When planning for retirement, most individuals focus on achieving a target savings amount or a specific average annual return. However, there's a critical factor that many overlook: the order in which those returns occur. This timing element, known as sequence of returns risk, can dramatically impact whether your retirement portfolio lasts 20 years or 30 years, even when two portfolios achieve identical average returns over time. Understanding this concept is essential for anyone approaching or already in retirement, as it influences withdrawal strategies, asset allocation decisions, and overall financial security.

What Is Sequence of Returns Risk

Sequence of returns risk refers to the danger that negative investment returns early in retirement can permanently damage your portfolio's ability to sustain withdrawals throughout your lifetime. Unlike the accumulation phase when you're adding money to your accounts, the distribution phase creates a vulnerability to market timing.

During your working years, market downturns can actually benefit you through dollar-cost averaging. When prices fall, your contributions purchase more shares, setting you up for greater gains when markets recover. This dynamic reverses completely once you begin taking withdrawals.

The Mathematics Behind the Risk

The mathematical reality is straightforward yet often counterintuitive. Consider two retirees who both achieve a 6% average annual return over 20 years. One experiences strong returns in the first decade followed by poor returns in the second. The other faces the inverse: poor returns initially, then strong performance later.

The retiree who experiences negative returns early while simultaneously withdrawing funds faces a double setback. Portfolio values decline due to market losses and simultaneous withdrawals, leaving fewer assets to benefit from the eventual recovery. Charles Schwab emphasizes how timing matters significantly when understanding this phenomenon.

| Scenario | Years 1-10 Average Return | Years 11-20 Average Return | Portfolio Outcome |

|---|---|---|---|

| Favorable Sequence | +8% | +4% | Portfolio sustains withdrawals |

| Unfavorable Sequence | +4% | +8% | Portfolio depleted earlier |

| Accumulation Phase | Either sequence | Either sequence | Minimal difference |

The table above illustrates why sequence of returns risk primarily affects retirees rather than working professionals still contributing to their accounts.

Why Sequence of Returns Risk Matters More Now

Several converging factors make sequence of returns risk particularly relevant for today's retirees. Market volatility has increased in recent decades, with more frequent significant corrections and bear markets. The 2000-2002 dot-com crash, the 2008-2009 financial crisis, and the 2020 pandemic-induced volatility demonstrate how retirees can face multiple severe downturns.

Longevity improvements mean retirement portfolios must last longer. A 65-year-old couple in 2026 has a significant probability that at least one spouse will live into their 90s, requiring portfolios to sustain three decades of withdrawals.

Interest rate environments also play a crucial role. Lower yields on bonds and fixed-income investments push retirees toward higher equity allocations to generate necessary income, increasing exposure to equity market volatility and sequence risk.

The First Decade Vulnerability

Research consistently shows that the first 10 years of retirement represent the highest-risk period for sequence of returns risk. If you retire into a bear market or experience significant losses in your initial retirement years, the probability of portfolio depletion increases substantially.

This vulnerability exists because:

- Withdrawal rates are typically highest relative to portfolio value early in retirement

- There's less time for markets to recover before the next withdrawal

- Compound growth has less principal to work with after simultaneous losses and withdrawals

- Portfolio rebalancing becomes more difficult with a depleted asset base

Thrivent discusses strategies to address the specific challenges this timing creates for retirement security.

Real-World Examples of Sequence Risk Impact

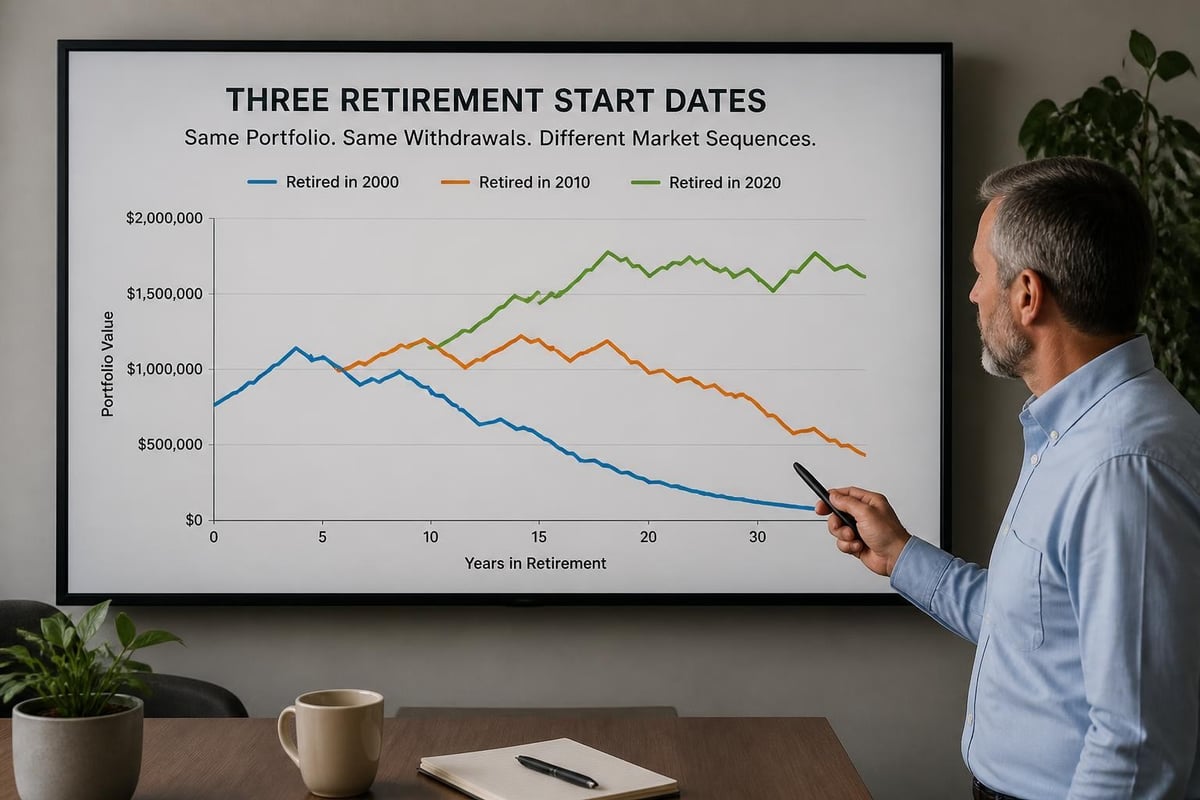

Consider three hypothetical retirees, each starting retirement in January 2000 with $1,000,000 and planning to withdraw $50,000 annually (5% initial withdrawal rate), adjusted for 3% inflation. Despite investing in identical portfolios, their experiences differed dramatically based on when they retired.

Case Study Analysis

Retiree A retired in January 2000, immediately facing the dot-com crash where the S&P 500 declined approximately 49% from peak to trough. Despite subsequent recoveries, the combination of early losses and ongoing withdrawals significantly reduced portfolio longevity.

Retiree B retired in January 2010, after markets had already experienced the financial crisis decline. While volatility continued, this retiree avoided withdrawing during the steepest losses, leaving more capital to benefit from the subsequent bull market.

Retiree C retired in January 2020, experiencing the pandemic crash within months of retirement but benefiting from the rapid recovery and strong subsequent returns.

These scenarios demonstrate how market timing at retirement, beyond any investor's control, creates vastly different outcomes even with identical strategies, highlighting the importance of working with experienced advisors who understand these dynamics.

Strategies to Mitigate Sequence of Returns Risk

Fortunately, several evidence-based strategies can help reduce sequence of returns risk exposure. No single approach eliminates the risk entirely, but combining multiple tactics creates a more resilient retirement plan.

Dynamic Withdrawal Strategies

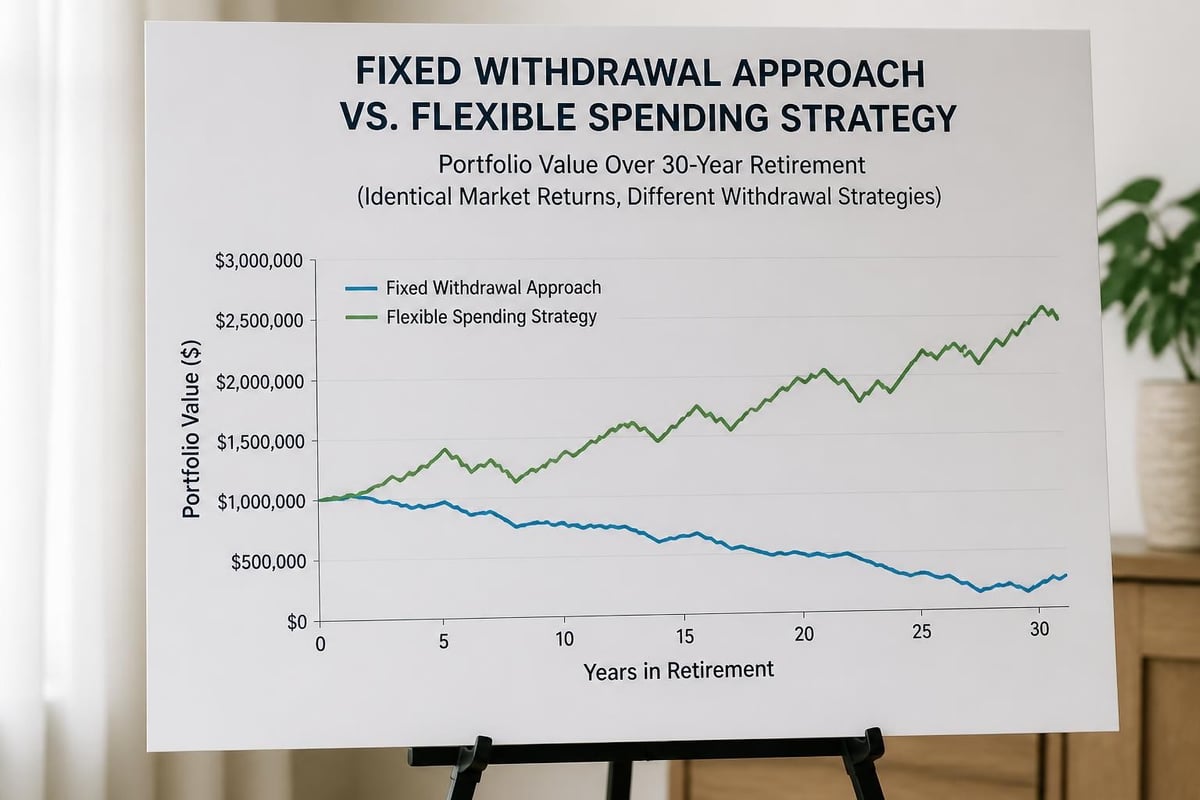

Rather than withdrawing a fixed dollar amount adjusted for inflation regardless of market conditions, dynamic strategies adjust withdrawals based on portfolio performance.

Guardrail approaches establish upper and lower withdrawal limits. When portfolio values increase significantly, you can increase withdrawals modestly. Conversely, when values decline below certain thresholds, you reduce withdrawals temporarily. This flexibility helps preserve capital during difficult market periods.

Percentage-based withdrawals tie each year's distribution to the current portfolio value rather than the initial value. While this creates income variability, it prevents the mathematical challenge of withdrawing fixed amounts from a declining portfolio.

The key advantage is that these strategies force spending reductions during market downturns, the exact time when maintaining high withdrawals does the most damage.

The Bucket Strategy

The bucket approach divides your portfolio into multiple segments based on time horizon:

- Immediate needs bucket (years 1-3): Cash and highly stable investments to fund near-term expenses

- Medium-term bucket (years 4-10): Balanced portfolio of bonds and dividend-paying stocks

- Long-term bucket (years 11+): Growth-oriented investments with higher equity allocations

This structure provides several benefits. You avoid selling equities during market downturns by drawing from the cash bucket. The medium-term bucket replenishes cash during favorable markets. The long-term bucket maintains growth potential for later retirement years.

Kiplinger recommends this bucket approach as one method to safeguard retirement assets against sequence risk.

Strategic Asset Allocation Adjustments

Traditional retirement advice suggested increasing bond allocations as you age, following rules like holding your age in bonds. Modern research suggests more nuanced approaches may better address sequence of returns risk.

Rising equity glide paths maintain higher equity allocations in early retirement when sequence risk is highest, then gradually increase equity exposure in later years when longevity risk becomes the primary concern. This counterintuitive approach recognizes that severe early losses pose the greatest danger.

Tactical positioning around the retirement date might involve temporarily increasing defensive positions 2-3 years before retirement and maintaining them for 3-5 years after, then gradually moving back to a more aggressive allocation.

| Strategy | Primary Benefit | Implementation Complexity | Income Stability |

|---|---|---|---|

| Dynamic Withdrawals | Preserves capital in downturns | Medium | Variable |

| Bucket Approach | Avoids selling in downturns | Low | High |

| Rising Equity Glide Path | Optimizes longevity vs sequence risk | High | Medium |

| Fixed Allocation | Simplicity | Low | Medium |

Additional Income Sources as Protection

Sequence of returns risk affects only the portion of retirement income dependent on portfolio withdrawals. Diversifying income sources reduces vulnerability to market timing.

Social Security Optimization

Delaying Social Security benefits increases the guaranteed inflation-adjusted income stream, reducing portfolio withdrawal requirements. Each year of delay from full retirement age to age 70 increases benefits by approximately 8%, providing valuable sequence risk protection.

Strategic claiming considers both spouses' benefit histories, health status, and other income sources to maximize lifetime benefits. For many retirees, ensuring adequate guaranteed income through Social Security reduces the pressure on portfolio withdrawals during market downturns.

Annuity Considerations

Income annuities convert a portion of savings into guaranteed lifetime payments, creating a personal pension. This guaranteed income reduces the withdrawal rate needed from the investment portfolio, leaving more assets to weather market volatility.

Deferred income annuities can be purchased years before payments begin, often providing higher payout rates. Strategic annuity placement creates income floors that continue regardless of market performance.

While annuities involve tradeoffs including reduced flexibility and legacy potential, they can effectively reduce sequence of returns risk for the portion of retirement expenses they cover. Understanding these complex products often requires guidance from fiduciary advisors who prioritize client interests.

Withdrawal Rate Considerations

The widely cited 4% rule, suggesting retirees can safely withdraw 4% of their initial portfolio value adjusted annually for inflation, emerged from research examining historical sequence of returns scenarios. However, this guideline requires important context.

Flexibility Is Essential

Research shows that rigid adherence to any withdrawal percentage without adjusting for market conditions or personal circumstances increases sequence of returns risk. The 4% rule assumed a 30-year retirement period and specific asset allocations.

Starting withdrawal rates should consider:

- Current market valuations at retirement

- Expected retirement duration

- Asset allocation strategy

- Flexibility in spending requirements

- Other income sources available

Lower initial withdrawal rates (3-3.5%) provide greater protection against unfavorable sequences but require either larger nest eggs or reduced spending. Higher rates (5%+) significantly increase the probability of portfolio depletion if early returns disappoint.

CNBC highlights how early market downturns can quickly deplete savings when withdrawal rates are too aggressive for prevailing market conditions.

Spending Flexibility Value

Retirees who can reduce discretionary spending by 10-20% during market downturns dramatically improve portfolio sustainability. This flexibility might involve:

- Postponing major purchases during bear markets

- Reducing travel or entertainment expenses temporarily

- Delaying home improvements or renovations

- Adjusting gift giving to family members

The mathematical impact of even modest spending reductions during critical early retirement years proves substantial. A temporary 15% spending reduction during a two-year market decline can extend portfolio longevity by several years.

Tax Strategy Integration

Tax planning directly impacts sequence of returns risk by influencing both withdrawal amounts needed and the tax efficiency of those withdrawals. Strategic tax management preserves more assets to weather market volatility.

Tax Location Strategy

Different account types receive different tax treatment, creating opportunities for strategic withdrawals that minimize tax drag on portfolios.

Tax-deferred accounts (traditional IRAs, 401(k)s) require ordinary income tax on withdrawals. Tax-free accounts (Roth IRAs) provide tax-free qualified distributions. Taxable brokerage accounts offer capital gains treatment and step-up basis at death.

During market downturns, withdrawing from taxable accounts or previously converted Roth accounts avoids selling depressed assets in tax-deferred accounts. This preservation strategy allows tax-deferred accounts more time to recover.

Roth Conversion Timing

Strategic Roth conversions during early retirement years or market downturns can reduce future required minimum distributions and create tax-free income sources for later retirement. Converting when account values are temporarily depressed due to market declines converts fewer dollars at lower values.

These conversions require careful analysis considering current tax brackets, future tax expectations, and overall retirement and estate planning objectives.

When to Reassess Your Strategy

Sequence of returns risk management isn't a one-time planning exercise. Regular reassessment ensures strategies remain appropriate as circumstances evolve.

Trigger Events for Review

Significant market movements, either positive or negative, warrant strategy evaluation. After a 20%+ decline, reassessing withdrawal rates and potentially implementing temporary spending reductions protects portfolio longevity. Following strong market gains, you might adjust buckets or modestly increase discretionary spending.

Life changes also necessitate review:

- Health status changes affecting life expectancy

- Inheritance or other windfalls

- Changes in housing costs or living situations

- Required minimum distribution age approaches

- Long-term care needs emergence

Annual reviews with financial professionals help identify necessary adjustments before small issues become significant problems.

Market Valuation Considerations

Retiring when markets appear overvalued based on historical metrics (high P/E ratios, elevated market capitalization to GDP) may warrant more conservative initial withdrawal rates and higher cash reserves. Understanding these market dynamics helps inform appropriate positioning.

Conversely, retiring after significant market corrections when valuations appear more reasonable historically might support slightly higher withdrawal rates, though caution remains prudent.

The Role of Professional Guidance

Navigating sequence of returns risk involves complex, interconnected decisions spanning investments, taxes, Social Security, insurance, and estate planning. The interplay between these elements makes professional guidance particularly valuable.

Experienced advisors help clients understand their specific vulnerability to sequence risk based on retirement timing, asset levels, spending requirements, and other income sources. They implement and monitor dynamic strategies that adjust as conditions change.

Fiduciary advisors provide advice in clients' best interests rather than promoting specific products. This alignment proves especially important when evaluating solutions like annuities or insurance products that address sequence risk but involve commissions and fees.

Virtual-first advisory models offer the convenience of remote access while maintaining the personalized attention necessary for comprehensive retirement planning. Technology enables regular monitoring and communication without geographic constraints.

Behavioral Aspects of Managing Sequence Risk

Understanding sequence of returns risk intellectually differs from maintaining discipline when markets decline 30% and your portfolio value drops while you're simultaneously withdrawing funds. Behavioral finance research shows that emotional responses to losses often lead to poor timing decisions.

Staying the Course During Volatility

Retirees facing significant losses early in retirement may panic and shift to overly conservative allocations, locking in losses and missing recoveries. Others might increase spending during good times without considering subsequent downturns.

Pre-commitment strategies help manage these behavioral challenges:

- Establish withdrawal and rebalancing rules in advance

- Automate distribution amounts to remove emotion from timing

- Maintain emergency reserves to avoid panic selling

- Focus on spending needs rather than portfolio values

- Limit portfolio checking frequency during volatile periods

Having predetermined guidelines and professional support helps retirees maintain beneficial strategies even when emotions push toward counterproductive actions.

Communication and Expectations

Clear understanding of sequence of returns risk and predetermined response strategies reduces anxiety when markets inevitably decline. Knowing that temporary spending reductions or drawing from cash reserves represents the plan rather than a crisis helps maintain emotional equilibrium.

Regular communication with advisors during volatile periods provides reassurance and keeps focus on long-term objectives rather than short-term fluctuations.

Understanding and managing sequence of returns risk represents one of the most critical aspects of retirement planning, yet it often receives insufficient attention until market declines expose the vulnerability. By implementing dynamic withdrawal strategies, maintaining appropriate asset allocations, diversifying income sources, and working with experienced professionals, retirees can significantly reduce this risk. At Brookwood Investment Group, our fiduciary advisors specialize in developing comprehensive retirement strategies that address sequence risk through personalized planning tailored to your unique circumstances and goals. If you're approaching retirement or want to reassess your current plan's resilience to market timing risk, Brookwood Investment Group can help you build a more secure financial future.