Building wealth and achieving independence from financial constraints requires more than simply earning a higher income. A well-structured financial freedom strategy combines disciplined spending habits, strategic investment decisions, and comprehensive planning across multiple areas of your financial life. The journey toward financial independence involves creating systems that generate sustainable wealth while protecting your assets and minimizing unnecessary risks. This approach enables you to make life decisions based on what matters most to you, rather than being limited by monetary concerns.

Understanding the Foundation of Financial Independence

Financial freedom means different things to different people. For some, it represents complete retirement from traditional employment. For others, it means having sufficient resources to pursue passion projects or spend more time with family without worrying about income.

The core principle underlying any effective financial freedom strategy centers on creating multiple income streams that eventually exceed your living expenses. This gap between income and expenses becomes the fuel for wealth accumulation and investment growth.

Defining Your Personal Vision

Before implementing specific tactics, you must clarify what financial independence means in your unique situation. Consider these fundamental questions:

- What annual income would you need to maintain your desired lifestyle?

- At what age do you want to achieve financial independence?

- What trade-offs are you willing to make today for future freedom?

- How much risk can you comfortably tolerate in your investment portfolio?

These answers form the blueprint for your customized approach. Research from Charles Schwab emphasizes the importance of setting clear goals as the foundation for building financial independence.

Building Your Budget Framework

A robust financial freedom strategy begins with understanding exactly where your money goes each month. Without this awareness, implementing advanced investment tactics becomes significantly more challenging.

Your budget serves as the operational backbone of wealth creation. It reveals opportunities to redirect funds from low-value spending toward high-impact investing and saving.

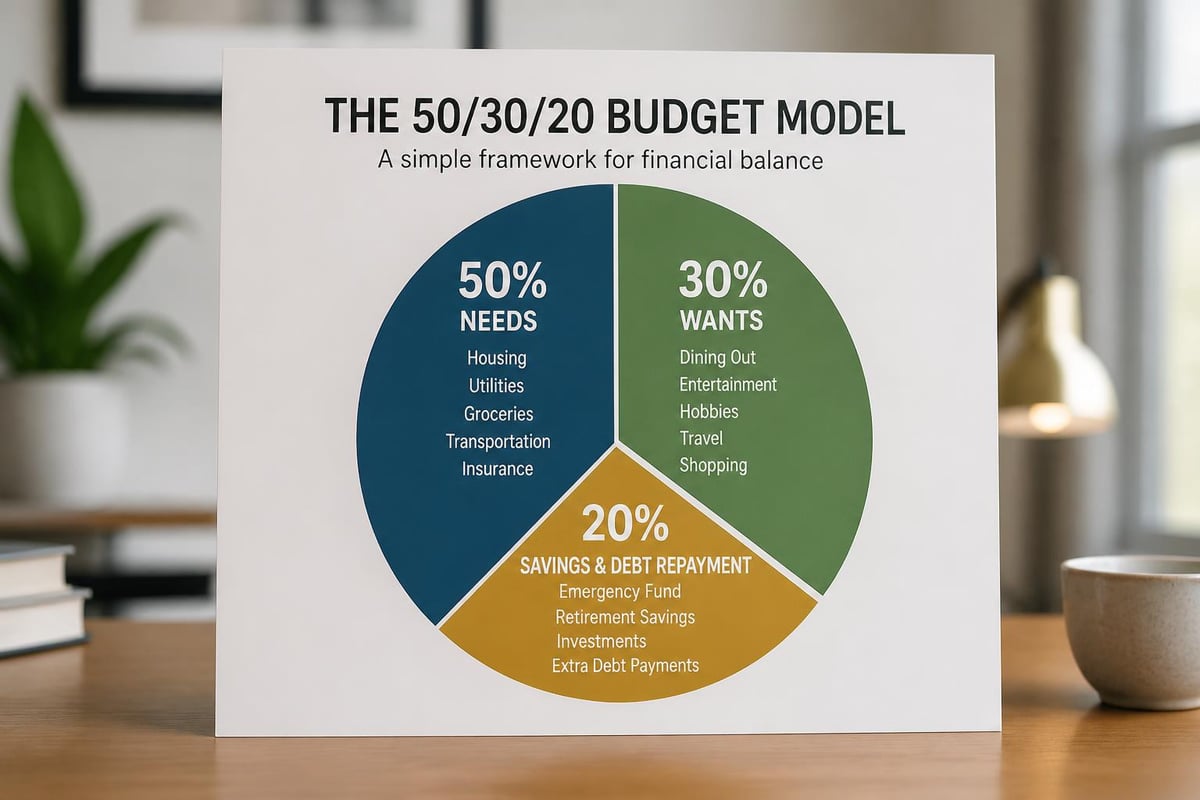

The 50/30/20 Allocation Model

This framework divides your after-tax income into three categories:

| Category | Percentage | Purpose |

|---|---|---|

| Needs | 50% | Housing, utilities, groceries, insurance, minimum debt payments |

| Wants | 30% | Dining out, entertainment, hobbies, non-essential purchases |

| Financial Goals | 20% | Savings, investments, debt repayment beyond minimums |

While this model provides a starting point, your optimal allocation depends on your current financial position and timeline for achieving independence. Those who start later may need to allocate 30-40% toward financial goals.

Tracking and Optimization

Technology has simplified expense tracking considerably. Digital tools automatically categorize transactions, revealing spending patterns that might otherwise remain hidden.

Review your spending monthly to identify categories where you consistently exceed budgeted amounts. Small adjustments across multiple categories often yield better results than dramatic cuts in one area. The key is sustainability-your financial freedom strategy must be maintainable for years or decades.

Strategic Debt Management

Debt represents one of the most significant obstacles to achieving financial independence. High-interest consumer debt, in particular, undermines wealth-building efforts by diverting funds toward interest payments rather than asset accumulation.

Prioritization Methods

Two primary approaches exist for debt elimination:

Avalanche Method: Focus on paying off debts with the highest interest rates first while making minimum payments on others. This approach minimizes total interest paid over time.

Snowball Method: Pay off smallest balances first, regardless of interest rate, creating psychological wins that build momentum.

Both methods work effectively. Choose based on whether mathematical optimization or behavioral motivation matters more to your personality type.

Consider that eliminating a credit card with a 19% interest rate delivers a guaranteed 19% return on those funds. Few investments offer such certainty. Forbes outlines defining personal financial goals as a critical step in the broader independence journey.

Investment Strategy Development

Once you've established budgeting discipline and addressed high-interest debt, your financial freedom strategy shifts toward wealth accumulation through strategic investing.

Investment decisions should align with your timeline, risk tolerance, and financial goals. A 30-year-old building toward retirement in 2056 has different needs than a 55-year-old planning to retire within a decade.

Asset Allocation Principles

Diversification across asset classes reduces portfolio volatility while maintaining growth potential. A balanced approach typically includes:

- Equities: Stocks provide long-term growth potential but experience short-term volatility

- Fixed Income: Bonds offer stability and income, particularly important as you near retirement

- Real Estate: Property investments provide inflation protection and potential income streams

- Cash Reserves: Liquid emergency funds prevent forced asset sales during market downturns

Your specific allocation should reflect your personal circumstances. Generally, younger investors can tolerate higher equity exposure, while those approaching retirement benefit from increased fixed-income allocations.

Tax-Advantaged Accounts

Maximizing contributions to tax-advantaged retirement accounts accelerates wealth building significantly. These vehicles offer either immediate tax deductions (traditional accounts) or tax-free growth (Roth accounts).

For 2026, contribution limits include:

| Account Type | Annual Limit | Catch-Up (50+) |

|---|---|---|

| 401(k)/403(b) | $23,500 | $7,500 |

| IRA (Traditional/Roth) | $7,000 | $1,000 |

| HSA (Individual) | $4,300 | $1,000 |

These limits represent powerful wealth-building tools. A consistent $23,500 annual contribution with 7% average returns grows to over $2.4 million in 30 years.

Working with professionals who provide fiduciary planning ensures your investment strategy aligns with your best interests rather than product sales quotas.

Risk Management and Protection

An often-overlooked component of a comprehensive financial freedom strategy involves protecting accumulated wealth from unexpected events. Insurance plays a critical role in preventing financial setbacks that could derail years of disciplined saving.

Essential Coverage Types

Appropriate insurance protects against catastrophic financial losses:

- Health Insurance: Medical expenses represent a leading cause of bankruptcy in the United States

- Disability Insurance: Protects your income-earning ability if injury or illness prevents work

- Life Insurance: Provides for dependents if you pass away prematurely

- Property and Casualty: Covers home and auto damage along with liability protection

- Umbrella Liability: Additional liability coverage beyond standard policy limits

Review coverage annually to ensure it reflects current needs. As your net worth grows, liability protection becomes increasingly important.

Advanced Tax Planning Strategies

Taxes represent one of your largest lifetime expenses. Strategic tax planning within your financial freedom strategy can save hundreds of thousands of dollars over a career.

Tax Location Strategy

Different account types receive different tax treatment. Optimize by placing investments in accounts that maximize tax efficiency:

Tax-Deferred Accounts (Traditional IRA, 401(k)):

- Corporate bonds generating ordinary income

- REITs distributing non-qualified dividends

- Actively managed funds with high turnover

Tax-Free Accounts (Roth IRA, Roth 401(k)):

- Investments with highest expected growth

- Small-cap and emerging market funds

- Individual stocks held long-term

Taxable Accounts:

- Tax-efficient index funds

- Municipal bonds (for high earners)

- Stocks eligible for qualified dividend treatment

This approach minimizes tax drag on portfolio returns. SmartAsset provides strategies for tax optimization within a broader financial independence framework.

Harvesting Strategies

Tax-loss harvesting allows you to sell investments at a loss to offset gains elsewhere in your portfolio. This strategy reduces your current tax liability while maintaining market exposure through similar replacement investments.

Capital gains harvesting in low-income years involves realizing gains when your tax rate is minimal, effectively securing a lower lifetime tax rate on appreciated assets.

Estate Planning Integration

A complete financial freedom strategy extends beyond your lifetime. Proper estate planning ensures your wealth transfers according to your wishes while minimizing estate taxes and probate complications.

Essential estate planning documents include:

- Will: Specifies asset distribution and guardian appointments for minor children

- Revocable Living Trust: Avoids probate and provides privacy for asset transfers

- Powers of Attorney: Designates decision-makers for financial and healthcare matters

- Healthcare Directive: Outlines end-of-life care preferences

Estate planning becomes particularly important as net worth increases. For 2026, the federal estate tax exemption stands at $13.99 million per individual, though this amount is scheduled to sunset in 2026. State-level estate taxes may apply at lower thresholds.

Professionals offering comprehensive retirement planning and estate planning services help ensure coordination between these critical financial areas.

Creating Multiple Income Streams

Relying solely on employment income creates vulnerability. A robust financial freedom strategy incorporates multiple revenue sources that provide stability if one stream diminishes.

Income Diversification Options

Consider developing these additional income channels:

Investment Income:

- Dividend-paying stocks providing quarterly distributions

- Bond interest from fixed-income holdings

- Real estate investment trusts (REITs) generating regular income

- Rental property cash flow after expenses

Business Income:

- Consulting or freelancing in your area of expertise

- Digital products or courses sharing specialized knowledge

- Service businesses requiring minimal capital investment

Passive Income:

- Royalties from creative works or patents

- Affiliate marketing from content creation

- Automated online businesses

Each income stream reduces dependence on traditional employment and accelerates progress toward financial independence. Capital One discusses investing early as one of nine essential habits for achieving financial freedom.

Behavioral Finance Considerations

Even the most sophisticated financial freedom strategy fails without addressing the psychological elements of money management. Behavioral biases often undermine rational decision-making.

Common Psychological Traps

Loss Aversion: People feel losses approximately twice as intensely as equivalent gains. This leads to holding losing investments too long and selling winners prematurely.

Recency Bias: Overweighting recent events when making decisions. After market crashes, investors often become overly conservative, missing subsequent recoveries.

Overconfidence: Believing you can predict market movements or pick winning stocks consistently. Evidence shows even professional investors struggle to beat market indexes over time.

Understanding these tendencies helps you implement systems that prevent emotional decision-making during market volatility.

Automation as a Solution

Automating financial decisions removes emotion from the equation:

- Schedule automatic transfers to investment accounts on payday

- Set up automatic bill payments to avoid late fees

- Implement automatic rebalancing to maintain target allocations

- Use automatic contribution increases annually

This "set and forget" approach ensures consistent progress regardless of market conditions or emotional states.

Measuring Progress and Adjusting Course

Your financial freedom strategy requires regular monitoring and adjustment. Market conditions change, personal circumstances evolve, and goals shift over time.

Key Performance Indicators

Track these metrics quarterly to assess progress:

| Metric | Target | Purpose |

|---|---|---|

| Savings Rate | 20%+ of gross income | Measures discipline and progress speed |

| Net Worth Growth | Increasing quarterly | Confirms wealth accumulation trajectory |

| Investment Returns | Benchmark comparison | Validates investment strategy effectiveness |

| Debt-to-Income Ratio | Decreasing over time | Tracks leverage reduction |

| Emergency Fund | 6-12 months expenses | Ensures financial stability cushion |

Comparing actual results against projections reveals whether you're on track to meet timeline goals. Shortfalls indicate a need for increased savings rates or adjusted expectations.

When to Seek Professional Guidance

Complex financial situations benefit from professional expertise. Consider working with qualified advisors when you face:

- Significant life transitions (marriage, divorce, inheritance, business sale)

- Complex tax situations requiring strategic planning

- Investment portfolio management beyond your expertise

- Retirement planning calculations and withdrawal strategies

- Estate planning for high net worth situations

Professionals offering comprehensive financial services provide coordinated guidance across all financial planning areas, ensuring strategies work together effectively.

The Role of Continuous Education

Financial markets, tax laws, and investment vehicles evolve constantly. A successful financial freedom strategy includes ongoing education to stay current with opportunities and risks.

Resources for continuous learning include:

- Financial planning publications and research

- Investment commentary from reputable sources

- Tax law updates and planning implications

- Estate planning regulation changes

- Economic trends affecting investment decisions

Kiplinger provides expert insights from financial planners on achieving true financial freedom through systematic approaches.

Dedicate time monthly to expanding your financial knowledge. This investment in education often yields returns exceeding traditional investments by helping you make better decisions and avoid costly mistakes.

Implementation Timeline

Breaking your financial freedom strategy into phases prevents overwhelm and creates achievable milestones.

Phase 1 (Months 1-3): Foundation Building

- Establish budget tracking system

- Build starter emergency fund ($1,000-$2,000)

- List all debts with interest rates and balances

- Review current insurance coverage

- Calculate net worth baseline

Phase 2 (Months 4-12): Debt Reduction and Savings

- Implement debt payoff strategy

- Increase emergency fund to one month expenses

- Maximize employer 401(k) match

- Review and optimize spending categories

- Set up automatic investment contributions

Phase 3 (Years 2-5): Wealth Acceleration

- Complete emergency fund (6-12 months)

- Maximize tax-advantaged account contributions

- Eliminate all high-interest debt

- Develop additional income streams

- Implement tax-loss harvesting strategies

Phase 4 (Years 5+): Optimization and Protection

- Focus on asset location optimization

- Increase charitable giving strategies

- Develop comprehensive estate plan

- Consider Roth conversion opportunities

- Refine withdrawal strategies for financial independence

This phased approach creates momentum through early wins while building toward long-term objectives. Exploring customized planning approaches ensures your strategy fits your unique circumstances rather than following generic advice.

Virtual Advisory Benefits

The financial services industry has evolved significantly with technology adoption. Virtual advisory relationships offer several advantages for implementing your financial freedom strategy.

Accessibility: Meet with advisors regardless of geographic location, expanding your choice of qualified professionals.

Convenience: Schedule meetings around your calendar without commuting time, making regular check-ins more feasible.

Technology Integration: Digital tools provide real-time portfolio access, document sharing, and collaborative planning platforms.

Cost Efficiency: Virtual-first firms often have lower overhead, potentially translating to reduced fees for clients.

These benefits make professional guidance more accessible for individuals at various stages of wealth building, not just those with substantial existing assets.

Achieving financial independence requires a comprehensive strategy that addresses budgeting, investing, tax optimization, risk management, and estate planning as interconnected components of your financial life. Success comes from consistent implementation of disciplined financial habits over time, regular monitoring of progress, and adjustments as circumstances evolve. Brookwood Investment Group LLC offers personalized, fiduciary guidance through a virtual-first model that makes professional financial planning accessible and tailored to your unique goals, helping you navigate each phase of your journey toward financial freedom.