Planning for a secure financial future requires intentional decision-making and strategic allocation of resources. For many Americans, retirement represents decades of life after their primary working years, which means accumulating sufficient wealth to maintain their desired lifestyle throughout this extended period. Understanding the fundamentals of retirement investment empowers individuals to make informed choices that align with their unique circumstances, risk tolerance, and long-term objectives. A comprehensive approach to building retirement wealth involves more than simply contributing to an account; it requires thoughtful portfolio construction, regular monitoring, and adjustments based on changing life circumstances and market conditions.

Understanding Retirement Investment Fundamentals

Retirement investment encompasses the systematic process of allocating financial resources into various vehicles designed to grow over time and provide income during your non-working years. This process differs significantly from other investment approaches due to its extended time horizon and specific purpose.

The foundation of effective retirement investing rests on several key principles. Time horizon plays a critical role in determining appropriate strategies, as individuals in their 30s can tolerate different risk levels compared to those approaching retirement age. Tax efficiency represents another crucial consideration, given that retirement accounts offer various tax advantages that can significantly impact long-term wealth accumulation.

Key Account Types and Their Advantages

Different retirement investment vehicles offer distinct benefits and limitations. Understanding these differences helps individuals optimize their savings strategy.

Employer-Sponsored Plans:

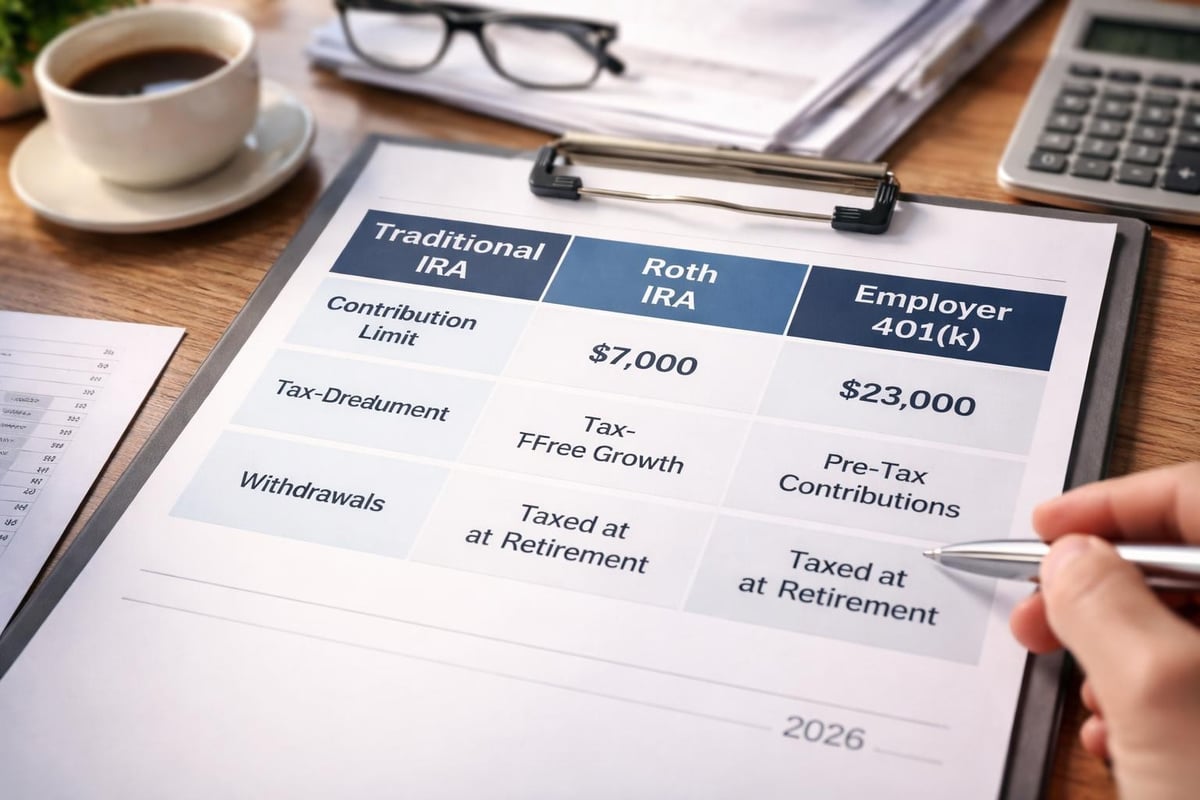

- 401(k) plans with potential employer matching contributions

- 403(b) accounts for nonprofit and educational institution employees

- 457 plans for government workers

- Simple IRA options for small business employees

Individual Retirement Accounts:

- Traditional IRAs with tax-deductible contributions

- Roth IRAs offering tax-free qualified withdrawals

- SEP IRAs for self-employed individuals

- Solo 401(k) plans for business owners without employees

The choice between these options depends on current income, expected future tax rates, employer benefits, and individual circumstances. Many successful retirement savers utilize multiple account types to create tax diversification, which provides flexibility in managing taxable income during retirement years. Working with fiduciary advisors ensures recommendations align with your best interests rather than commission-based products.

Asset Allocation Strategies Across Life Stages

Portfolio construction represents one of the most critical aspects of retirement investment success. The mix of stocks, bonds, and other assets determines both growth potential and risk exposure.

Traditional guidance suggested subtracting your age from 100 to determine stock allocation percentage, but modern approaches recognize increased longevity and adjust this formula. With life expectancy extending well into the 80s and 90s for many Americans, longevity presents unique financial challenges that require portfolios to maintain growth potential even in later years.

Age-Based Portfolio Recommendations

| Age Range | Stock Allocation | Bond Allocation | Alternative Assets |

|---|---|---|---|

| 20-35 | 85-95% | 5-15% | 0-5% |

| 36-50 | 75-85% | 15-25% | 0-5% |

| 51-60 | 60-75% | 25-35% | 5-10% |

| 61-70 | 45-60% | 35-45% | 5-15% |

| 71+ | 30-50% | 40-55% | 10-20% |

These ranges provide general guidance rather than prescriptive rules. Individual circumstances, risk tolerance, other income sources, and specific goals should influence actual allocation decisions. Some individuals with substantial pension income can maintain higher equity exposure, while those relying entirely on portfolio withdrawals might prefer more conservative approaches.

Diversification within asset classes matters equally to overall allocation. The 5% diversification rule provides practical guidance for managing concentration risk by limiting individual holdings. This approach prevents overexposure to single companies or sectors that could jeopardize retirement security.

Investment Vehicles and Options

Beyond account types, understanding available investment options helps build effective portfolios. Each vehicle offers different characteristics regarding returns, risk, fees, and liquidity.

Target-date funds have gained popularity as simplified retirement investment solutions. These funds automatically adjust asset allocation based on expected retirement date, becoming more conservative as that date approaches. While convenient, investors should understand the underlying glide path and ensure it matches their risk tolerance and circumstances.

Individual Securities:

- Stocks providing growth potential and dividend income

- Bonds offering stability and predictable income streams

- Real estate investment trusts for property exposure

- Commodities and precious metals for inflation protection

Pooled Investment Vehicles:

- Mutual funds with professional management

- Exchange-traded funds offering low-cost diversification

- Index funds tracking market benchmarks

- Managed accounts with personalized strategies

Fee structures significantly impact long-term wealth accumulation. A seemingly small difference of 1% annually can reduce portfolio value by hundreds of thousands of dollars over several decades. Understanding expense ratios, transaction costs, and advisory fees helps maximize net returns. Professional investment management services should provide value exceeding their costs through superior returns, tax efficiency, or behavioral coaching.

Income Planning and Distribution Strategies

Accumulating wealth represents only half the retirement investment equation. Converting savings into sustainable income requires careful planning and execution.

Several retirement income strategies help retirees structure withdrawals while preserving capital. The traditional 4% rule suggests withdrawing 4% of portfolio value in year one, then adjusting for inflation annually. While this approach has historical support, current market conditions and longer lifespans may require modifications.

Alternative Withdrawal Approaches

The bucket strategy divides portfolios into time-based segments. Near-term buckets hold conservative investments covering 1-3 years of expenses, mid-term buckets balance growth and stability for years 4-10, and long-term buckets maintain growth orientation for expenses beyond 10 years. This approach provides psychological comfort during market volatility while maintaining overall portfolio growth potential.

Dynamic withdrawal strategies adjust distributions based on portfolio performance and market conditions. During strong market years, retirees might increase spending, while weak years trigger reduced distributions. This flexibility helps portfolios weather market cycles more effectively than static withdrawal rates.

Key Income Sources to Coordinate:

- Social Security benefits and optimal claiming strategies

- Pension payments from former employers

- Required minimum distributions from tax-deferred accounts

- Rental income from real estate holdings

- Part-time work or consulting income

- Annuity payments providing guaranteed income

Tax-efficient withdrawal sequencing can significantly extend portfolio longevity. Generally, withdrawing from taxable accounts first, then tax-deferred accounts, and finally Roth accounts maximizes after-tax income. However, individual situations may warrant different approaches based on current tax brackets, future income expectations, and estate planning goals. Comprehensive tax strategies integrate retirement investment decisions with broader financial planning.

Risk Management Throughout Retirement

Managing risk evolves as individuals transition from accumulation to distribution phases. While younger investors can recover from market downturns through continued contributions and time, retirees face sequence-of-returns risk, where poor early returns can permanently impair portfolio sustainability.

Market volatility near retirement presents particular challenges. A significant downturn just before or shortly after retirement, combined with withdrawals for living expenses, can deplete portfolios faster than historical averages suggest. Strategies to mitigate this risk include maintaining larger cash reserves, reducing equity exposure before retirement, or implementing guardrail strategies that adjust spending based on portfolio performance.

Inflation represents another critical risk factor for retirement investment portfolios. While current inflation might seem manageable, even modest 3% annual inflation reduces purchasing power by nearly 50% over 20 years. Portfolios need growth-oriented assets to preserve real purchasing power across potentially 30-35 years of retirement.

Common Retirement Investment Risks

| Risk Type | Impact | Mitigation Strategies |

|---|---|---|

| Market Risk | Portfolio value decline | Diversification, appropriate allocation |

| Inflation Risk | Purchasing power erosion | Equity exposure, TIPS, real assets |

| Longevity Risk | Outliving savings | Conservative withdrawal rates, annuities |

| Sequence Risk | Timing of returns | Cash reserves, dynamic withdrawals |

| Healthcare Costs | Unexpected expenses | HSAs, insurance planning, reserves |

Healthcare expenses deserve special attention in retirement investment planning. Medicare covers many but not all medical costs, and long-term care expenses can quickly deplete even substantial portfolios. Health savings accounts offer triple tax advantages and can serve as supplemental retirement accounts when paired with high-deductible health plans during working years.

Behavioral Aspects of Retirement Investing

Investment success depends as much on behavioral discipline as technical knowledge. Emotional decisions during market volatility frequently undermine long-term wealth accumulation and preservation.

Research consistently demonstrates that investors who frequently trade or react to short-term market movements underperform those who maintain disciplined, long-term approaches. The average investor earns returns significantly below market averages due to poorly-timed buying and selling decisions driven by fear and greed.

Focusing on life goals rather than purely financial metrics can improve both planning quality and adherence to strategies. When retirement investment connects to specific objectives like travel, hobbies, or spending time with family, individuals demonstrate greater commitment to their plans.

Common Behavioral Pitfalls:

- Chasing performance by purchasing recent winners

- Panic selling during market downturns

- Holding losing investments too long hoping for recovery

- Overconcentration in familiar companies or sectors

- Neglecting to rebalance portfolios regularly

Systematic rebalancing removes emotion from portfolio management. Setting specific thresholds or time-based schedules for rebalancing ensures portfolios maintain target allocations regardless of market conditions. This discipline forces selling appreciated assets and purchasing underperforming ones, the essence of buying low and selling high.

Special Considerations for Different Life Situations

Retirement investment strategies should adapt to individual circumstances. Self-employed individuals face different challenges than corporate employees, while business owners have unique opportunities and complexities.

Business owners can leverage specialized retirement investment vehicles like defined benefit plans or cash balance plans that allow substantially higher contributions than standard 401(k) limits. These strategies require careful planning but can dramatically accelerate wealth accumulation for those with profitable businesses. Financial guidance for business owners addresses these unique situations.

Career changers and those with multiple employers throughout their working lives often accumulate several retirement accounts. Consolidating these accounts through rollovers can simplify management, but executing rollovers properly prevents costly mistakes like inadvertent tax consequences or temporary cash positions that miss market gains.

Specialized Situations Requiring Tailored Approaches

Individuals with substantial wealth face different retirement investment considerations than those with modest savings. High-net-worth individuals benefit from advanced strategies like tax-loss harvesting, direct indexing, and sophisticated estate planning techniques. Estate planning integration ensures retirement investments align with legacy goals and minimize transfer taxes.

Geographic flexibility creates additional opportunities. Some retirees relocate to states with favorable tax treatment or lower costs of living, stretching retirement portfolios further. International retirement introduces complexity but can offer lifestyle benefits and potentially reduced expenses depending on location choices.

Monitoring and Adjusting Your Strategy

Retirement investment requires ongoing attention rather than set-and-forget approaches. Regular reviews ensure portfolios remain aligned with goals, risk tolerance, and changing circumstances.

Annual reviews should assess performance relative to benchmarks, verify asset allocation remains within target ranges, evaluate fee structures, and confirm the strategy still matches current life situations. Major life events like marriage, divorce, inheritance, or health changes may warrant immediate strategy adjustments rather than waiting for scheduled reviews.

Tax law changes can significantly impact retirement investment strategies. Recent years have seen modifications to required minimum distribution ages, contribution limits, and withdrawal rules. Staying informed about these changes or working with advisors who monitor regulatory developments helps optimize strategies under current rules.

Market conditions influence tactical adjustments within overall strategic frameworks. While maintaining long-term discipline, recognizing when specific asset classes appear particularly overvalued or undervalued can inform rebalancing decisions or marginal allocation shifts.

Review Checklist for Annual Assessment:

- Performance versus benchmarks and goals

- Asset allocation drift from targets

- Fee analysis and cost efficiency

- Tax efficiency opportunities

- Beneficiary designations current

- Estate planning document updates

- Risk tolerance changes

- Income needs projections

- Healthcare planning adequacy

- Emergency fund sufficiency

Advanced Strategies for Optimization

Beyond fundamental approaches, sophisticated retirement investment strategies can enhance outcomes for those willing to add complexity. These techniques require more active management or professional guidance but can provide meaningful benefits.

Roth conversions allow transferring funds from traditional IRAs to Roth IRAs, paying taxes currently to enable future tax-free withdrawals. Strategic conversions during low-income years, such as early retirement before Social Security begins or between jobs, can significantly reduce lifetime tax burdens.

Selecting appropriate investment options within retirement accounts maximizes tax efficiency by placing high-growth assets in Roth accounts, bonds in tax-deferred accounts, and tax-efficient equity investments in taxable accounts. This asset location strategy complements asset allocation decisions.

Qualified charitable distributions allow individuals over 70.5 to donate required minimum distributions directly to charities, satisfying distribution requirements without increasing taxable income. This strategy benefits those with charitable inclinations who would otherwise face higher tax bills from unwanted distributions.

Coordinating Multiple Financial Elements

Social Security claiming strategies represent crucial retirement investment decisions despite technically being insurance rather than investments. Delaying benefits increases monthly payments substantially, effectively providing a risk-free, inflation-adjusted return unavailable from traditional investments. For many individuals, optimizing Social Security timing provides better value than sophisticated portfolio management.

Medicare enrollment decisions interact with retirement investment strategies. Understanding premiums, coverage gaps, and how modified adjusted gross income affects costs helps optimize the intersection of healthcare and financial planning.

Building Your Personalized Approach

No universal retirement investment strategy works for everyone. Individual circumstances, goals, risk tolerance, and values should shape personalized approaches.

Starting with clear objectives provides direction for all subsequent decisions. Specific goals like replacing 80% of pre-retirement income, funding specific travel plans, or leaving particular legacy amounts help determine required savings rates, appropriate investment strategies, and suitable withdrawal approaches.

Risk assessment extends beyond simple questionnaires to understanding both capacity and willingness to accept volatility. Someone with a substantial pension can potentially tolerate more investment risk than someone entirely dependent on portfolio withdrawals, regardless of emotional comfort with market fluctuations.

Creating customized financial plans integrates retirement investment with broader financial life, including debt management, insurance planning, estate considerations, and tax strategies. This holistic approach ensures all elements work together rather than optimizing one area while neglecting others.

Regular education and staying informed about retirement investment concepts, market conditions, and regulatory changes empowers better decision-making. However, recognizing the value of professional guidance, particularly for complex situations or those lacking time or interest to manage investments personally, often proves wise.

Building a sustainable retirement investment strategy requires balancing growth objectives with risk management across potentially several decades. Success comes from establishing clear goals, implementing appropriate strategies, maintaining discipline through market cycles, and making adjustments as circumstances evolve. Brookwood Investment Group LLC provides personalized, fiduciary guidance to help individuals navigate these complex decisions. Our virtual-first approach offers convenient access to comprehensive retirement planning, investment management, and tax strategies tailored to your unique situation. Schedule a consultation to explore how professional guidance can help you build confidence in your retirement investment approach.