Building a financially secure retirement requires more than just saving money. It demands strategic planning to minimize the tax burden on your hard-earned savings. As tax rates potentially shift and legislative changes continue to reshape the retirement landscape, understanding how to structure your retirement income to reduce or eliminate taxes becomes increasingly valuable. The concept of tax-free retirement income isn't just a dream for the wealthy; it's an achievable goal for individuals who implement the right strategies early and consistently.

Understanding Tax-Free Retirement Income Sources

Tax-free retirement income comes from specific account types and strategies designed to provide distributions without triggering federal income tax obligations. Unlike traditional retirement accounts where withdrawals are taxed as ordinary income, certain vehicles allow your money to grow and be withdrawn completely tax-free when structured properly.

The most common sources of tax-free retirement income include Roth IRAs, Roth 401(k)s, Health Savings Accounts (HSAs), and certain life insurance policies. Each of these vehicles operates under different rules, but they share the common benefit of providing distributions that don't increase your taxable income during retirement years.

Roth Accounts: The Foundation of Tax-Free Retirement

Roth accounts represent the cornerstone of most tax-free retirement strategies. With a Roth IRA or Roth 401(k), you contribute after-tax dollars today in exchange for completely tax-free withdrawals in retirement. This trade-off can be particularly advantageous if you expect to be in a higher tax bracket during retirement or if tax rates increase over time.

For 2026, Roth IRA contribution limits allow individuals under age 50 to contribute $7,000 annually, while those 50 and older can contribute $8,000. These accounts offer significant flexibility, as contributions (but not earnings) can be withdrawn at any time without penalty. Understanding different retirement account options helps you determine which vehicles align best with your financial goals.

Key Roth Account Benefits:

- Tax-free qualified distributions after age 59½

- No required minimum distributions (RMDs) during the account owner's lifetime

- Tax-free inheritance options for beneficiaries

- Flexibility to withdraw contributions penalty-free

- Protection from future tax rate increases

Advanced Strategies for High-Income Earners

High-income professionals often face unique challenges in building tax-free retirement income due to income limitations on Roth IRA contributions. However, several sophisticated strategies can help overcome these barriers and maximize tax-free accumulation potential.

The Mega Backdoor Roth Strategy

For individuals with access to certain 401(k) plans, the mega backdoor Roth strategy allows contributions far exceeding standard Roth IRA limits. This approach involves making after-tax contributions to your 401(k) beyond the standard elective deferral limit, then converting those funds to a Roth account.

In 2026, the total 401(k) contribution limit (employee plus employer) is $70,000 for those under 50, and $77,500 for those 50 and older. After maximizing your elective deferrals and receiving any employer match, the remaining room can potentially be filled with after-tax contributions that are then converted to Roth.

| Strategy Component | Annual Limit (2026) | Tax Treatment |

|---|---|---|

| Employee Elective Deferral | $23,500 ($31,000 age 50+) | Pre-tax or Roth |

| Employer Match | Varies by plan | Pre-tax |

| After-tax Contributions | Up to $70,000 total limit | After-tax, then convert |

| Mega Backdoor Roth Result | Potentially $46,500+ | Tax-free in retirement |

This strategy requires specific plan features, including the ability to make after-tax contributions and either in-service distributions or in-plan Roth conversions. Working with fiduciary advisory services can help determine if your plan qualifies and how to execute this strategy effectively.

Roth Conversion Ladder Planning

Strategic Roth conversions involve gradually moving money from traditional pre-tax retirement accounts into Roth accounts during years when your income is lower. This might occur during early retirement years before Social Security begins, during career transitions, or in years with significant deductions.

The key is converting enough to fill up lower tax brackets without pushing yourself into higher marginal rates. Converting a traditional 401(k) into a Roth 401(k) requires careful analysis of current versus expected future tax rates, but can significantly expand your tax-free retirement income potential.

Optimal Roth Conversion Timing:

- Early retirement years before required minimum distributions begin

- Years with unusually low income or high deductions

- When market downturns have temporarily reduced account values

- Before Social Security or pension income begins

- After leaving employment but before drawing on retirement accounts

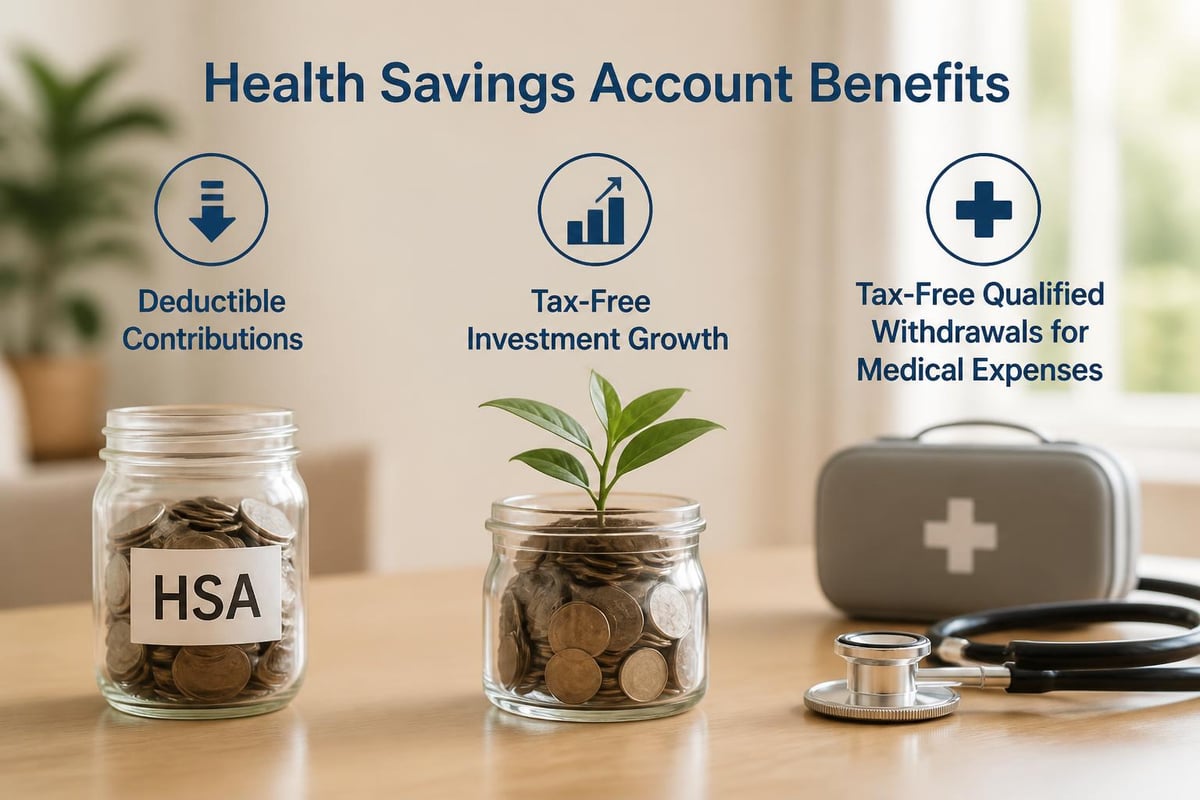

Health Savings Accounts: The Triple Tax Advantage

Health Savings Accounts represent one of the most powerful yet underutilized tools for building tax-free retirement income. Often called the "triple tax advantage," HSAs offer tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses at any age.

For 2026, HSA contribution limits are $4,300 for individual coverage and $8,550 for family coverage, with an additional $1,000 catch-up contribution for those 55 and older. To qualify, you must be enrolled in a High Deductible Health Plan (HDHP).

The strategic approach involves maximizing HSA contributions annually, investing the funds for long-term growth rather than spending them on current medical expenses, and preserving receipts for qualified medical expenses. You can reimburse yourself tax-free for those expenses decades later, effectively creating a tax-free distribution stream.

After age 65, HSAs become even more flexible. While withdrawals for non-medical expenses are subject to ordinary income tax (similar to a traditional IRA), there's no penalty. This makes HSAs function as supplemental retirement accounts with the upside potential of tax-free medical expense withdrawals.

Medical Expenses in Retirement

Healthcare represents one of the largest expense categories in retirement, with the average couple potentially needing hundreds of thousands of dollars for medical costs throughout retirement. An HSA specifically designed to cover these expenses provides significant tax advantages compared to paying from taxable accounts or traditional retirement distributions.

Life Insurance as a Tax-Free Retirement Vehicle

Permanent life insurance policies, particularly those structured as Tax-Free Retirement Accounts (TFRAs), offer another avenue for tax-free income. These policies combine death benefit protection with a cash value component that grows tax-deferred and can be accessed through policy loans and withdrawals.

Understanding how TFRAs function reveals that while these are not technically retirement accounts in the IRA or 401(k) sense, properly structured permanent life insurance can provide tax-free access to cash value during retirement years. This strategy works best for individuals who have maximized other retirement account contributions and need additional tax-advantaged saving vehicles.

Permanent Life Insurance Retirement Benefits:

- Cash value grows tax-deferred

- Policy loans are not taxable events

- Death benefit passes income-tax-free to beneficiaries

- No contribution limits like qualified retirement plans

- Can supplement other retirement income sources

- Provides estate planning benefits simultaneously

The key to using life insurance effectively for tax-free retirement income lies in proper policy design and funding. Overfunding strategies that maximize cash value accumulation while maintaining the policy's insurance status require expertise in both insurance and tax planning. Comprehensive retirement planning services can help structure these policies appropriately.

Strategic Withdrawal Sequencing for Tax Efficiency

Creating tax-free retirement income isn't just about which accounts you fund; it's equally about the order in which you withdraw from various accounts. Strategic withdrawal sequencing can significantly reduce lifetime tax obligations and preserve more wealth throughout retirement.

The general principle involves drawing from taxable accounts first, tax-deferred accounts second, and tax-free accounts last. This approach allows tax-free accounts maximum time to grow while potentially keeping you in lower tax brackets during early retirement years.

The Four-Bucket Withdrawal Strategy

- Taxable Accounts (Brokerage): Withdraw first to allow tax-advantaged accounts more growth time

- Tax-Deferred Accounts (Traditional IRA, 401(k)): Withdraw strategically to manage tax brackets

- Tax-Free Accounts (Roth IRA, HSA): Preserve for later years or higher-expense periods

- Tax-Free Insurance: Access through loans when additional income doesn't trigger tax consequences

This sequencing strategy becomes more nuanced when considering required minimum distributions (RMDs), Social Security timing decisions, and state tax implications. Tax-savvy withdrawal strategies require annual adjustments based on changing tax laws, account balances, and personal circumstances.

| Account Type | Tax on Contributions | Tax on Growth | Tax on Withdrawals | RMD Required |

|---|---|---|---|---|

| Traditional IRA/401(k) | Deductible | Tax-deferred | Ordinary income | Yes, age 73 |

| Roth IRA/401(k) | After-tax | Tax-free | Tax-free (qualified) | No (Roth IRA) |

| HSA | Deductible | Tax-free | Tax-free (medical) | No |

| Taxable Brokerage | After-tax | Capital gains/dividends | Capital gains rates | No |

Building a Comprehensive Tax-Free Retirement Strategy

Creating substantial tax-free retirement income requires a multi-account approach that begins years or decades before retirement. The most effective strategies combine several vehicles working in concert to provide flexibility, tax efficiency, and income security.

Starting in Your 30s and 40s

For professionals in their prime earning years, the foundation of tax-free retirement income begins with maximizing Roth contributions when income allows and tax brackets are manageable. This period offers the longest time horizon for tax-free compounding, making even modest Roth contributions extremely valuable.

Simultaneously establishing an HSA and adopting a "save now, spend later" approach creates another tax-free income source specifically for healthcare costs. Given the power of compound growth, a 35-year-old maximizing HSA contributions could accumulate several hundred thousand dollars by retirement, all available tax-free for medical expenses.

Early-Career Priority Actions:

- Contribute enough to employer 401(k) to capture full match

- Maximize Roth IRA contributions if income allows

- Establish and fund HSA if eligible

- Consider Roth 401(k) over traditional if in moderate tax bracket

- Build emergency fund in taxable accounts for flexibility

Approaching Retirement in Your 50s and 60s

As retirement approaches, the focus shifts toward strategic Roth conversions during lower-income years and finalizing the tax diversification of your portfolio. This decade offers a crucial window for implementing sophisticated tax strategies that can significantly impact retirement income efficiency.

Individuals aged 50 and older benefit from catch-up contributions, allowing an additional $7,500 to 401(k) plans and $1,000 to IRAs and HSAs in 2026. These enhanced limits provide opportunities to accelerate both pre-tax and Roth savings as retirement nears.

Common Pitfalls to Avoid

Even well-intentioned retirement savers can undermine their tax-free retirement goals through common mistakes. Understanding these pitfalls helps you maintain course toward optimal tax efficiency.

Over-concentration in Tax-Deferred Accounts

Many professionals accumulate substantial traditional 401(k) and IRA balances without balancing them with Roth assets. This creates a future tax obligation that can push retirees into higher brackets when RMDs begin at age 73, potentially causing Social Security benefits to become taxable and Medicare premiums to increase.

Tax diversification across traditional, Roth, and taxable accounts provides flexibility to manage taxable income year-by-year in retirement. Forbes outlines multiple strategies for building this balanced approach to tax-free income sources.

Ignoring State Tax Implications

While federal tax planning receives the most attention, state income taxes significantly impact retirement income efficiency. Some states don't tax retirement income at all, while others fully tax traditional retirement distributions but exempt Social Security. A few states have no income tax whatsoever, making Roth conversions potentially less valuable if you plan to relocate.

Understanding where you'll retire and how that state treats various income sources should inform your tax-free retirement strategy from the beginning. The value of Roth accounts, for example, increases if you expect to retire in a high-tax state.

Premature Roth Withdrawals

While Roth accounts offer flexibility to withdraw contributions anytime, tapping these accounts prematurely sacrifices decades of potential tax-free growth. Every dollar withdrawn from a Roth account loses its future tax-free earning potential, making early withdrawals costly even though they're not penalized.

Five-Year Rules to Remember:

- Earnings withdrawals must occur after age 59½ AND five years after first Roth contribution

- Each Roth conversion has its own five-year clock for penalty-free withdrawal

- Roth 401(k) distributions must meet five-year requirement even if older than 59½

- Missing the five-year mark triggers taxes and potential penalties on earnings

Coordinating Tax-Free Strategies with Overall Financial Planning

Tax-free retirement planning doesn't exist in isolation. The most effective strategies integrate with broader financial planning goals including estate planning, charitable giving, insurance needs, and investment management. Comprehensive financial guidance considers how each decision impacts the overall financial picture.

For example, Roth accounts provide significant estate planning advantages since beneficiaries can inherit them tax-free and stretch distributions over their lifetimes. Similarly, HSAs can serve dual purposes as both health expense coverage and legacy assets. Life insurance policies structured for retirement income can simultaneously address income needs and provide estate liquidity.

Charitable Giving Integration

Qualified Charitable Distributions (QCDs) from traditional IRAs offer another tax-efficient strategy when coordinated with tax-free retirement planning. After age 70½, you can direct up to $105,000 annually (in 2026) from your IRA directly to qualified charities. These distributions count toward RMDs but aren't included in taxable income.

This strategy becomes particularly powerful when combined with substantial Roth assets. By using QCDs to satisfy RMDs from traditional accounts while preserving Roth assets for personal use, you effectively convert what would have been taxable distributions into charitable contributions without increasing your adjusted gross income.

Working with Professional Advisors

The complexity of tax law, retirement account rules, and strategic planning considerations makes professional guidance valuable for those pursuing tax-free retirement income. Understanding tax implications across different account types requires expertise that evolves with changing legislation and personal circumstances.

A fiduciary advisor brings objectivity to decisions about Roth conversions, withdrawal sequencing, and account selection. They can model different scenarios to show how choices today impact tax obligations decades into the future. This forward-looking analysis often reveals opportunities and risks that aren't apparent when considering only current circumstances.

Questions to Ask Your Advisor

When working with financial professionals on tax-free retirement strategies, consider asking:

- What's my optimal mix of traditional versus Roth contributions given my current and projected tax situation?

- Should I pursue Roth conversions, and if so, how much should I convert annually?

- How should I coordinate multiple tax-advantaged accounts to maximize tax-free income?

- What withdrawal sequence minimizes lifetime taxes given my specific situation?

- How do state tax considerations affect my strategy?

- What impact will required minimum distributions have on my tax situation?

The Role of Tax-Advantaged Accounts in Modern Retirement

The retirement landscape has shifted dramatically over recent decades, with defined benefit pensions largely replaced by defined contribution plans that place investment and tax planning responsibility on individuals. Tax-advantaged retirement accounts have become essential tools for building financial security.

This shift makes understanding and maximizing tax-free retirement income sources increasingly important. Unlike previous generations who relied primarily on Social Security and pensions (both taxable), today's retirees have the opportunity to structure significant portions of their income to arrive tax-free if they plan strategically.

The flexibility to choose between traditional and Roth treatment for contributions, combined with sophisticated conversion and withdrawal strategies, provides unprecedented control over retirement tax obligations. However, this flexibility also creates complexity that requires education, planning, and often professional guidance.

Legislative Considerations for 2026 and Beyond

Tax law continues to evolve, with potential changes affecting retirement account rules, contribution limits, and tax rates. The SECURE Act and SECURE 2.0 have already altered RMD ages and catch-up contribution rules, with additional changes possible as lawmakers address budget deficits and changing demographics.

Staying informed about legislative changes and adjusting your tax-free retirement strategy accordingly ensures you continue maximizing available opportunities. Some provisions, such as the backdoor Roth strategy, exist due to legislative gaps rather than explicit design, making them potentially vulnerable to elimination in future tax reforms.

Building a tax-free retirement income stream requires thoughtful planning, strategic execution, and ongoing management across multiple account types and decades of saving. By understanding the tools available, avoiding common pitfalls, and coordinating strategies with your broader financial goals, you can significantly reduce or eliminate taxes on retirement distributions. Whether you're just starting your career or approaching retirement, the principles of tax diversification and strategic planning remain essential. Brookwood Investment Group specializes in creating personalized retirement strategies that integrate tax-efficient planning with investment management and estate planning, helping clients navigate the complexities of building sustainable, tax-optimized retirement income tailored to their unique circumstances and goals.