Estate planning and wealth management represent two sides of the same coin when it comes to securing your financial future. While many individuals focus exclusively on accumulating assets during their working years, the thoughtful distribution and protection of those assets require equal attention. The landscape of estate planning has evolved significantly, particularly in 2026, with changing tax laws, digital assets becoming increasingly prevalent, and families becoming more geographically dispersed. Understanding how estate planning and comprehensive financial strategies intersect enables you to make informed decisions that protect both your loved ones and your legacy.

Understanding the Foundation of Estate Planning

Estate planning and financial advisory services work together to create a comprehensive strategy for managing your assets during your lifetime and beyond. At its core, estate planning involves determining how your assets will be distributed, who will make decisions on your behalf if you become incapacitated, and how to minimize the tax burden on your beneficiaries.

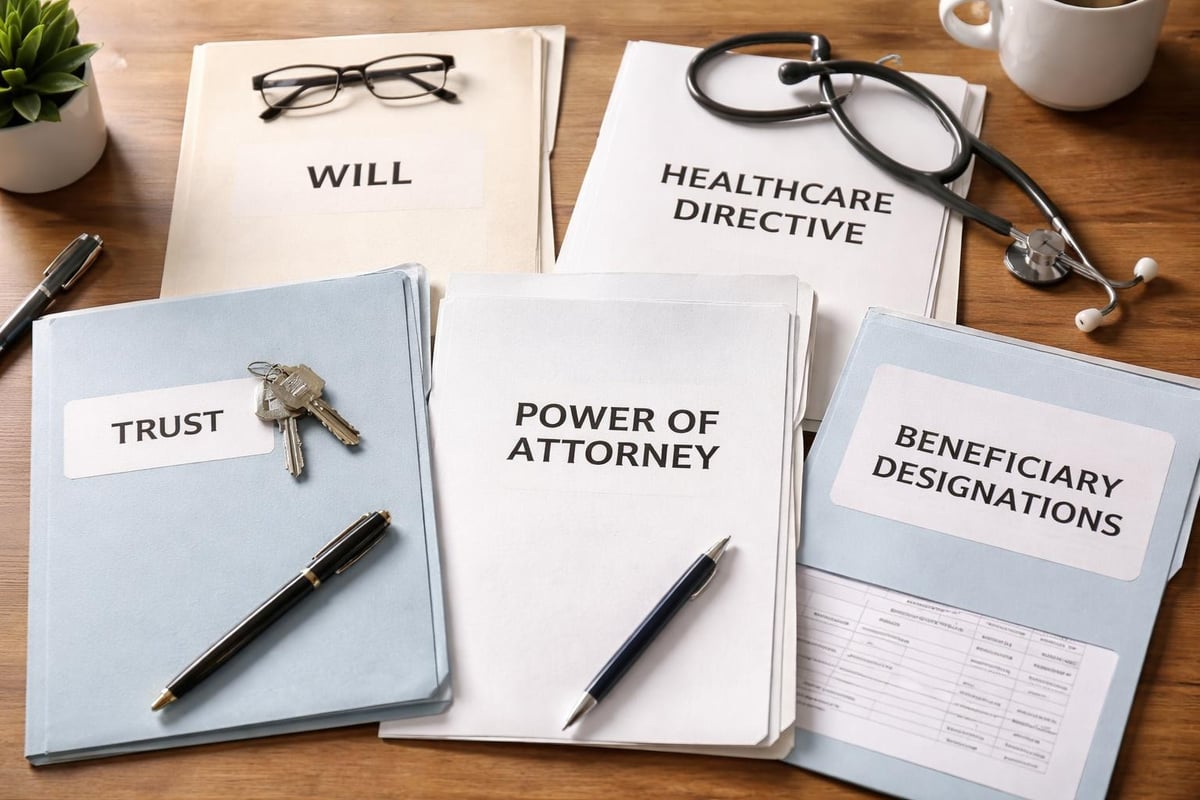

The components of a thorough estate plan extend far beyond a simple will. Estate planning and related documents typically include:

- Last Will and Testament for asset distribution

- Revocable or Irrevocable Trusts for asset protection

- Healthcare Directives for medical decisions

- Durable Power of Attorney for financial management

- Beneficiary Designations for retirement accounts and insurance

- Digital Asset Planning for online accounts and cryptocurrency

These elements form the framework that protects your wishes and provides clarity for your family during difficult times. Working with qualified professionals ensures each component aligns with your overall financial goals.

Tax Implications in Estate Planning and Wealth Transfer

Estate planning and tax strategy remain inseparable in 2026. The federal estate tax exemption amount changes periodically, and understanding current thresholds helps determine whether your estate may face tax liability. According to the IRS estate tax guidelines, estates exceeding certain values may be subject to federal taxation.

Federal Estate Tax Considerations

The relationship between estate planning and taxation requires careful analysis of your total asset value. This includes real estate, investment accounts, retirement funds, business interests, and life insurance proceeds.

| Estate Component | Tax Treatment | Planning Strategy |

|---|---|---|

| Retirement Accounts | Taxed as ordinary income to beneficiaries | Consider Roth conversions |

| Primary Residence | Step-up in basis applies | Coordinate with capital gains planning |

| Life Insurance | Generally tax-free to beneficiaries | Use trusts for large policies |

| Business Interests | Complex valuation rules apply | Implement succession planning early |

State-level estate taxes add another layer of complexity. Several states maintain their own estate or inheritance taxes with lower exemption thresholds than federal limits. Estate planning and state tax considerations become particularly important if you own property in multiple states or plan to relocate during retirement.

Gift Tax Planning

Estate planning and gifting strategies can work together to reduce the size of your taxable estate. Annual exclusion gifts allow you to transfer wealth during your lifetime without triggering gift tax consequences. In 2026, staying informed about current exclusion amounts helps maximize tax-efficient transfers.

Strategic gifting may include:

- Direct payments for education or medical expenses

- Contributions to 529 college savings plans

- Funding trusts for children or grandchildren

- Charitable donations that provide income tax deductions

Trusts as Essential Tools in Estate Planning

Estate planning and trust creation frequently go hand-in-hand for individuals seeking asset protection and control. Trusts offer flexibility that basic wills cannot provide, allowing you to specify conditions for distributions, protect assets from creditors, and potentially reduce estate taxes.

Revocable Living Trusts

A revocable living trust maintains flexibility during your lifetime while providing seamless asset transfer upon death. Estate planning and probate avoidance represent key benefits of this structure. Assets held in a properly funded revocable trust bypass the public probate process, providing privacy and potentially reducing settlement costs.

Benefits include:

- Immediate asset access for successor trustees

- Privacy protection from public probate records

- Incapacity planning with automatic successor management

- Multi-state property management without multiple probate proceedings

- Contestability reduction compared to wills alone

Irrevocable Trusts

Estate planning and irrevocable trusts serve specific purposes when asset protection or tax reduction become priorities. Once established, these trusts cannot be easily modified, but they offer unique advantages for high-net-worth individuals.

Irrevocable trust applications include life insurance trusts to exclude policy proceeds from your taxable estate, charitable remainder trusts that provide income while supporting causes you value, and special needs trusts that protect inheritances for beneficiaries with disabilities without jeopardizing government benefits.

Healthcare Directives in Estate Planning

Estate planning and healthcare decision-making intersect through advance directives that specify your medical preferences. These documents ensure your wishes are honored if you become unable to communicate them yourself.

A comprehensive healthcare directive typically includes a living will expressing your preferences for life-sustaining treatment and a healthcare power of attorney designating someone to make medical decisions on your behalf. Estate planning and end-of-life preferences may be uncomfortable topics, but addressing them prevents family conflict and ensures medical providers understand your values.

Consider these elements when preparing healthcare directives:

- Specific preferences regarding artificial nutrition and hydration

- Organ donation wishes

- Pain management priorities

- Religious or philosophical beliefs affecting medical care

- HIPAA authorization for information sharing

The American College of Trust and Estate Counsel provides resources for finding qualified professionals who can help draft these important documents with appropriate legal language for your jurisdiction.

Digital Assets in Modern Estate Planning

Estate planning and technology now intersect in ways unimaginable a generation ago. Digital assets require specific attention in your estate plan to ensure executors can access and manage them appropriately.

Categories of Digital Assets

Your digital footprint likely includes financial accounts accessed online, social media profiles, digital photos and videos stored in the cloud, cryptocurrency holdings, and intellectual property like blogs or digital art. Estate planning and digital asset management require careful documentation and access planning.

| Digital Asset Type | Planning Consideration | Access Method |

|---|---|---|

| Financial Accounts | Two-factor authentication | Password manager with executor access |

| Social Media | Memorial or deletion preferences | Legacy contact designation |

| Cryptocurrency | Private key storage | Secure backup location documented |

| Cloud Storage | Family photos and documents | Shared access credentials |

Federal and state laws regarding digital asset access continue evolving. The Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA) governs how executors and trustees can access digital property, but implementation varies by state.

Beneficiary Designations and Estate Coordination

Estate planning and beneficiary forms must align to avoid unintended consequences. Many assets transfer directly to named beneficiaries regardless of will provisions, including retirement accounts, life insurance policies, payable-on-death bank accounts, and transfer-on-death investment accounts.

Regular beneficiary review prevents common pitfalls. Outdated designations naming former spouses, deceased individuals, or minors without proper trust structures can create significant complications. Estate planning and beneficiary updates should occur after major life events such as marriage, divorce, births, deaths, or significant financial changes.

Coordination Strategies

Ensure your beneficiary designations support your overall estate plan by reviewing all accounts annually, confirming primary and contingent beneficiaries remain appropriate, verifying minor children have designated guardians or trusts, and coordinating with your financial advisor to align distributions with tax efficiency goals.

Fidelity’s estate planning resources offer tools for tracking beneficiary designations across multiple accounts, helping you maintain consistent documentation.

Business Succession in Estate Planning

Estate planning and business ownership create unique challenges requiring specialized attention. If you own a business, your estate plan must address both personal asset distribution and business continuity.

Key considerations include:

- Valuation methodology for determining business worth

- Succession planning identifying who will lead the company

- Buy-sell agreements establishing transfer terms with co-owners

- Liquidity planning ensuring estate taxes don't force business liquidation

- Family dynamics managing relationships between active and inactive family members

Business owners should consider whether family members have the interest and capability to continue operations, how to provide fair inheritance to children not involved in the business, and whether key employees should have ownership opportunities.

Estate planning and business succession often require multiple tools working together, such as trusts holding business interests, life insurance funding buy-sell agreements, and family limited partnerships facilitating gradual ownership transfer.

Charitable Giving Strategies

Estate planning and philanthropy enable you to support causes you value while potentially receiving tax benefits. Charitable giving can occur during your lifetime or as part of your estate distribution.

Lifetime Giving Options

Donor-advised funds allow you to make charitable contributions, receive immediate tax deductions, and recommend grants to specific charities over time. Charitable remainder trusts provide income during your lifetime with the remainder benefiting your chosen charity. Direct charitable contributions reduce your taxable estate while supporting organizations aligned with your values.

Testamentary Charitable Gifts

Estate planning and charitable bequests in your will or trust create lasting legacies. You can specify fixed dollar amounts, percentages of your estate, or particular assets for charitable purposes. Kiplinger’s estate planning guidance explores various charitable giving structures and their tax implications.

Special Considerations for Blended Families

Estate planning and second marriages present unique challenges requiring thoughtful planning. Balancing the needs of a current spouse with the inheritance expectations of children from previous relationships demands clear communication and specific legal structures.

Qualified Terminable Interest Property (QTIP) trusts allow you to provide for your surviving spouse while ensuring remaining assets ultimately pass to your children. Estate planning and prenuptial agreements may work together to clarify financial expectations and asset distribution. Life insurance can equalize inheritances when specific assets like a family business go to certain children.

Long-Term Care Planning Integration

Estate planning and long-term care considerations protect your assets from potential healthcare costs. The expenses associated with extended care can rapidly deplete estates without proper planning.

Strategies include long-term care insurance to cover potential nursing home or home healthcare costs, Medicaid planning for those who may need to qualify for benefits, and asset protection trusts in certain jurisdictions to shield resources while maintaining eligibility for government programs.

Starting long-term care planning well before you need care provides more options and better outcomes. Estate planning and elder law specialists can help navigate complex rules governing asset protection and benefit eligibility.

Estate Plan Review and Updates

Estate planning and regular maintenance ensure your documents remain current and effective. Life changes, tax law modifications, and shifting family dynamics all necessitate periodic review.

Recommended review schedule:

- Annual check of beneficiary designations and minor updates

- Every 3-5 years for comprehensive document review

- After major life events such as marriage, divorce, births, deaths, or significant asset changes

- Following tax law changes that may affect your strategy

Working with experienced professionals who stay current on legal and tax developments helps ensure your estate plan adapts to changing circumstances. Additional resources for ongoing education can be found through various financial planning materials that address estate planning topics.

Coordinating Estate Planning With Retirement Strategies

Estate planning and retirement planning share interconnected goals of financial security and legacy creation. Your retirement account distribution strategy affects both your lifetime income and the inheritance you leave behind.

Required minimum distributions (RMDs) from traditional retirement accounts create taxable income that impacts your estate size. Roth conversion strategies may reduce future tax burdens for beneficiaries. Estate planning and beneficiary designation for retirement accounts determine whether distributions stretch over beneficiaries' lifetimes or must be withdrawn within shorter timeframes under current regulations.

The SECURE Act changed inherited IRA rules significantly, generally requiring non-spouse beneficiaries to withdraw accounts within ten years. Estate planning and these distribution requirements affect how you structure account ownership and beneficiary designations.

Estate planning and comprehensive financial strategies work together to protect everything you've built throughout your lifetime. The key takeaways include maintaining current documentation, coordinating beneficiary designations with your overall plan, and reviewing your strategy regularly to adapt to life changes and evolving laws. Brookwood Investment Group LLC provides personalized guidance on integrating estate planning into your comprehensive financial strategy, helping you make informed decisions that align with your unique goals and family situation. As a fiduciary advisor, we work collaboratively with your legal and tax professionals to ensure all aspects of your financial life work together effectively.