Managing retirement tax obligations requires careful planning and strategic decision-making. One approach that continues to gain attention among retirement savers is the partial Roth conversion, a technique that allows individuals to systematically convert portions of their traditional retirement accounts into Roth IRAs over time. This measured approach offers opportunities to manage tax brackets, reduce future required minimum distributions, and create tax-free income streams during retirement. Understanding how this strategy works and when it might be appropriate can help you make informed decisions about your retirement planning.

Understanding the Mechanics of Partial Roth Conversions

A partial Roth conversion involves transferring a specific portion of your traditional IRA, 401(k), or other qualified retirement account to a Roth IRA. Unlike converting your entire balance at once, this strategy focuses on converting smaller amounts over multiple years.

When you execute a partial Roth conversion, you pay income tax on the converted amount in the year of conversion. The converted funds then grow tax-free in the Roth IRA, and qualified withdrawals during retirement are not subject to federal income tax.

Key Differences from Full Conversions

The distinction between partial and full conversions matters significantly for tax management:

- Tax bracket control: Converting smaller amounts helps you stay within your current tax bracket

- Flexibility: You can adjust conversion amounts annually based on your income and tax situation

- Risk management: Spreading conversions across years reduces the impact of market volatility

- Planning precision: Allows for more refined tax planning aligned with your specific financial circumstances

Understanding the strategic considerations for retirement planning helps you determine the right conversion approach for your situation.

Tax Benefits and Strategic Advantages

The primary advantage of a partial Roth conversion centers on tax optimization. By converting amounts that keep you within a target tax bracket, you can potentially pay less in total taxes over your lifetime compared to larger, one-time conversions.

Managing Future Required Minimum Distributions

Traditional IRAs require you to begin taking required minimum distributions (RMDs) at age 73 as of 2026. These mandatory withdrawals can push you into higher tax brackets and potentially increase Medicare premiums.

| Traditional IRA | Roth IRA |

|---|---|

| Subject to RMDs starting at age 73 | No RMDs during owner's lifetime |

| Distributions taxed as ordinary income | Qualified distributions are tax-free |

| Increases taxable income in retirement | Does not increase AGI |

| May affect Medicare premiums | No impact on IRMAA calculations |

The tax benefits of a partial Roth conversion become particularly valuable when you consider the long-term reduction in RMDs and associated tax consequences.

Creating Tax Diversification

Having both traditional and Roth accounts provides flexibility in retirement. You can strategically withdraw from different account types based on your annual tax situation, managing your taxable income more effectively.

Benefits of tax diversification include:

- Ability to fill lower tax brackets with traditional IRA withdrawals

- Supplementing income with tax-free Roth distributions as needed

- Greater control over taxable income for Medicare premium calculations

- Flexibility to respond to changing tax laws and personal circumstances

Optimal Timing for Partial Roth Conversions

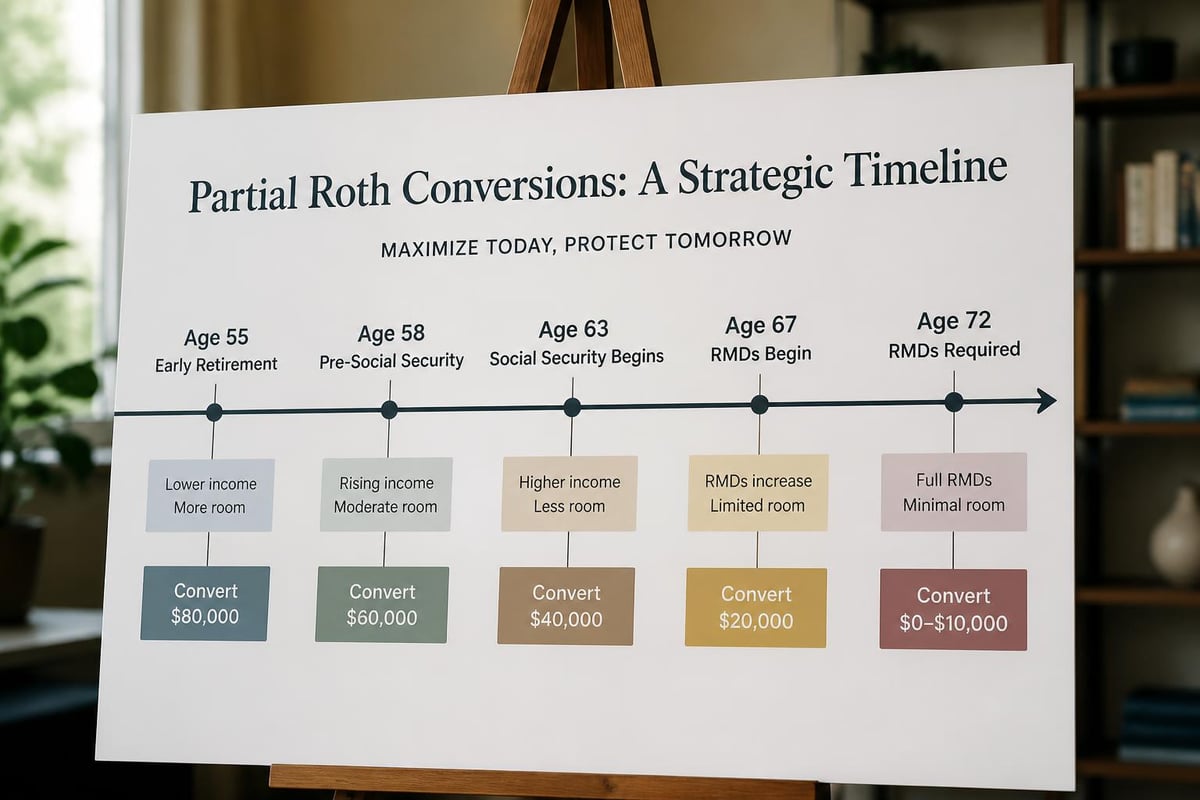

Identifying the right time to execute a partial Roth conversion requires analyzing your current and projected future tax situations. Several scenarios often present favorable opportunities.

Low-Income Years

Years when your income drops below your typical earnings create excellent conversion opportunities. This might occur during:

- Early retirement years before Social Security and RMDs begin

- Career transitions or temporary unemployment

- Business downturns for self-employed individuals

- Sabbaticals or extended time off from work

Converting during these periods allows you to take advantage of lower marginal tax rates.

Before Required Minimum Distributions Begin

The years between retirement and age 73 often represent a strategic window for conversions. Smart Roth conversions during this period can significantly reduce the size of your traditional IRA before RMDs commence.

Market Downturns

When investment values decline, converting a specific dollar amount means you're converting more shares. If the market recovers, that growth occurs in the tax-free Roth environment.

Consider this example: Converting $50,000 when your account balance is down 20% means you convert more shares than the same $50,000 conversion would have purchased at higher valuations.

Calculating Your Optimal Conversion Amount

Determining how much to convert each year requires careful analysis of your tax situation. The goal is typically to convert up to the top of your current tax bracket without pushing into the next bracket.

Tax Bracket Analysis Steps

Step 1: Calculate your current taxable income

Step 2: Identify your current marginal tax bracket

Step 3: Determine the remaining room in your current bracket

Step 4: Consider other income sources and deductions

Step 5: Calculate the maximum conversion amount that keeps you in your target bracket

Factors That Influence Conversion Amounts

Beyond simple bracket management, several factors should influence your conversion decisions:

- Projected future tax rates: Both personal and legislative

- State income tax implications: Some states tax Roth conversions

- Medicare premium considerations: Large conversions can trigger IRMAA surcharges

- Time horizon: Years until you need the funds

- Estate planning goals: Tax-free inheritance for beneficiaries

| Consideration | Impact on Conversion Strategy |

|---|---|

| Current age 60-72 | Maximum flexibility for multi-year conversions |

| High state income tax | May reduce conversion benefits |

| Large traditional IRA balance | Requires longer conversion timeline |

| Expected tax law changes | May accelerate or delay conversions |

| Desire to leave tax-free inheritance | Increases conversion priority |

Common Misconceptions and Mistakes

Even well-intentioned savers can make errors when implementing a partial Roth conversion strategy. The Roth conversion mistake too many people make often involves converting too much at once without considering the full tax implications.

Converting Without Adequate Cash Reserves

One critical mistake involves paying conversion taxes from the IRA itself rather than from outside funds. Using IRA funds to pay taxes reduces the amount that can grow tax-free and may trigger early withdrawal penalties if you're under age 59½.

Best practice: Maintain sufficient cash reserves in taxable accounts to cover conversion taxes without touching retirement funds.

Ignoring the Five-Year Rule

Each Roth conversion has its own five-year clock for penalty-free withdrawals of converted amounts. Converting funds you might need within five years requires careful planning to avoid penalties.

Failing to Coordinate with Other Income

Conversion amounts should account for all income sources in a given year, including capital gains, bonuses, or other one-time income events that might push you into higher brackets.

Scenarios When Partial Conversions May Not Be Appropriate

While partial Roth conversions offer benefits for many retirement savers, they're not universally appropriate. Knowing when to say no to a Roth conversion is equally important as recognizing opportunities.

Already in High Tax Brackets

If you're currently in one of the highest marginal tax brackets and expect to be in a lower bracket during retirement, paying high taxes now to convert may not provide benefits.

Short Time Horizon

The tax-free growth advantage of Roth IRAs requires time. If you need the funds within a few years, the conversion taxes may outweigh potential benefits.

Limited Cash for Tax Payments

Without sufficient funds outside retirement accounts to pay conversion taxes, the strategy becomes less effective.

Potential Need for Early Withdrawals

If you anticipate needing to access converted funds before the five-year period expires, penalties could negate the benefits.

Implementing a Multi-Year Conversion Strategy

A successful partial Roth conversion approach typically unfolds over several years. This systematic method allows you to take advantage of multiple years of favorable tax treatment while maintaining control over your tax liability.

Annual Review Process

Each year, review and adjust your conversion strategy based on:

- Changes in tax law and bracket thresholds

- Your current income and deduction situation

- Market performance and account balances

- Evolving retirement timeline and needs

- Estate planning considerations

Coordination with Other Tax Strategies

Partial Roth conversions work best when integrated with comprehensive retirement planning and tax strategies. Consider how conversions interact with:

- Tax-loss harvesting in taxable accounts

- Charitable contributions and qualified charitable distributions

- Health savings account contributions and distributions

- Capital gains management strategies

Working with Professional Guidance

The complexity of partial Roth conversion planning often benefits from professional expertise. Getting comprehensive advice about Roth conversions goes beyond simple tax calculations to encompass your entire financial picture.

What Professional Advisors Analyze

A fiduciary advisor evaluates multiple dimensions of your situation:

- Current and projected tax brackets

- Income sources throughout retirement

- Estate planning objectives

- Medicare premium management

- State tax implications

- Legacy goals for beneficiaries

Personalized Modeling

Professional financial planning software can model different conversion scenarios, showing projected outcomes based on various assumptions about tax rates, investment returns, and withdrawal patterns.

| Analysis Component | Value to Decision-Making |

|---|---|

| Lifetime tax projection | Quantifies total tax savings potential |

| Cash flow modeling | Ensures adequate liquidity for tax payments |

| RMD impact analysis | Shows reduction in future required distributions |

| Estate value projection | Demonstrates benefit to heirs |

| Break-even timeline | Identifies when conversion benefits exceed costs |

Key Considerations for 2026 and Beyond

As we navigate 2026, several factors make partial Roth conversion planning particularly relevant. Current tax laws scheduled to sunset in 2025 have been extended in modified form, but future changes remain possible.

Legislative Environment

Tax laws continue to evolve, and staying informed about potential changes helps you time conversions strategically. Understanding when a Roth conversion is beneficial requires awareness of both current rules and potential future modifications.

Planning for Uncertainty

Given potential legislative changes, many financial professionals recommend accelerating partial conversions while current tax rates remain relatively favorable compared to historical levels.

Strategies to address uncertainty:

- Convert more aggressively if you expect higher future tax rates

- Maintain flexibility to adjust annual conversion amounts

- Document your decision-making process and assumptions

- Review and update projections annually

Integration with Comprehensive Planning

Partial Roth conversions shouldn't exist in isolation. They form one component of holistic financial planning that addresses retirement income, investment management, estate planning, and tax efficiency together.

Implementing a partial Roth conversion strategy requires careful analysis of your unique tax situation, retirement timeline, and financial goals. This measured approach to converting traditional retirement accounts can provide significant benefits through tax bracket management, RMD reduction, and creation of tax-free income streams. However, the complexity of these decisions and their long-term implications make professional guidance valuable. Brookwood Investment Group LLC offers personalized financial planning that integrates partial Roth conversion strategies with comprehensive retirement, investment, and tax planning tailored to your specific circumstances. As a fiduciary advisor, we can help you evaluate whether this strategy aligns with your goals and implement a multi-year plan designed for your situation.