Planning how to withdraw funds from your retirement accounts represents one of the most consequential financial decisions you'll make. The approach you select influences not only how long your savings will last but also the lifestyle you can sustain throughout your retirement years. With Americans living longer than ever before and market volatility remaining a constant factor, developing a thoughtful withdrawal plan has become increasingly important for retirees seeking financial stability. Understanding the various retirement withdrawal strategies available can help you make informed decisions that align with your unique circumstances and goals.

Understanding the Fundamentals of Retirement Distributions

Before diving into specific strategies, it's essential to grasp the basic principles that govern retirement withdrawals. Your retirement income typically comes from multiple sources including Social Security benefits, defined benefit pensions, tax-deferred accounts like traditional IRAs and 401(k)s, tax-free accounts such as Roth IRAs, and taxable investment accounts.

Each account type carries different tax implications that significantly impact your overall financial picture. Withdrawals from traditional retirement accounts are taxed as ordinary income, while Roth distributions generally come out tax-free if you meet the requirements. Understanding these tax consequences helps you coordinate withdrawals across different account types to potentially reduce your lifetime tax burden.

Timing Considerations for Withdrawals

The age at which you begin taking distributions matters considerably. While you can generally access retirement funds penalty-free starting at age 59½, waiting longer may allow your investments additional time to grow. However, Required Minimum Distributions (RMDs) mandate that you begin withdrawing from most tax-deferred accounts by age 73 for those turning 72 after December 31, 2022.

Delaying Social Security benefits beyond your full retirement age can increase your monthly payments by approximately 8% per year until age 70. This strategy may complement your retirement withdrawal strategies by providing higher guaranteed income later in life.

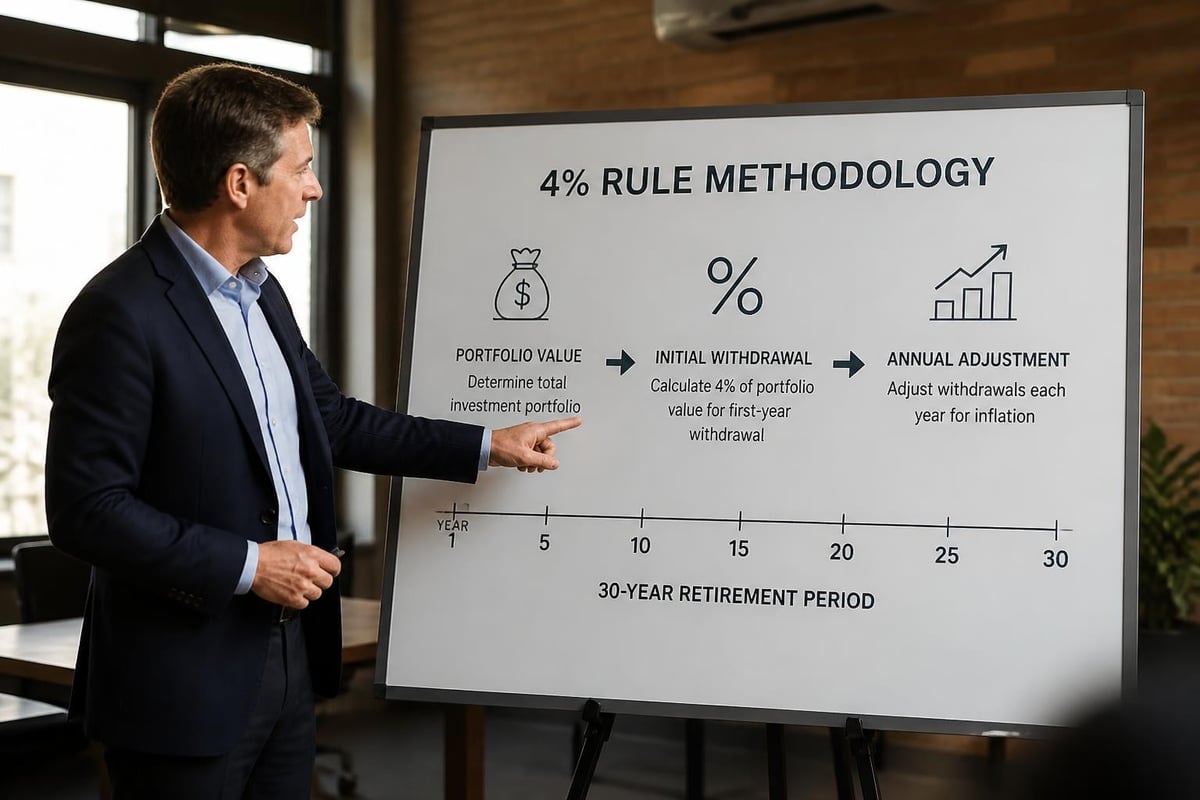

The Traditional 4% Rule and Its Applications

The 4% rule has served as a foundational guideline for retirement planning since financial planner William Bengen introduced it in the 1990s. This approach suggests withdrawing 4% of your retirement portfolio in the first year, then adjusting subsequent withdrawals for inflation annually.

Key assumptions underlying this strategy include:

- A balanced portfolio containing approximately 60% stocks and 40% bonds

- A 30-year retirement timeframe

- Historical market returns continuing into the future

- Consistent inflation rates

Research supporting this approach demonstrated that retirees following this pattern had a high probability of not outliving their savings. However, critics argue that current market conditions including lower bond yields and higher stock valuations may make the 4% rule less reliable than it was historically.

Modern Adaptations of the 4% Rule

Many financial professionals now advocate for more flexible interpretations. BlackRock’s overview of withdrawal strategies highlights several variations including starting with a lower initial withdrawal rate of 3% to 3.5% or implementing dynamic adjustments based on portfolio performance and market conditions.

Some retirees adopt a guardrails approach where they establish upper and lower spending limits. If portfolio performance exceeds expectations, withdrawals can increase slightly. Conversely, during market downturns, spending may need to decrease temporarily to preserve capital.

Dynamic Withdrawal Strategies for Changing Markets

Unlike static approaches, dynamic retirement withdrawal strategies adjust distributions based on portfolio performance, age, spending needs, and market conditions. This flexibility can potentially extend portfolio longevity while allowing retirees to capitalize on strong market years.

Fidelity’s approach to dynamic withdrawal strategies emphasizes the importance of adapting to your evolving financial situation. This method requires more active management but may offer superior outcomes for those willing to adjust their spending based on market realities.

Percentage-Based Withdrawal Approach

This strategy involves withdrawing a fixed percentage of your portfolio value each year, typically between 4% and 5%. Unlike the traditional 4% rule, this approach recalculates your withdrawal amount annually based on current portfolio value.

| Strategy Type | Initial Withdrawal | Adjustment Method | Volatility Level |

|---|---|---|---|

| Fixed Dollar | 4% of starting balance | Inflation-adjusted | Low |

| Fixed Percentage | 4-5% of current value | Portfolio-based | High |

| Dynamic | Variable based on rules | Performance-based | Moderate |

Advantages of this approach:

- Withdrawals automatically decrease during market downturns, preserving capital

- Higher distributions become available when markets perform well

- Simpler calculations than complex dynamic strategies

- Reduced risk of depleting your portfolio prematurely

The primary disadvantage involves income unpredictability. Retirees who require stable cash flow for fixed expenses may find this variability challenging to manage.

The Bucket Strategy for Retirement Income

The bucket strategy has gained considerable popularity among financial advisors and retirees seeking both stability and growth. This approach divides retirement assets into multiple "buckets" based on when you'll need the funds, with each bucket invested according to its time horizon.

Typical bucket allocation structure:

- Short-term bucket (0-2 years): Cash and cash equivalents including money market funds, high-yield savings accounts, and short-term CDs

- Medium-term bucket (3-10 years): Bonds, bond funds, balanced funds, and conservative income-generating investments

- Long-term bucket (10+ years): Growth-oriented investments including stocks, stock funds, and real estate investments

U.S. Bank’s discussion of the bucket strategy emphasizes how this method provides psychological comfort during market volatility since your immediate spending needs remain insulated from stock market fluctuations.

Implementing the Bucket Approach

You withdraw from the short-term bucket for current expenses while allowing the longer-term buckets to remain invested for growth. Periodically, typically during positive market years, you "refill" the short-term bucket by moving funds from the medium-term bucket, which in turn gets replenished from the long-term bucket.

This rebalancing discipline ensures you're generally selling investments when values are higher rather than being forced to sell during market downturns. The strategy aligns well with comprehensive financial planning services that consider your complete financial picture.

Systematic Withdrawal Plans and Floor-and-Upside Strategies

Systematic withdrawal plans offer structure and predictability for retirees who value consistent income streams. These plans establish regular distributions from investment accounts on a monthly or quarterly basis, similar to receiving a paycheck.

The floor-and-upside strategy combines guaranteed income sources with growth-oriented investments. Your "floor" consists of reliable income from Social Security, pensions, annuities, or bond ladders that cover essential expenses. The "upside" portion includes stock investments that provide growth potential and additional income for discretionary spending.

Establishing Your Income Floor

Calculate your essential monthly expenses including housing, healthcare, food, utilities, and insurance. Next, inventory your guaranteed income sources and determine whether they fully cover these baseline needs. If gaps exist, you might consider strategies to increase guaranteed income such as:

- Delaying Social Security to maximize benefits

- Purchasing immediate or deferred income annuities

- Creating a bond ladder for predictable interest payments

- Allocating a portion of assets to dividend-paying stocks with strong histories

Once your floor is established, remaining assets can be invested more aggressively for growth, knowing your basic needs are covered regardless of market performance. This psychological benefit often allows retirees to maintain higher equity allocations than they might otherwise tolerate.

Tax-Efficient Withdrawal Sequencing

The order in which you withdraw from different account types significantly impacts your after-tax retirement income. Conventional wisdom once suggested depleting taxable accounts first, then tax-deferred accounts, and finally Roth accounts. However, modern retirement withdrawal strategies often employ more sophisticated sequencing to optimize tax outcomes.

Strategic withdrawal sequencing considerations:

- Taking some tax-deferred distributions before RMDs begin to avoid large mandatory withdrawals later

- Utilizing Roth conversions during lower-income years to reduce future tax burdens

- Coordinating withdrawals with other income sources to manage tax brackets

- Harvesting capital gains in taxable accounts when you're in low tax brackets

- Timing charitable contributions from IRAs after age 70½ through Qualified Charitable Distributions

Bankrate’s analysis of retirement withdrawal strategies notes that tax planning should remain fluid throughout retirement as tax laws change and your personal situation evolves.

The Importance of Tax Bracket Management

Retirees often have more control over their taxable income than they realize. Strategic planning can help you fill up lower tax brackets with income from various sources while avoiding spikes that push you into higher brackets or trigger additional Medicare premiums through Income-Related Monthly Adjustment Amounts (IRMAA).

Working with professionals who understand the intersection of investment management and tax strategies can help identify opportunities to reduce lifetime tax liability. Some years it may make sense to realize additional income intentionally, while other years minimizing distributions preserves flexibility.

Adjusting Strategies for Market Volatility and Life Changes

Market downturns present particular challenges for retirement withdrawal strategies. Selling investments when values are depressed crystallizes losses and removes shares that won't participate in the eventual recovery. This sequence-of-returns risk means that experiencing poor market performance early in retirement can significantly reduce portfolio longevity.

The Motley Fool’s discussion of withdrawal strategies emphasizes the importance of flexibility during market stress. Options for managing volatility include:

- Reducing discretionary spending temporarily during bear markets

- Drawing from cash reserves or bond allocations rather than stocks

- Pausing portfolio rebalancing until markets recover

- Generating supplemental income through part-time work or consulting

- Delaying major purchases or gifts until portfolio values improve

Life Transitions Requiring Strategy Adjustments

Retirement rarely follows a perfectly predictable path. Health changes, family circumstances, housing decisions, and unexpected opportunities all may necessitate modifications to your withdrawal approach.

Major life events that often trigger strategy reviews include:

- Significant health diagnoses requiring increased medical spending

- Death of a spouse changing household income needs and tax filing status

- Relocating to a different state with varying tax implications

- Receiving an inheritance or selling a business

- Taking on financial responsibility for aging parents or adult children

- Deciding to leave a legacy through charitable giving or family gifts

Maintaining regular communication with trusted financial advisors ensures your withdrawal strategy remains aligned with your evolving needs and goals.

Avoiding Common Withdrawal Mistakes

Even well-intentioned retirees can make costly errors when implementing retirement withdrawal strategies. Common RMD mistakes include missing deadlines, calculating distributions incorrectly, or failing to account for all retirement accounts.

Critical Pitfalls to Avoid

Underestimating longevity: Many retirees plan for average life expectancies rather than considering that one spouse in a couple has a significant probability of living into their 90s. Conservative planning should account for potentially 30-35 years of retirement.

Ignoring healthcare costs: Medicare doesn't cover everything, and supplemental insurance, prescription drugs, and long-term care can consume substantial retirement resources. Factoring realistic healthcare inflation into your withdrawal plan prevents unpleasant surprises.

Failing to coordinate with Social Security timing: Your withdrawal strategy should align with your Social Security claiming strategy since the timing of benefits affects both your guaranteed income floor and your tax situation.

Neglecting required minimum distributions: Missing RMD deadlines triggers penalties of 25% (or 10% if corrected promptly) of the amount you should have withdrawn. Setting up systematic distributions before RMDs begin can help avoid this costly mistake.

Being too conservative with investments: While reducing risk in retirement makes sense, maintaining adequate growth potential remains important. Continuing wealth-building activities in retirement helps ensure your portfolio can sustain potentially decades of withdrawals.

Personalizing Your Withdrawal Approach

No single strategy works optimally for everyone. Your ideal approach depends on numerous factors including portfolio size, income needs, risk tolerance, health status, legacy goals, and personal preferences regarding spending flexibility.

Wells Fargo emphasizes personalization in developing withdrawal strategies that match individual circumstances. Variables to consider when designing your approach include:

| Factor | Impact on Strategy |

|---|---|

| Portfolio Size | Larger portfolios may tolerate more aggressive strategies |

| Fixed vs. Variable Expenses | High fixed costs require more stable income sources |

| Legacy Goals | Desire to leave inheritance may suggest lower withdrawal rates |

| Risk Tolerance | Comfort with volatility influences investment allocation |

| Pension Income | Guaranteed income allows more growth-oriented investing |

| Health Status | Shorter life expectancy may justify higher spending |

Some retirees prioritize maximizing lifetime spending, while others place greater emphasis on leaving assets to heirs or charitable causes. Understanding habits of successful retirees reveals that clarity about priorities enables better decision-making.

The Value of Professional Guidance

The complexity of retirement withdrawal strategies, combined with the high stakes of getting it wrong, makes professional guidance valuable for most retirees. Fiduciary advisors can provide objective recommendations tailored to your specific situation rather than promoting products that benefit them financially.

Comprehensive planning addresses not just withdrawal strategies but also investment allocation, tax planning, estate planning, and risk management. This holistic approach ensures all aspects of your financial life work together efficiently. Access to personalized financial planning services can help you navigate the complexities of retirement income management.

Monitoring and Adjusting Your Strategy Over Time

Implementing retirement withdrawal strategies isn't a set-it-and-forget-it proposition. Regular monitoring ensures your approach remains appropriate as markets fluctuate, tax laws change, and your personal circumstances evolve.

Recommended review schedule:

- Quarterly: Review portfolio performance, rebalance if necessary, and assess whether withdrawals are proceeding as planned

- Annually: Evaluate overall strategy effectiveness, adjust for inflation, review tax situation, and ensure RMD compliance

- Major life events: Reassess strategy following health changes, moves, inheritance, or family situation changes

- Significant market movements: Consider whether extreme market performance warrants temporary adjustments

Documentation helps track decision-making over time. Maintaining records of withdrawal amounts, tax payments, portfolio values, and reasoning behind strategy adjustments creates valuable historical context for future planning.

Incorporating Flexibility Into Your Plan

The most resilient retirement withdrawal strategies build in flexibility to accommodate uncertainty. Rather than committing rigidly to a single approach, consider establishing decision rules that guide adjustments based on circumstances.

For example, you might decide to increase withdrawals by 10% when your portfolio exceeds its starting value by 20% or more, but reduce discretionary spending by 15% if your portfolio declines by 20% or more. These predetermined guidelines remove emotion from difficult decisions during stressful market periods.

Building a cash cushion equal to one to two years of expenses provides flexibility to adjust withdrawal timing. This reserve lets you pause portfolio distributions during market downturns without immediately cutting your standard of living.

Selecting and implementing appropriate retirement withdrawal strategies requires careful consideration of multiple factors including portfolio composition, income needs, tax implications, and personal circumstances. The approaches outlined here offer different benefits depending on your priorities and risk tolerance. Whether you prefer the simplicity of traditional methods or the adaptability of dynamic strategies, the key is developing a plan that provides sustainable income throughout your retirement years. Brookwood Investment Group LLC offers personalized guidance in creating withdrawal strategies tailored to your unique financial situation, helping you navigate the complexities of retirement income planning with confidence. Their fiduciary commitment ensures recommendations focus solely on your best interests, coordinating withdrawal strategies with comprehensive tax planning, investment management, and estate planning services.