tax-efficient than leaving them in the estate.

Special Situations and Advanced Strategies

Beyond basic ira charitable distribution implementation, several specialized applications deserve consideration based on individual circumstances.

One-Time Gift Election

The SECURE 2.0 Act introduced a one-time option to make a QCD of up to $50,000 (indexed for inflation) to a charitable remainder trust or charitable gift annuity. This election, available starting in 2023, allows more sophisticated planned giving arrangements while maintaining QCD tax benefits.

This one-time provision creates planning opportunities for larger charitable commitments. If you want to establish a charitable gift annuity that provides income for life while ultimately benefiting a charity, you can fund it with a QCD rather than paying income tax on an IRA distribution first.

Inherited IRA Considerations

The rules for QCDs from inherited IRAs follow specific provisions. Spouse beneficiaries who treat an inherited IRA as their own can make qualified charitable distributions once they reach age 70½. Non-spouse beneficiaries generally cannot make QCDs from inherited IRAs, though this area involves complex rules that may require professional guidance.

State Tax Implications

While federal tax benefits drive most ira charitable distribution planning, state tax treatment varies. Most states follow federal tax treatment, excluding QCDs from income. However, some states have different rules or don't recognize QCDs for state tax purposes.

Before implementing a QCD strategy, verify how your state treats these distributions. This consideration particularly matters in states with high income tax rates, where the state tax impact could be substantial.

Common Mistakes to Avoid

Even well-intentioned ira charitable distribution attempts can fail to achieve their intended tax benefits if common pitfalls aren't avoided.

Taking the Distribution First

Perhaps the most frequent error involves receiving the IRA distribution personally, then writing a check to the charity. This sequence fails the direct transfer requirement, forcing you to report the full distribution as income. The subsequent charitable deduction may offset some tax impact if you itemize, but you lose the MAGI reduction and other QCD benefits.

Some custodians issue checks payable to the charity but send them to the account owner for forwarding. While this method can work, it requires the account owner to deliver the check without cashing it themselves, creating both temptation and documentation challenges.

Missing the Age Requirement

The 70½ age threshold catches some donors off guard. If you make an ira charitable distribution before reaching this age, even by a few days, it doesn't qualify for tax-free treatment. The distribution becomes taxable income, and you'll need to itemize deductions to claim any charitable deduction.

Age verification steps:

- Calculate your exact 70½ birthday (six months after your 70th birthday)

- Ensure the distribution date falls after this threshold

- Document your birthdate in your QCD file

- Confirm timing with your tax advisor if you're making distributions near the cutoff

Exceeding the Annual Limit

The $105,000 annual limit applies per individual. Married couples can each make QCDs up to this amount if both have IRAs and meet the age requirement. Exceeding the limit doesn't invalidate the entire QCD, but the excess amount becomes a taxable distribution.

If you're making multiple QCDs throughout the year, maintain a running total to avoid accidentally exceeding the limit. This tracking becomes particularly important when both spouses are making distributions or when you're coordinating QCDs with regular distributions.

Working With Financial Professionals

Given the complexity of ira charitable distribution rules and their interaction with other tax provisions, professional guidance often proves valuable. Financial advisors who specialize in retirement planning can help integrate QCD strategies with your overall financial plan.

A comprehensive approach examines how charitable distributions fit within your income strategy, tax planning, estate planning, and philanthropic goals. Advisors can model different scenarios, showing how various QCD amounts affect your tax situation across multiple years.

Professional guidance typically addresses:

- Optimal annual QCD amounts based on income needs and RMD requirements

- Coordination between QCDs and other charitable giving methods

- Documentation requirements and record-keeping systems

- Integration with estate planning and legacy goals

- State-specific tax considerations

Many retirees find that the personalized financial guidance provided by fiduciary advisors helps them maximize both the tax efficiency and the philanthropic impact of their charitable giving. This comprehensive perspective ensures that ira charitable distribution strategies support rather than conflict with other financial objectives.

Understanding the detailed mechanics of QCD planning from resources like Fidelity Charitable provides a foundation, but applying these concepts to your specific situation requires customized analysis.

Tax professionals also play an important role, particularly during the first year you implement a QCD strategy. They ensure proper reporting on your tax return and can address questions about documentation requirements or state tax treatment.

Making the Most of Your Charitable Impact

Beyond tax considerations, an ira charitable distribution offers opportunities to increase your philanthropic effectiveness. Strategic giving multiplies the impact of your charitable dollars while simplifying your financial life.

Organizations like Samaritan’s Purse and other established charities have developed robust programs to receive QCDs efficiently. Working with organizations that understand the QCD process reduces administrative friction and ensures your gifts are processed correctly.

Developing a Giving Strategy

Rather than making ad hoc charitable decisions, develop a systematic approach to your ira charitable distribution giving. Identify your core philanthropic priorities and align your QCD distributions with these values. This intentionality often leads to greater satisfaction and more significant charitable impact.

Some donors create a multi-year giving plan that specifies which organizations will receive QCD support and in what amounts. This planning allows charities to anticipate your support and may enable you to participate in capital campaigns or special initiatives more effectively.

Building Relationships With Charities

Regular QCD giving creates opportunities to deepen relationships with organizations you support. Many charities offer special recognition or engagement opportunities for consistent donors. These relationships can enhance your understanding of the organization's work and your confidence that your gifts are making a difference.

When you commit to ongoing support through qualified charitable distributions, communicate this intention to the organization. While you're not legally obligated to continue distributions in future years, sharing your plans helps charities with their own strategic planning and budgeting.

An ira charitable distribution combines tax efficiency with philanthropic impact, offering a powerful tool for retirees who want to support causes they care about while managing their required minimum distributions and taxable income. The strategy's benefits extend beyond simple tax savings to include Medicare premium management, estate planning advantages, and enhanced charitable effectiveness. Whether you're just beginning to explore retirement planning options or looking to optimize your existing strategy, Brookwood Investment Group provides personalized guidance tailored to your unique financial situation and charitable goals, helping you navigate the complexities of QCD planning within the context of your comprehensive financial picture.