Understanding the rules and strategies surrounding your retirement accounts can significantly impact your financial future. An IRA distribution represents any withdrawal you make from your Individual Retirement Account, whether traditional or Roth, and each type carries specific tax implications and regulatory requirements. As you approach retirement or face life circumstances requiring access to these funds, knowing how distributions work becomes essential for maintaining your financial health and avoiding unnecessary penalties or tax burdens.

Understanding IRA Distribution Basics

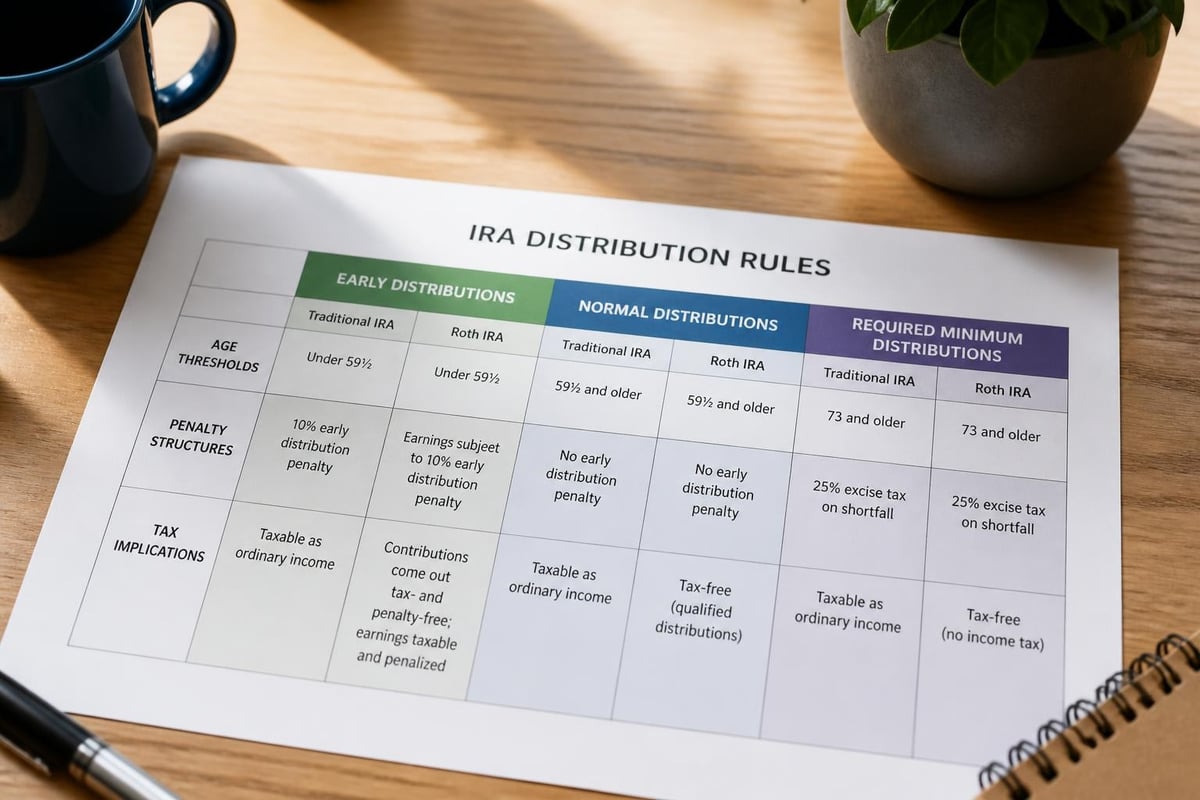

An ira distribution occurs whenever money leaves your Individual Retirement Account, regardless of your age or the reason for withdrawal. These distributions follow strict Internal Revenue Service regulations that dictate when you can take money out, how much you must withdraw after certain ages, and what tax consequences you'll face.

The type of IRA you own determines how your distributions are taxed. Traditional IRA distributions typically count as ordinary income since you received a tax deduction when making contributions. Conversely, Roth IRA distributions may be tax-free if you meet specific criteria regarding age and account holding period.

Tax Treatment of Different Distribution Types

Not all ira distribution events receive the same tax treatment. The IRS distinguishes between several categories that affect your tax liability and potential penalties.

Early distributions occur before you reach age 59½ and generally trigger a 10% additional tax on top of regular income taxes. However, numerous exceptions exist for specific circumstances like disability, first-time home purchases, or qualified education expenses. The IRS provides detailed guidance on distribution exceptions that may apply to your situation.

Normal distributions begin after age 59½ when you can withdraw funds without the early withdrawal penalty. You'll still owe income tax on traditional IRA distributions, but the additional 10% penalty no longer applies.

Required Minimum Distributions (RMDs) represent mandatory withdrawals that begin at age 73 for those born in 1951 or later. These distributions ensure the government eventually collects tax revenue on tax-deferred retirement accounts.

Required Minimum Distributions Explained

Once you reach age 73, the IRS mandates you begin taking annual distributions from traditional IRAs. This requirement ensures tax-deferred accounts don't remain untouched indefinitely, allowing the government to collect taxes on funds that grew tax-free for decades.

The calculation for your ira distribution under RMD rules involves dividing your account balance by a life expectancy factor from IRS tables. This factor changes annually, typically resulting in larger required withdrawals as you age. Missing an RMD carries severe consequences: a 25% excise tax on the amount you should have withdrawn but didn't.

Calculating Your Required Minimum Distribution

| Age | Distribution Period | Example Balance | Required Distribution |

|---|---|---|---|

| 73 | 26.5 years | $500,000 | $18,868 |

| 75 | 24.6 years | $500,000 | $20,325 |

| 80 | 20.2 years | $500,000 | $24,752 |

| 85 | 16.0 years | $500,000 | $31,250 |

These calculations use the IRS Uniform Lifetime Table applicable for most account owners. Your specific calculation may differ based on your spouse's age if they're your sole beneficiary and more than 10 years younger.

Understanding RMD requirements becomes crucial for tax planning as you approach retirement. Working with fiduciary advisory services can help ensure you meet these obligations while optimizing your overall tax strategy.

Strategic Timing for IRA Distributions

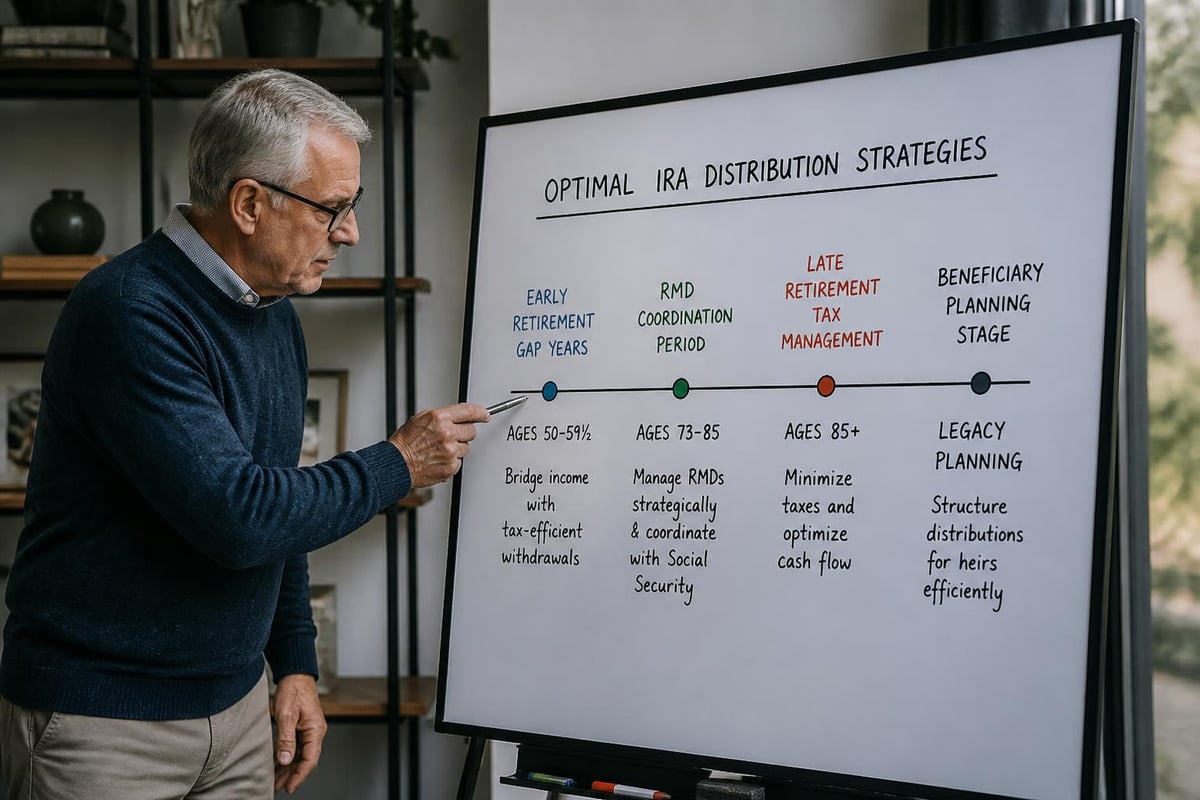

The timing of your ira distribution can dramatically affect your tax situation and retirement income sustainability. Several factors should influence when you choose to tap into these accounts.

Tax bracket management represents a primary consideration. Taking distributions during years when your income is lower can reduce the tax hit on traditional IRA withdrawals. Some retirees benefit from taking distributions before claiming Social Security benefits or during early retirement years before RMDs begin.

Roth conversion opportunities may arise during low-income years. Converting traditional IRA funds to a Roth IRA creates a taxable event in the current year but allows future tax-free growth and distributions. This strategy works particularly well if you anticipate higher tax rates later.

Healthcare coverage considerations matter significantly for those retiring before Medicare eligibility at age 65. Large ira distribution amounts can increase your modified adjusted gross income, potentially affecting premium tax credits for marketplace insurance plans.

Coordinating Distributions with Other Income Sources

- Social Security benefit timing affects total taxable income

- Pension payments create a baseline income floor

- Part-time employment during early retirement

- Capital gains from investment accounts

- Rental income or business revenue

Each income source interacts with your ira distribution to determine your overall tax liability. Strategic coordination across these sources can minimize lifetime taxes paid.

Early Distribution Exceptions and Hardship Withdrawals

Life circumstances sometimes necessitate accessing retirement funds before reaching age 59½. While the 10% early withdrawal penalty generally applies, the IRS recognizes specific situations warranting exceptions.

Qualified exceptions to the early distribution penalty include:

- Unreimbursed medical expenses exceeding 7.5% of adjusted gross income

- Health insurance premiums while unemployed

- Permanent disability as defined by IRS criteria

- Substantially equal periodic payments under IRS guidelines

- First-time home purchase (up to $10,000 lifetime limit)

- Qualified higher education expenses

- IRS levy on your retirement plan

- Qualified disaster distributions

Even when exceptions apply, you'll still owe income tax on traditional IRA distributions. Only the 10% additional penalty is waived. Careful documentation of qualifying circumstances is essential when claiming these exceptions on your tax return.

The IRS offers comprehensive guidance on retirement plan distributions including which circumstances qualify for penalty-free early access. Understanding these rules before taking an ira distribution can prevent costly mistakes.

Inherited IRA Distribution Rules

Inheriting an IRA creates unique distribution requirements that depend on your relationship to the deceased account owner and the account type. Recent legislation significantly changed these rules, making proper planning essential.

SECURE Act Changes for Non-Spouse Beneficiaries

The SECURE Act of 2019 introduced the 10-year rule for most non-spouse beneficiaries. Under this requirement, inherited IRA accounts must be fully distributed within 10 years following the original owner's death. This represents a significant change from previous rules allowing "stretch IRAs" where beneficiaries could take distributions over their lifetime.

Eligible designated beneficiaries who can still use the stretch provision include:

- Surviving spouses

- Minor children (until reaching age of majority)

- Disabled individuals

- Chronically ill individuals

- Beneficiaries less than 10 years younger than the deceased

The 10-year rule for inherited IRAs creates complex tax planning scenarios, particularly for beneficiaries in high tax brackets who must absorb potentially large distributions within a compressed timeframe.

Tax Planning Strategies for IRA Distributions

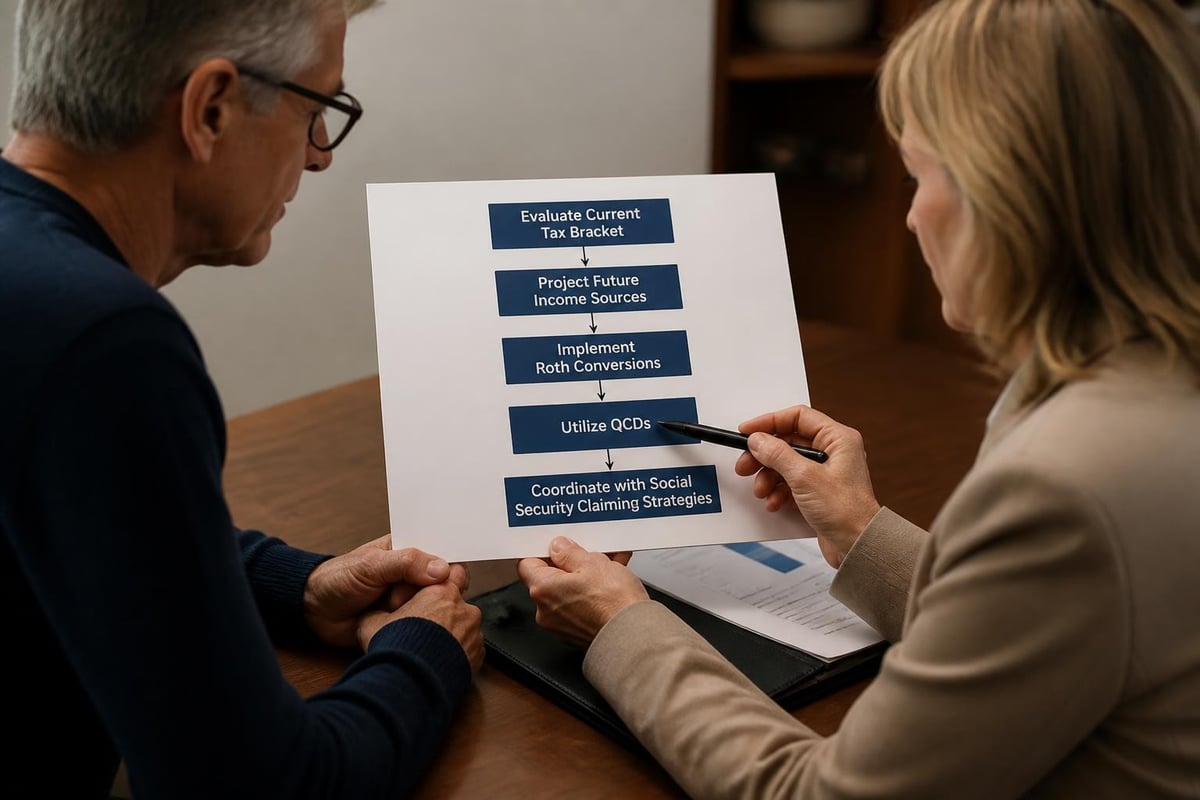

Minimizing taxes on your ira distribution requires proactive planning and coordination with your overall financial strategy. Several techniques can reduce your lifetime tax burden while maximizing retirement income.

Qualified Charitable Distributions (QCDs) allow individuals age 70½ or older to donate up to $105,000 annually (2026 limit) directly from an IRA to qualified charities. These distributions count toward RMD requirements but don't increase taxable income, creating significant tax savings for charitably inclined retirees.

Tax-loss harvesting in taxable accounts can offset IRA distribution income. Realizing capital losses strategically can reduce overall tax liability when you must take large distributions.

Multi-year tax projection modeling helps identify optimal distribution timing. Professional advisors can project future tax scenarios under different withdrawal strategies, revealing opportunities for tax efficiency. Consider working with retirement planning specialists who understand the nuances of distribution planning.

| Strategy | Best For | Tax Benefit | Complexity |

|---|---|---|---|

| QCDs | Charitable donors 70½+ | Income exclusion | Low |

| Roth conversions | Low-income years | Future tax-free growth | Medium |

| Bracket management | Flexible income timing | Lower marginal rates | Medium |

| SEPP withdrawals | Early retirees | Penalty avoidance | High |

Impact of IRA Distributions on Social Security Benefits

Your ira distribution decisions can significantly affect Social Security taxation and Medicare premiums. These interconnections often surprise retirees who don't anticipate how retirement account withdrawals influence other government benefits.

Up to 85% of Social Security benefits become taxable when your combined income (adjusted gross income plus tax-exempt interest plus half of Social Security benefits) exceeds certain thresholds. Large IRA distributions can push you into higher Social Security taxation brackets, effectively increasing your marginal tax rate beyond the standard income tax brackets.

Medicare Part B and Part D premiums use a two-year lookback based on modified adjusted gross income. A large ira distribution in 2026 affects your Medicare premiums in 2028, creating delayed financial impacts that require forward planning. Understanding how IRAs impact Social Security helps you develop comprehensive withdrawal strategies.

Income-Related Monthly Adjustment Amount (IRMAA)

Higher-income Medicare beneficiaries pay additional premiums through IRMAA surcharges. For 2026, these surcharges begin when modified adjusted gross income exceeds $106,000 for single filers or $212,000 for joint filers, with multiple tiers creating substantial premium increases.

Strategic timing of large ira distribution events around Medicare enrollment or during years when other income sources are lower can help minimize IRMAA surcharges and preserve more retirement income.

Rolling Over IRA Distributions

Not all money leaving your IRA represents a permanent taxable distribution. Rollovers allow you to move funds between retirement accounts without triggering immediate taxes, preserving tax-deferred growth potential.

Direct rollovers move funds from one IRA custodian directly to another without the money passing through your hands. This method avoids mandatory withholding and eliminates any risk of missing rollover deadlines.

60-day rollovers occur when you receive an ira distribution check and must redeposit the funds into another qualifying retirement account within 60 days. This method carries risks: the distributing institution typically withholds 20% for taxes, and failing to complete the rollover within 60 days creates a taxable event plus potential penalties.

The IRS limits you to one 60-day rollover per 12-month period across all IRAs you own. Direct trustee-to-trustee transfers don't count against this limitation. Rollover rules and withholding requirements contain numerous nuances that affect whether your transaction qualifies for tax-free treatment.

Roth IRA Distribution Rules

Roth IRA distributions follow different rules than traditional IRAs, creating unique planning opportunities. Understanding the distinction between contributions and earnings affects your tax strategy.

Contributions can be withdrawn at any time, at any age, completely tax and penalty-free. Since you funded Roth IRAs with after-tax dollars, the IRS doesn't penalize accessing your original contributions.

Earnings on those contributions face more restrictions. To withdraw earnings tax-free and penalty-free, you must satisfy both conditions: the account must be at least five years old, and you must be age 59½ or older (or meet another qualifying exception).

The Five-Year Rule for Roth IRAs

The five-year holding period begins January 1st of the year you made your first Roth contribution, not the actual contribution date. This timing quirk means a contribution made in April 2026 for tax year 2025 starts its five-year clock on January 1, 2025.

Roth IRAs carry no RMD requirements during the original owner's lifetime, making them powerful estate planning tools. Beneficiaries who inherit Roth IRAs must follow distribution rules but receive those distributions tax-free if the five-year rule was satisfied.

Distribution Reporting and Tax Forms

Proper reporting of your ira distribution ensures compliance with IRS requirements and accurate tax returns. Your IRA custodian issues Form 1099-R documenting all distributions taken during the year.

Form 1099-R contains multiple boxes reporting distribution amounts, taxable portions, and distribution codes indicating the type of withdrawal. These codes tell the IRS whether your distribution was premature, a normal distribution, an RMD, or qualifies for special treatment.

Common reporting mistakes include:

- Failing to report rollovers correctly, causing taxable income errors

- Incorrectly claiming early distribution exceptions

- Not tracking basis in traditional IRAs with non-deductible contributions

- Miscalculating the taxable portion of Roth conversions

Understanding how to report IRA withdrawals helps avoid IRS notices and ensures accurate tax calculations. Many distribution scenarios involve complex reporting requirements that benefit from professional guidance.

Year-End Planning for IRA Distributions

December presents critical deadlines and opportunities for ira distribution planning. Several time-sensitive strategies require completion before the calendar year ends.

RMD deadlines generally require satisfaction by December 31st each year. Your first RMD carries a one-time exception allowing delay until April 1st of the following year, though this creates a double distribution year with potentially higher taxes.

Qualified Charitable Distributions must reach the charity by December 31st to count for the current tax year. Processing time considerations mean initiating these distributions several weeks before year-end ensures timely completion.

Tax-loss harvesting opportunities close December 31st, making late-year reviews essential for offsetting ira distribution income with capital losses.

Roth conversion timing allows you to execute conversions through December 31st, though you'll want to ensure you can pay the resulting tax liability when filing your return the following April.

Working with investment management professionals who understand these year-end planning opportunities can help you maximize tax efficiency across your retirement accounts.

State Tax Considerations for IRA Distributions

While federal tax rules govern IRA operations, state taxation of ira distribution amounts varies significantly by location. Some states offer favorable treatment that influences retirement location decisions.

States with no income tax don't tax IRA distributions at the state level: Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire taxes only interest and dividends, not retirement account distributions.

States with retirement income exclusions provide varying degrees of tax relief on retirement distributions. Mississippi excludes all IRA distributions from state taxation. Illinois doesn't tax any retirement income including IRA distributions.

States that fully tax IRA distributions treat them as ordinary income with no special exclusions: California, Connecticut, Minnesota, Nebraska, Rhode Island, and Vermont, among others.

Residency decisions around retirement timing can significantly impact lifetime tax bills when ira distribution taxation differs substantially between states. However, tax considerations represent just one factor among many affecting where to live during retirement.

Coordination with Estate Planning Goals

Your ira distribution strategy intersects with estate planning objectives, particularly regarding beneficiary designations and legacy goals. These accounts pass outside your will through beneficiary designation forms, making those documents critical estate planning tools.

Beneficiary designation review should occur regularly to ensure alignment with current wishes. Life events like marriages, divorces, births, and deaths may necessitate updates that prevent unintended inheritance outcomes.

Spousal considerations offer unique flexibility. Surviving spouses can treat inherited IRAs as their own, delaying RMDs until their own required beginning date and naming new beneficiaries. Non-spouse beneficiaries face more restrictive distribution requirements under current law.

Tax-efficient beneficiary selection considers the tax situations of potential heirs. Naming high-income beneficiaries to inherit tax-deferred accounts may create larger tax burdens than leaving those assets to lower-bracket heirs or charities while directing other assets to high-earners.

Effective estate planning coordinates ira distribution rules with overall wealth transfer strategies, ensuring your legacy matches your intentions while minimizing unnecessary taxes.

Navigating ira distribution rules requires understanding complex regulations, strategic tax planning, and coordination with your broader financial picture. The decisions you make regarding when to take distributions, how much to withdraw, and which accounts to tap first can significantly impact your retirement security and tax liability over time. Whether you're approaching required minimum distributions, considering early withdrawals, or planning beneficiary strategies, Brookwood Investment Group provides personalized guidance tailored to your unique circumstances, helping you make informed decisions that align with your retirement goals and financial objectives.